This is fast moving now, but the Fed is still pouring fuel on the fire. Struggling to re-establish its shredded and ridiculed credibility as The Inflation Fighter, the Fed concluded its most hawkish Fed meeting in decades, raising all of its weapons higher…

by Wolf Richter on Wolf Street:

Struggling to re-establish its shredded and ridiculed credibility as inflation fighter, the Fed today concluded the most hawkish Fed meeting in decades. Following the CPI report last week that apparently had blown all doorknobs off inside the Fed’s Eccles Building, everything got moved higher by a bunch: Actual policy rates, projected policy rates by the end of 2022 and 2023, projected inflation rates, and projected unemployment rates. The only thing that got lowered was the projection of economic growth.

The FOMC voted to hike all policy rates by 75 basis points, the most hawkish move since 1994, with only one dissenting vote (by Esther George, who wanted a 50 basis point hike):

- Federal funds rate target range, to 1.50% – 1.75%.

- Interest it pays the banks on reserves, to 1.65%.

- Interest it charges on overnight Repos, to 1.75%.

- Interest it pays on overnight Reverse Repos (RRPs), to 1.55%.

- Primary credit rate it charges banks, to 1.75%.

“Clearly, today’s 75 basis point increase is an unusually large one, and I do not expect moves of this size to be common,” Fed Chair Jerome Powell said in his statement at the press conference. But he said that at the next meeting in July, another 75-basis point hike might be on the table.

And the Fed will be “looking for compelling evidence” that inflation is moving down before “declaring victory”, Powell said. This phrase, “compelling evidence,” has been cropping up a lot recently among Fed governors. They’re looking for more than just a little squiggle in the line before backing off.

Expects much higher policy rates, much faster.

This is now fast-moving. Today’s “dot plot” in the Economic Materials showed that all 18 FOMC members who participated in the meeting, expected the Fed to raise its federal funds rate to at least 3% by the end of 2022, with 13 members expecting higher rates. The median projection jumped to 3.4%.

The Fed would have to raise its policy rates by another 1.75 percentage points to get to the median projection of 3.4% by the end of this year.

The median projection for the policy rate at the end of 2023 rose to 3.8%. For 2024, it dipped to 3.4%.

These 3-4% policy rates were unthinkably and impossibly high just a few months ago. It was something the Fed would never ever and could never ever do because of whatever. Now they’re on the table.

Quantitative Tightening (QT) has kicked off.

QT has started this month. The plan was laid out in May. The Fed confirmed today that it is proceeding according to plan. During the phase-in period of June through August, the Fed caps the amount of securities that can roll off the balance sheet at $47.5 billion per month ($30 billion in Treasury securities, $17.5 billion in MBS). Starting in September, the caps will double to a total of $95 billion a month.

If not enough Treasury notes and bonds mature during the month to hit the cap, the Fed will make up the difference by allowing short-term Treasury bills to mature without replacement. In other words, the cap is essentially a fixed amount that will come off the balance sheet.

The Fed will not sell securities outright at this point, but will allow them to mature without replacement. Most of the reductions for MBS will come from the pass-through principal payments that are forwarded to MBS holders when mortgages are paid off (when the house is sold or the mortgage is refinanced) or are paid down through regular mortgage payments.

Still pouring fuel on the fire.

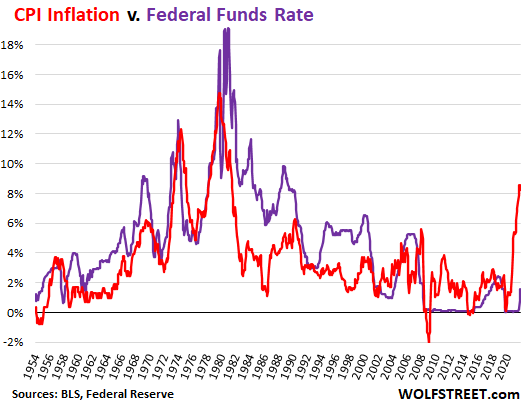

With the Fed’s target range for the federal funds rate at 1.50% to 1.75%, the effective federal funds rate (EFFR) will be around 1.6% going forward.

But CPI inflation is now 8.6%, and the “real” EFFR is now a negative 7%, which represents the amount by which the Fed has fallen behind inflation. Its slowness in reacting to inflation is unprecedented in modern times:

Kiss that “Labor Shortage” goodbye.

Higher interest rates are supposed to slow demand, which is supposed to remove some fuel from raging inflation. As a consequence of the reduced demand, unemployment is expected to tick up.

The Fed raised its projections for unemployment rates, with the median projection rising from 3.7% at the end of 2022, to 3.9% at the end of 2023, and to 4.1% at the end of 2024.

This is the first time in this cycle that the Fed is projecting that unemployment will increase as a result of its crackdown on inflation. In the May meeting’s statement, the Fed still expected its magic to bring inflation down to its target of 2%, while the labor market would remain strong. That line went out the window in today’s statement.

And Powell confirmed in the press conference that the Fed is unlikely to be able to get inflation back to 2% without deliberately slowing the economy and raising unemployment.

Rising unemployment would obviously end the “labor shortage” and untangle some of the inflationary and supply-chain issues that came with it.

Expects higher inflation rates.

The Fed has been ridiculously far behind reality over the past 15 months in its projection were inflation rates would be. But it has been raising them, and today it nudged them up further. Its median projection for the PCE inflation rate rose to 5.2% by the end of 2022. But it’s still hoping that by the end of 2023, PCE inflation will be down to 2.6%, and that by the end of 2024 it will be down to 2.2%.

But this projection too could go out the window as “participants continue to see risks to inflation as weighted to the upside,” Powell said at the press conference.

Expects economic slowdown: Avoiding a recession “not going to be easy.”

The idea is to slow demand growth by some amount, just enough to bring down inflation, but not enough to trigger a recession. But achieving that soft landing under current conditions “is not getting easier” Powell said.

“What is becoming clearer is that many factors that we don’t control are going to play a very significant role in deciding whether that’s possible or not,” he said. “It is not going to be easy.”

“The events of the last few months have raised the degree of difficulty” of getting that soft landing, he said. “There is a much bigger chance now that it will depend on factors that we don’t control. Fluctuations and spikes in commodity prices could wind up taking that option out of our hands.”

He thereby acknowledged implicitly that the risk of a recession would be the price to pay for bringing this raging inflation back down.

Expects markets to figure out their own landing.

After past sell-downs of 20% or so of the S&P 500 Index, the Fed would start putting phrases into its communications that indicated some sort of pivot. This was the Fed put. But that too has gone out the window. The S&P 500 Index is down 21% from its high, and the Nasdaq is down 31%, and yet there was nothing in any of this that indicated that the Fed is worried.

On the contrary. The market sell-off, if sustained, and sustained price declines in the housing market, could do some of the heavy lifting for the Fed, so that the Fed might not have to raise its policy rates toward the rate of inflation, or even above the rate of inflation — above the red line in the EFFR-CPI chart — to knock down inflation, which would be a real rug-pull for the economy. Seems markets are going to have to figure out how to stand on their own two feet amid rising interest rates and QT.

If you enjoy reading Wolf Richter and want to support him, click here to find out how.

Renowned economist issues startling prediction for America’s future:

According to former Goldman Sachs executive, Nomi Prins, Americans who are hoping for a ‘return to normal’ are going to be shocked when they see what happens next in America. She says, “If you’re betting your job, savings, or retirement accounts on a return to ‘normal’ you’re about to be left behind by a brand-new crisis few see coming.”

Click here now to see America’s next crisis.