The “Everything Bubble” has jumped from hyperbole to literal truth in just a couple of years, as more and more assets enter “crazy expensive/extremely reckless” territory. The latest addition to the list is collateralized loan obligations (CLOs), which are created when a bank lends money to a less-than-creditworthy company and then bundles that loan with a bunch of similar loans into bonds for sale to yield-starved pension funds and bond funds.

There’s a legitimate place in the market for this kind of security, as long as everyone understands the risks. But in financial bubbles, banks’ insatiable hunger for fees combines with bond buyers’ desperate need for income to cloud everyone’s judgment. Lending standards slip, bond quality declines, credit rating agencies look the other way to keep the deals flowing, and buyers keep buying because they have no choice.

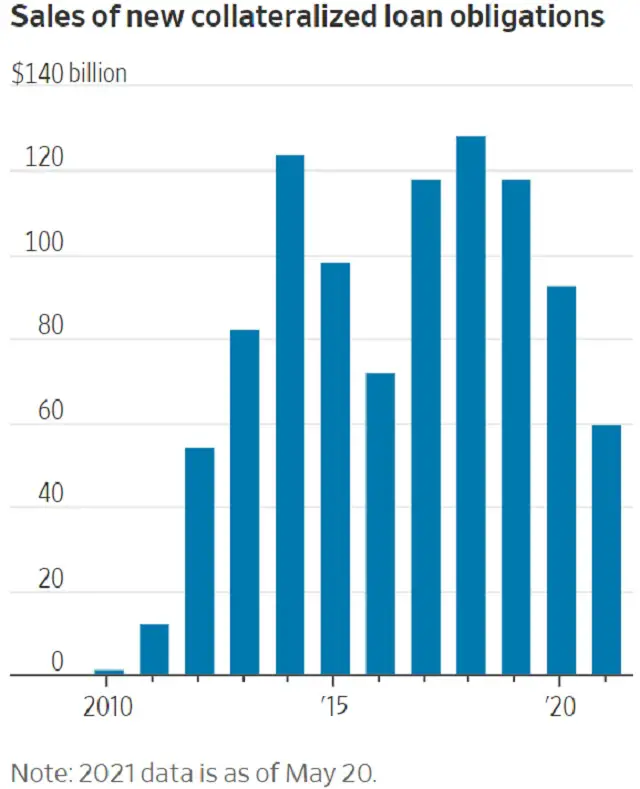

Record year

So far this year, issuance of new CLOs is on pace to easily exceed 2018’s record.

Part of this surge is, like so much else, catch-up from last year’s nationwide lockdown. But most is just your typical out-of-control financing fueled by way too much new currency being dumped into the banking system.

So how can bonds made up of below-investment-grade paper be investment grade? Through the magic of securitization. As the Wall Street Journal recently quoted CitiGroup:

Because CLOs’ loan holdings are diversified, the bonds can achieve higher credit ratings than the underlying loans, making them popular among institutions restricted to investment-grade debt, such as banks and insurers.

Meanwhile, the combination of a recovering economy and lots of lenders willing to finance pretty much anything is improving the prospects of financially challenged companies. Fewer of them are defaulting, which increases the confidence of the people buying CLO bonds. Moody’s Investors Service now expects the trailing 12-month default rate on CLOs to fall to 3.9% by the year-end, from 7.5% in March. And a growing number of firms are now being reviewed by rating agencies to have their CLOs upgraded.

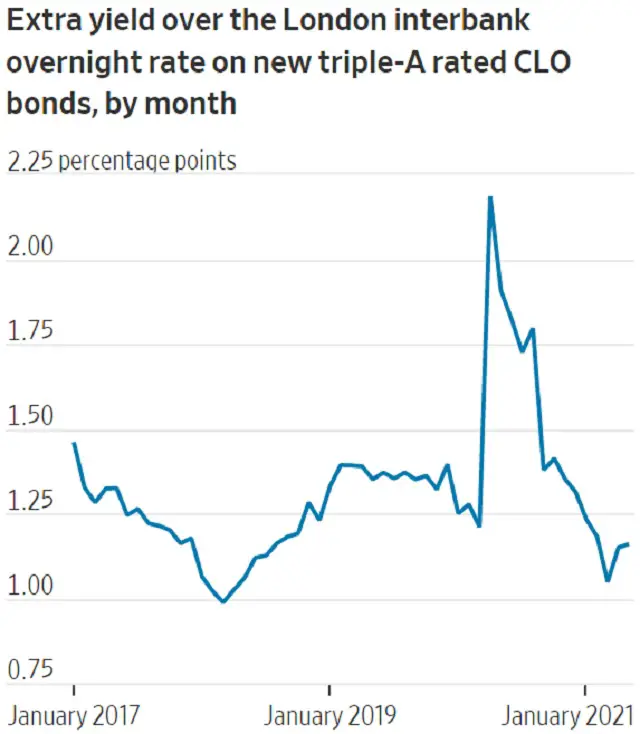

Meanwhile, spreads relative to risk-free paper are shrinking:

Sounds promising, right? And, alas, also familiar. Here’s how CDO’s, the previous bubble’s version of CLO’s, worked just before the bottom fell out in 2008:

Perpetual motion machine

Once they really get going, asset-backed securities like CDOs and CLOs take on a kind of perpetual-motion-machine vibe in which easy money begets even easier money. To the extremely credulous, such a system looks capable of spinning right along forever. Unfortunately, this perception tends to become widespread just as some crucial cog in the machine is about to break.

Which cog will it be? Candidates abound. Interest rates might rise, stocks might tank, the government might realize its policies are stoking instability and try to “taper.” Some crazy geopolitical thing might happen (DO NOT look closely at Palestine, Ukraine, or Taiwan). It doesn’t matter which breaks first, as long as one eventually does.

Then the perpetual motion machine shifts into reverse, with rising defaults causing lower CLO bond ratings causing mass sales by panicked institutions. And so on, until whoever had the guts to short this market cashes out with epic gains.

——————————–

31 thoughts on "CLOs Join The Everything Bubble"

Excellent John, thank you – the ingredients are mixed and the cake is about to be baked IMHO