Let’s start by sketching out a rough spectrum of the pandemic’s impact on major industries. At the hellish end of this spectrum is hospitality, where cruise ships, vacation resorts, and other crowd magnets have been rendered toxic and therefore useless overnight. Most of these companies will fail and their flagship assets will be repurposed or trashed.

At the other, much happier end of the spectrum are “stay at home” businesses like Amazon, Netflix, and food delivery service Instantcart, which can’t publicly admit to loving the pandemic but would probably not mind if it became the new normal.

In the middle of the spectrum – and therefore tougher to predict – is housing. Specifically, are prices going to plunge or soar in this new world, and how should buyers and sellers behave going forward?

In the last recession, the answer was clear-cut: Houses were the epicenter – in fact the cause – of the crisis, and were going behave the way bubble assets always do.

Home prices ended up falling by 40% in many formerly hot markets, foreclosures soared and banks ended up with mountains of unwanted property that they were legally obligated to unload at fire-sale prices. With hindsight, the obvious strategy was to sell at the bubble peak in 2007 and buy back in at a deep discount a few years later.

This time around housing is collateral damage. It’s expensive in a lot of places – frequently higher than at the previous cycle’s peak. But supply hasn’t run out of control, and pre-pandemic there were widespread house shortages. So a repeat of the previous bloodbath would only make sense in the context of a 1930s-style deflationary Depression – certainly possible but unlikely in a world of negative interest rates and central banks with fiat currency printing presses.

All that being said, it’s still going to be ugly in a lot of housing markets. A global pandemic is not conducive to shaking hands with realtors and touching other people’s doorknobs. An equities bear market, meanwhile, generates the kind of negative wealth effect that makes writing a check for a 20% down payment on a half-million-dollar house even more painful than usual.

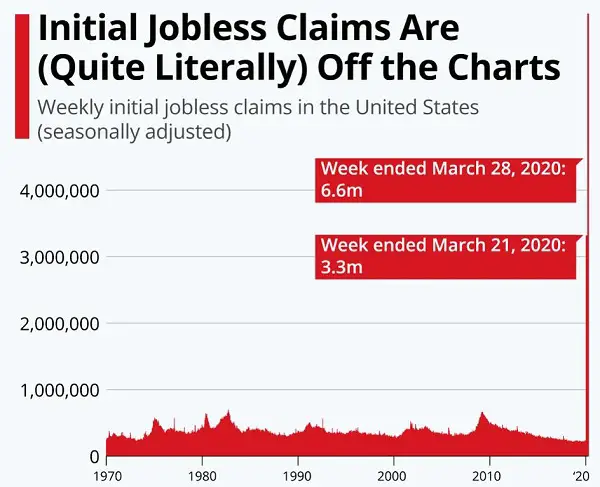

And jobs are evaporating. The past two weeks’ initial jobless claims reports show a staggering 9 million newly unemployed. It’s a safe bet that anyone in that group who was house hunting now has other priorities.

Then there are the people who have a house but virtually no other savings (something like 20% of the population). Once they become unemployed, the occasional government relief check won’t prevent them from having to sell their home to put food on the table. The result: A lot of new housing inventory coming to market.

Last but not least are the people who still have the wherewithal to buy a house but understand what’s coming and are gleefully waiting to toss low-ball-offer hand grenades into the crowds of desperate sellers.

The result: A period of rising inventory and falling prices that produces some serious bargains. Maybe not quite as juicy as the half-off sales in Florida condos and suburban McMansions circa 2010, but still very nice deals compared to the overheated bygone days of last summer.

When will housing statistics start reflecting the coming buyer’s market? Almost immediately:

Housing market shows first signs of trouble from pandemic

(MSN) – March started out as a strong month for the U.S. housing market — but by the second half of the month, the first indications that the coronavirus pandemic would weigh on homeselling activity began to emerge, according to a new report from Realtor.com.

Real-estate firms have taken steps to brace for the impact of the coronavirus pandemic. So-called iBuyers including Zillow (ZG) and Redfin (RDFN) that purchase homes from sellers and then sell them for a profit had wound down their home-buying operations in anticipation of an economic downturn.

Google search activity for “homes for sale” is currently down about 25% from year-ago levels.

Another sign that home sales will slump this spring: Mortgage applications. The volume of mortgage applications for loans used to purchase homes was down 24% compared with a year ago for the week ending March 27, according to data from the Mortgage Bankers Association.

So the top is definitely in. But the bottom is probably a ways off. Government mortgage forbearance will allow people to keep their homes longer than was the case during the Great Recession. This will spread the pain over multiple months (maybe years if forbearance is extended) instead of concentrating it in one big foreclosure spasm.

Housing will likely go through the typical “denial … anger and resistance … panic … capitulation” process, with prices bottoming at maybe two-thirds of their 2019 peaks, but the descent might be slower than last time around.

