Turning points in a financial system usually occur in discrete phases. At first, new information that contradicts existing preconceptions is dismissed as unimportant. But as more such data accumulates, a growing number of people come to expect the new trend to continue. In economist-speak, “expectations” change, and these become self-fulfilling prophecies, as people start behaving in ways that anticipate — and thus cause — more of the same.

Inflation is a classic example. When the cost of most things has been flat for a long time, a few scattered price increases don’t change any minds. But when lots of things start costing more, everyone eventually decides that prices are rising generally and begin buying in anticipation, whatever the current price, which in turn causes prices to rise even faster.

This kind of data-driven perceptual shift is now occurring in a lot of different places.

In US housing, Reuters just conducted a poll of property market analysts to see what they think home prices will do in coming years. Turns out – not really surprising given the recent surge back to 2006 bubble levels – that they expect home prices to outpace both overall inflation and wage growth for at least the next few years.

U.S. house prices to rise at twice the speed of inflation and pay: Reuters poll

An acute shortage of affordable homes in the United States will continue over the coming year, according to a majority of property market analysts polled by Reuters, driving prices up faster than inflation and wage growth.

After losing over a third of their value a decade ago, which led to the financial crisis and a deep recession, U.S. house prices have regained those losses – led by a robust labor market that has fueled a pickup in economic activity and housing demand.

But supply has not been able to keep up with rising demand, making homeownership less affordable.

Annual average earnings growth has remained below 3 percent even as house price rises have averaged more than 5 percent over the last few years.

The latest poll of nearly 45 analysts taken May 16-June 5 showed the S&P/Case Shiller composite index of home prices in 20 cities is expected to gain a further 5.7 percent this year.

“We are not seeing a temporary phenomenon. House prices have been outrunning family incomes for several years in the U.S. and while demand has cooled off a bit, the supply side is still very tight,” said Sal Guatieri, senior economist at BMO Financial Group.

“I think house prices will continue to outrun family incomes for at least another year and it will take some time for demand to slow and to some extent supply to increase.”

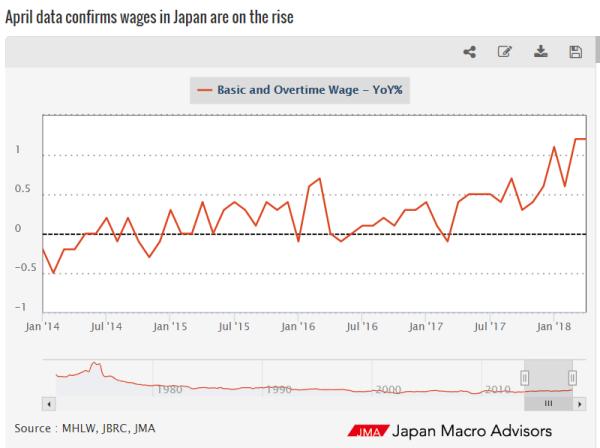

Meanwhile on the other side of the world expectations for Japanese wages have shifted dramatically:

(Japan Macro Advisors) – The April wage report was consistent with our view that wages in Japan are finally on the rise. The preliminary estimate for the month showed that regular wages in Japan rose by 1.2% year on year (YoY) in April, continuing to rise at the highest rate of increase since July 1997. There have been a few false dawns for wage inflation, but the current upturn seems to be the real one, in our view

US home prices and Japanese wages are of course two very different, seemingly unrelated indicators. But that’s what makes their simultaneous increase so telling. Easy money around the world is affecting different sectors in different ways. But more and more of them are starting to move in the same direction.

As the “prices are rising” signals become louder, more people will stop seeing each as a one-off event and start viewing them as confirmation of a broader trend.

Should this happen, central banks – which see “inflationary expectations” as one of the things they’re supposed to “manage,” will feel obligated to try to curb the growing mindset. The Fed is already behaving this way, while the European Central Bank is now “debating the timetable for ending QE.”

Let Japanese wages stay on the current trajectory for just a little while longer and the Bank of Japan will probably follow. Which leads to a classic tightening cycle with bubbles bursting all over the place.

5 thoughts on "Inflation Is Back, Part 6: More People Now Expect Higher Prices"

At least as I see it – the “old preconceptions” were that the Fed is going to screw things up, fiat currencies are doomed, government debt levels will hit the wall causing interest rates to rise “naturally” (i.e, due to market forces not central bank finagling), general debt levels will clog the system and slow economic growth, bankruptcies and defaults are around the corner, and inflation will rise because of so much fiat money creation (e.g. QE).

The knew “acceptance” now seems to be fiat currencies are as stable as ever, the US dollar is king again, debt levels don’t matter nearly as much as previously feared, inflation may finally be rising to 2% per annum as the CB’s want and that’s okay so the CBs won’t tighten, economic growth is accelerating, etc. If so, as crazy as it sounds and if JR’s thesis holds, ‘we ain’t seen nothing yet.’

Time to normalize interest rates. Ooops! Can’t do it, too much debt.