“Commentary out of the Fed over the last few weeks indicates to me that our central bankers know they are doing far too little, far too late.”

The events in monetary policy over the last few weeks have reminded me of an article I wrote almost 4 years ago to the day, in 2018, called “The Fed Is Gutless And By The Time We Realize, It’ll Be Too Late”.

The point of that article was to note that by the time the Fed felt forced to take decisive action, it would already be too late. I’m reminded of it now a

Last week, St. Louis Fed President James Bullard came right out and said it, calling the Fed “behind the curve”, before qualifying his language. He said that markets pricing in 3.5% rates by 2023 was “a bit slower” than he anticipated, according to CNBC. Bullard also said last week that “inflation is too high” and the Fed needs to act.

“U.S. inflation is exceptionally high, and that doesn’t mean 2.1% or 2.2% or something. This means comparable to what we saw in the high inflation era in the 1970s and early 1980s. Even if you’re very generous to the Fed in interpreting what the inflation rate really is today … you’d have to raise the policy rate a lot,” Bullard lamented.

But reminding everyone that heavy delusion still exists in the world of Central Banking, Bullard said it would be different this time because the Fed has – wait for it – more credibility.

“The difference between today and the 1970s is central bankers have a lot more credibility. In the ’70s, no one believed the Fed would do anything about inflation. It was kind of a chaotic era. You really needed (former Fed Chair Paul) Volcker to come in … . He slayed the inflation dragon and established credibility. After that, people believed the central bank would bring inflation under control,” he said, according to CNBC.

Even uber-dove Federal Reserve Governor Lael Brainard came out to help set the tone last week, commenting that the Fed’s balance sheet runoff will “be rapid”.

“I think we can all absolutely agree inflation is too high and bringing inflation down is of paramount importance,” she said. She said the Fed would raise rates “methodically”, as soon as next month, and will begin to reduce its $9 trillion balance sheet at a “considerably” more rapid pace than last time, according to Reuters.

“We are prepared to take stronger action,” she said, if inflation goals aren’t met.

Federal Reserve Bank of Cleveland President Loretta Mester added to this in late March, along with Federal Reserve governor Christopher Waller.

“In my view, inflation, which is at a 40-year high, is the No. 1 challenge for the U.S. economy at this time,” Mester said in late March, according to the Wall Street Journal.

“Based on my current outlook and my assessment of the risks to the outlook, I believe it will be appropriate this year to move the target range of the fed-funds rate up to its longer-run level, which I estimate to be about 2.5%, and to follow with further rate increases next year,” she commented.

“The data is basically screaming at us to go 50 [basis points]…” Waller also said in late March, before qualifying his statement by saying the Fed was cautious about geopolitical events.

He continued: “I really favor front-loading our rate hikes, that we need to do more withdrawal of accommodation now if we want to have an impact on inflation later this year and next year. So in that sense, the way to front-load it is to pull some rate hikes forward, which would imply 50 basis points or at one or multiple meetings in the near future.”

Finally, minutes from the Fed’s March meeting showed consensus around shrinking the balance sheet by $95 billion per month after a 3 month phase in, and also revealed that many Fed officials would support 50 basis point hikes at upcoming meetings, MarketWatch reported.

One thing is for sure, the talk is getting tough. Will the Fed’s action follow suit?

Well I’ll be damned – we’re getting the ole’ gang back together and everybody is finally getting on the aggressive rate hike bandwagon in unison.

Which, of course, has me fearing that because we are considering it only now, we are already far too late in our attempts to address an inflation problem that has gotten out of hand and can only be corrected by a devastating recession.

The attitude from these monetary policy tacticians over the last couple of weeks has stood at stark odds with the action that they have taken. My guess is that if their words line up directly with their actions in the future, the result will be like that 42 car pile up scene from Bad Boys 2.

Instead of answering to Joe Pantoliano, the Fed will have to answer to the public.

‘What’s your job description? What is your job description,” the public will ask the Fed while the economy lies in ruins in the background.

“Tactical narcotics team! Key word: tactical! Displaying finesse and subtlety in achieving the goal! Tell me gentlemen, what was subtle about your work today? 42 cars – and a boat!”

Despite the fact that everyone all of a sudden seems to think we are behind the eight ball, the Fed’s first opportunity to raise rates in a way that the market was expecting wound up falling short they backed off a 50 basis point hike and only hiked 25 basis points in the face of 7% inflation.

Not only do comments from Fed governors this past month suggest that they know they are behind, they also suggested that they know that not enough was done at the last meeting, and that this likely set them further behind.

The predominant ethos coming from the Fed now, if you ask me, is one of sheer panic. The Fed is coming off like they are scared shitless. And when people are scared shitless, they start to flail wildly.

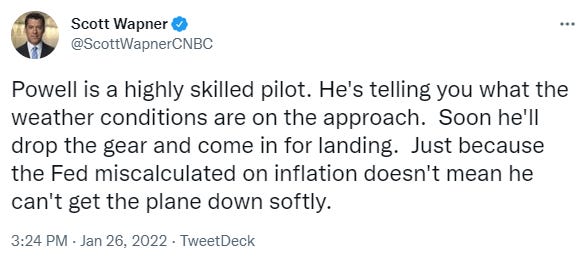

This means the forthcoming “soft landing” that CNBC anchor Scott Wapner was congratulating Jerome Powell for in advance this January could wind up being closer to a four alarm, in-air emergency.

If the Fed is to follow through on what they have been telegraphing over the last few weeks, multiple 50 basis point hikes are going to be on their way, with the next one just days away.

But, to be honest, it almost feels like taking the action of these next few 50 bps hike isn’t even important anymore. It has been well telegraphed and there will be little surprise factor to the markets, which I believe will continue to plunge as rate hike shocks make their way through the pornographic amount of outstanding debt in the system.

What will matter, however, will be how the Fed reacts to the inevitable chaos and volatility that is going to be on its way this year as a result of the hikes.

For the Fed to hold their nerve, it’ll require uncommon constitution and guts. And because the Fed hasn’t had a backbone for the last 20 years, the steadfast nature of how the Fed must hold its nerve in coming months is going to be exponentially more intense than it would have been in years prior. We’ve waited until the last minute and are flying face first into the win.

I was certain the Fed was gutless in 2018.

Has anything changed since then? It’s not likely anything at the Fed has.

But the consequences of avoiding the problem and kicking the can down the road this time are far more near-team and far more profound than they’ve ever been.

——————————–

Steve Jobs’ “Final Prophecy” Now Coming to Life

Steve Jobs’ ability to predict the future was remarkable – Now his “Final Prophecy” is coming to life, with huge implications for you and your money. And that’s exactly why investing legend Joel Litman has just prepared the most fascinating and useful analysis I’ve seen in many years…

3 thoughts on "The Fed Is Scared $h*tless"

Raise rates and QT – stock market crash. Continue QE and hyperinflation. Good luck.

The Fed isn’t gutless, they are fulfilling their final mission – to act as suicide bomber to the US economy. All in an effort to get Klaus Schwab and the New World Order’s “Great Reset.”