The takeaway: If you’re a seller, smack whatever bids are out there now. If you’re a buyer, be patient. Bargains are headed your way, but slowly.

9 thoughts on "The Housing Bust Will Take Longer This Time"

Anyone thinking of selling ought to list to sell just below market prices. Be the most attractive home on the market (price wise). Businesses will fail and the market will soon be saturated with inventory. And during that process there will be sellers who will “need” to sell and they will be the ones who will drive the market downward. If the damage is severe then banks will suffer dearly. Rates are already at rock bottom. The FED cannot take them lower. (They’re damned if they do go into negative rate territory and damned if they raise rates. Our economy was very precarious before the Covid-19 pandemic. The pandemic pushed us over the edge. The Trump administration grabbed our economy by the seat of it’s pants (with trillions of salvation) so we now have a precarious economy with new incredible debts. If you own a home with at least an acre of land you may want to keep it. But it won’t help much to own an expensive home, even if yo can pay it off in the future with cheap (inflated) dollars, if you can’t feed yourself. Land with homes are still dirt cheap in the SE of the U.S. And it is land and or gold to invest in. But land can feed you.

I would imagine refinancing will similarly become more attractive as time progresses? As banks become more desperate to execute mortgages?

Or is that false logic?

A surprising optimistic analysis here. I sort of agree, so that’s a problem.

In 2009 I didn’t think the central banks would be successful in bailing out and reflating things (yet again) but I was wrong. So – having learned my lesson (“never fight the Fed” – lender of last resort and counterfeiter if necessary) – I think they’ll be successful once again. I now understand that all things financial can be solved by bail outs. The so-called psychologically important $20 trillion national US debt didn’t even register a few years ago, and now at $22 trillion and the prospect of permanent multi-trillion dollar deficits indefinitely, even JR et al are talking about a more gradual and less severe drop in housing than last time. It’s so crazy he’s probably right.

I know a lot of articles are warning about “bear market traps” and an overdue mega-cyclical blah, blah, blah but I don’t think that will happen, and that’s why I’m worried.

Yea right. Liquidity is everything when the Fed can print trillions of dollars and there are willing foreign dollars-takers, else trillions of dollars circulate in US and create hyperinflation. Coronavirus greatly disrupt millions of china’s factories. China exports much less, take much less dollars. Also, China already stopped allowing foreign tourists into China starting 3/31, so those millions of potential tourists can’t spend their dollars in China. The point of China disallowing foreign tourists into China is to stop importing inflation from EU and US. Beside, China already accumulate too much Dollars and Euros already, why in the world Chinese leaders allow the dollar and Euro to be Chinese people’s company stores with polluted air, etc. In fact, Chinese leaders will use resurgent Coronavirus to close factories, to export much less, to produce enough for their people. Wake up and smell the coming spectacular, unreal US economic collapse.

I’ll believe it when I see it. The problem with bashing the US is everybody forgets that every other industrialized country is even worse off, including their currencies (and even Germany as long as it’s part of the EU). If the dollar does collapse it will be the last one to do so.

Jeeze, at no time I was bashing the US or the US dollar, at no time I said: the dollar will collapse. I just laid out the obvious points: No country, No leader will allow it’s people to work so hard to produce goods, deplete raw materials, mines in exchange paper currencies from other countries for eternity. Never. Why in the world China keeps running trade surplus with US and EU for eternity and accumulate trillions and trillions of Dollars, Euros and destroy their environment, accept higher oil price in the process? Unless, people put their heads in the sand, and can’t see what’s going on? i believe This is it. From now on, China will use resurgent coronvirus as excuses to shut down factories at will, and to run a balance trade with the US, EU. US GDP can’t have 70+% consumer spending forever. It’s time to reckon with realities.

about currency exchange is a giant scam. before currency exchange trading was born, countries was trading perfectly. Currency exchange trading is the most effective for 1 country to rob another county of their labor. FYI, in 2018 China banned recyclable trash, then Vietnam, Malaysia, Singapore, Thailand, Cambodia, Indonesia, Fillippine immediately followed. Consequently, the recycle industries in USA, Canada, EU are now in crisis.

https://www.youtube.com/results?search_query=China+ban+trash

https://www.youtube.com/results?search_query=indonesia+ban+trash

etc

these exporting countries will follow China and use Coronavirus as excuses to shut down factories at will.

stop comparing now and 2008. In 2008, China was much weaker and poorer country with great majority of population was living under poverty line, Chinese leaders had no choice but to play along. Now, something like under 1% of China population is living under poverty line. Nobody, no leader, no country is stupid enough to have their people work hard to produce goods, pollute their country’s environment, then to take paper currency from other countries. Beside, they produce less, the import oil less, and that results much cheaper oil for China and Chinese people.

not fast enugh