Guest Post by Wolf Richter from his blog on WolfStreet.com:

It makes sense to see a recession later this year. The Fed has hiked interest rates with the top of its policy rates now at 5.0%. Businesses and consumers haven’t had to deal with these kinds of short-term interest rates in 15 years. Three banks have blown up because long-term rates have risen sharply, and they got caught not preparing for it, and depositors then pulled the rug out from under them. Economists are widely predicting a recession later this year. Even the Federal Reserve’s staff projections, prepared for the March meeting and mentioned in the minutes, included the possibility of “a mild recession starting later this year.”

So the recession scenario later this year is getting baked in. Wall Street’s megaphones, assorted hedge fund gurus, and the occasional bond kings are all on board: We’re going to get a recession, and the Fed is going to be forced to cut rates this year to deal with it.

Rate cuts is what all these people want, because they hope that it would put an end to this horrible misery where the money isn’t free, and they’re counting on it and they’re betting on it.

But before the cuts, there will be one more hike, they figure. The likelihood of a 25-basis point rate hike on May 3 has risen to 87% today, according to the Investing.com Fed Rate Hike Monitor, which is based on CME Fed Fund futures. So that is now kind of a done deal, as far as markets are concerned.

If the Fed hikes its policy rates by 25 basis points, to a range of 5.0% to 5.25%., markets then expect rate cuts by year end.

The likelihood of one or more rate cuts by December is 87%, according to the Rate Hike Monitor. Specifically:

- One cut: 30%;

- Two cuts: 35%;

- Three cuts: 18%;

- Four cuts: 4%.

Some things in the economy have started to wobble. Three mid-sized banks collapsed in March – two crypto-eager banks, Silvergate Bank and Signature Bank; and the startup-centered bank, Silicon Valley Bank. They all were concentrated on a peculiar bunch of depositors with lots of uninsured deposits: crypto companies and massively funded startup companies. Then there was some contagion, and other banks got hit by runs and were teetering for a few days.

But the Fed’s liquidity programs largely ended the deposit flight, banks have been paying back those loans, and now all eyes are back on bank earnings – and so far for Q1, bank earnings have been pretty good.

Earnings at the largest banks benefited from the spread between what they’re paying on deposits and what they’re charging on their loans, and revenues at the four mega-banks all jumped. They all increased their loan loss provisions, but the banks generated so much in profits that it barely made a dent. JPMorgan’s CEO Jamie Dimon is still seeing “the storm clouds” on the horizon that he saw a year ago, but they’re still on the horizon. He said that the US would eventually have a recession, and everyone can agree with that because eventually, there’s always a recession.

But what if there’s no recession this year?

Consumers slowed their spending late last year. But this year, they got used to all the stuff going on around them, and they picked up their spending.

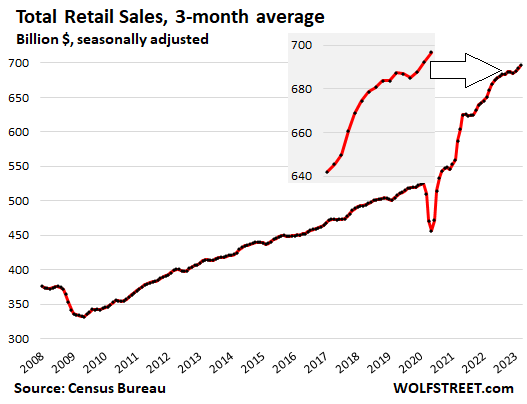

We saw that in retail sales for the first three months: Q1 was up by 1.7% from Q4 and by 5.4% from the same period a year ago, despite plunging prices of gasoline and dropping prices of many goods that retailers sell:

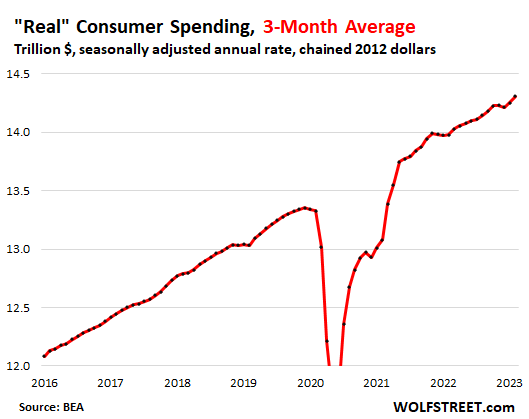

And we saw it in overall consumer spending, which includes services, and all of it adjusted for inflation, through February. The three-month moving average of “real” consumer spending, adjusted for inflation, was up 2.4% year-over-year. Better than just muddling through, but a notch below the 2.9% “real” consumer spending growth on average in 2015 through 2019, when interest rates were a lot lower. You can see the slowdown late last year and the pickup this year:

St. Louis Federal Reserve President James Bullard told Reuters in an interview that “Wall Street is very engaged in the idea there’s going to be a recession in six months or something, but that isn’t really the way you would read an expansion like this.”

They may see rate cuts in the near future, part of a recession-breeds-accommodation view of the world, he told Reuters, but “the labor market just seems very, very strong. And the conventional wisdom is that if you have a strong labor market that feeds into strong consumption … and that’s a big chunk of the economy.”

“It doesn’t seem like the moment to be predicting that you have a recession in the second half of 2023,” he said. These recession forecasts “are coming from models that put too much weight on the idea that interest rates went up quickly,” he said.

And “what about the pandemic money still to be spent off, both at the state and local level and at the individual household level?”

The trillions of dollars that the government handed out directly to consumers, businesses, and state and local governments are still sloshing through the system. States like California are racking up big deficits on an accounting basis, but they’re still sitting on piles of cash from the pandemic, and they are spending it.

Consumers are awash in cash. You can see that in the deposits at banks which hit $18 trillion by the end of 2021 and have now dipped to $17.4 trillion, which is still huge. You can see it in the different measures of money market funds that have all shot up. Consumers have also parked a lot of cash in Treasury bills. Many of these instruments are paying from 4% to 5% in interest.

That’s a lot of additional cash-flow that consumers are now getting. On, say, $10 trillion of all these instruments combined, an average 3.5% interest rate would generate $350 billion a year in cash flow that consumers didn’t get 15 months ago during the near-0% era, and that they now get to spend. And many, especially retirees, are spending every dime of that cash flow.

I’ve been saying for a while that this is a weird economy. It has refused to go into a recession despite the higher rates, and despite some wobbles in some areas. Instead, it’s adjusting to the 5% rates and to higher inflation. Everyone is getting used to it.

“Inflation is coming down, but not as fast as Wall Street expects,” Bullard said. To get a handle on inflation, Bullard feels that the Fed should hike further after the May meeting to push its policy rate into the mid-5% range.

“You want to be responsive to incoming data through the summer into the fall,” he said. “You wouldn’t want to be caught giving forward guidance that said we’re definitely not doing anything and then have inflation coming in too hot or too sticky.”

Once interest rates are considered “sufficiently restrictive” to slow inflation, Bullard felt “the bias would be higher for longer” to make sure inflation is fully under control.

And so the economy muddles through with muted growth, relatively high inflation, and 5%-plus short-term interest rates, and it’s adjusting to it, and consumers and businesses are getting used to it, and they’re sustaining this inflation by getting used to it, and so there’s no recession that would cause the Fed to loosen monetary policies, and after 14 years of free money, we’d be in a new era where money isn’t free anymore, and that would be a bummer for Wall Street.