Guest post by Michael Lebowitz from Real Investment Advice:

The Bank of England is bailing out U.K. pension funds. The Bank of Japan uses excessive monetary policy to protect its currency and cap interest rates. China encourages its banks to buy stocks. The dollar, the world’s currency, is on a tear, interest rates are surging, and the financial world is fracturing.

Unlike any other currency, the U.S. dollar drives the global economy and financial markets. Because of the dollar’s status as the world’s reserve currency, the Fed’s monetary policy actions play a critical role in steering the U.S. economy and all global economies and financial markets.

To foresee the next crisis, it is imperative to understand the dollar’s role in global finance and economics and the resulting role that the Fed plays in influencing international monetary policy. To do so, we start with insight from Triffin Warned Us, an article we published in 2018.

These “cliff notes” for the article lay the groundwork for Part 2. Following this article, we will discuss the risks investors face as the Fed attempts to quell inflation.

The Bretton Woods Agreement

In 1944, the United States and many nations forged a significant financial arrangement in Bretton Woods, New Hampshire. The agreement has paid enormous economic dividends to the United States. However, it has a flawed incongruity with a dear price that is rearing its ugly head today.

Per the terms of the 1944 Bretton Woods Agreement, the U.S. dollar supplanted the British Pound to become the world’s reserve currency. The agreement assured a large majority of global trade would occur in U.S. dollars, regardless of whether the United States was participating in such trade. Additionally, it set up a system whereby other nations would peg their currency to the dollar. This arrangement is akin to the global currency concept made popular by John Maynard Keynes. Keynes’s brainchild was Bancor, a supranational currency.

Within the terms of the agreement was a supposed remedy for one of the abuses that countries with reserve currency status typically commit, running continual trade and fiscal deficits. The pact discouraged such behavior by allowing participating nations to exchange U.S. dollars for gold. Therefore, other countries that were accumulating too many dollars, the side effect of American trade deficits, could exchange their excess dollars for U.S.-held gold. As a result, a rising price of gold, indicative of a devaluing U.S. dollar, would be a telltale sign that America was abusing her privilege.

London Gold Pool

The agreement started fraying shortly after. In 1961, the world’s leading nations established the London Gold Pool. The objective was to fix the price of gold at $35 an ounce. The action was an attempt to maintain the Bretton Woods status quo. By manipulating the price of gold, an important gauge of the size of U.S. trade deficits was broken. Therefore, there was less incentive to swap dollars for gold.

Seven years later, France broke the ranks. France withdrew from the Gold Pool and demanded large amounts of gold in exchange for dollars. As a result, in 1971, President Richard Nixon, fearing the U.S. would lose its gold, suspended the convertibility of dollars into gold.

From that point forward, the U.S. dollar was a floating currency. There was no longer the discipline imposed upon it by gold convertibility. Nixon’s actions essentially annulled the Bretton Woods Agreement.

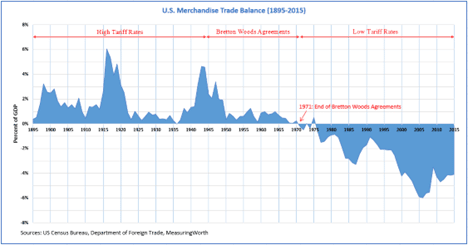

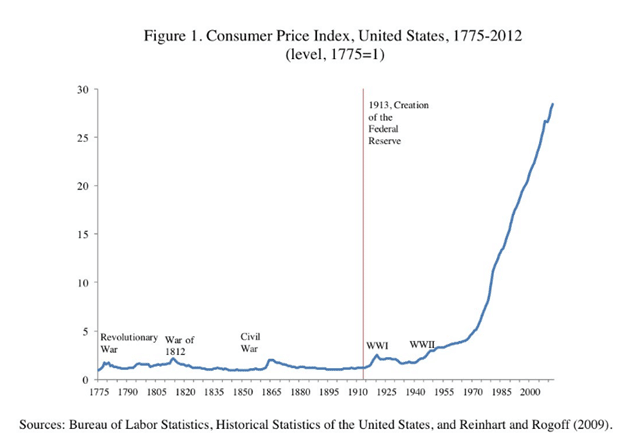

The following decade saw double-digit inflation, persistent trade deficits, and weak economic growth. These were signs that America was abusing its privilege as the reserve currency. The first graph below shows that, like clockwork, the U.S. began running annual trade deficits in 1971. The second graph highlights how inflation picked up markedly after 1971.

By the late-1970s, Fed Chair Paul Volcker raised interest rates from 5.875% to nearly 20.00% to break inflations back decisively. While economically painful, Volcker’s actions not only ended ten years of persistently high inflation and restored economic stability but, more importantly, satisfied America’s trade partners. The now floating rate dollar regained the integrity required to be the world’s reserve currency. This was despite lacking the checks and balances imposed upon it by the Bretton Woods Agreement and the gold standard.

Our article The Fifteenth of August discusses how Nixon’s “suspension” of the gold window unleashed the Federal Reserve.

Enter Dr. Triffin

In 1960, 11 years before Nixon’s suspension of gold convertibility and the effective demise of the Bretton Woods Agreement, Robert Tiffin foresaw this inevitable problem in his book Gold and the Dollar Crisis: The Future of Convertibility. According to his logic, the privilege of becoming the world’s reserve currency would eventually carry a heavy penalty for the U.S.

At the time, few paid attention to Triffin’s thesis. However, he was invited to a congressional hearing of the Joint Economic Committee in December of the same year.

What he described in his book and Congressional testimony became known as Triffin’s Paradox. Events have played out primarily as he envisioned.

Essentially, he argued the reserve status forces a good percentage of global trade to occur in U.S. dollars. For trade and global economies to grow under such a system, the U.S. must supply the world with U.S. dollars.

To supply the world with dollars, the United States must consistently run a trade deficit. Running persistent deficits, the United States would become a debtor nation.

Foreign Creditors Enable U.S. Deficits

Foreign nations accumulate and spend dollars through trade. They keep extra dollars on hand to manage their economies and limit financial shocks. These dollars, known as excess reserves, are invested primarily in U.S.-denominated investments ranging from bank deposits to U.S. Treasury securities and a wide range of other financial securities. As the global economy expanded and more trade occurred, additional dollars were required. As a result, foreign dollar reserves grew and were lent back to the U.S. economy.

Making the world even more dependent on the dollar, many foreign countries and companies issue U.S. dollar-denominated debt to better facilitate trade and take advantage of America’s liquid capital markets.

The arrangement benefits all parties involved. The U.S. purchases imports with dollars lent to her by the same nations that sold the goods. Additionally, the need for foreign countries to hold dollars and invest them in the U.S. results in lower U.S. interest rates, further encouraging domestic consumption and providing relative support for the dollar.

For their part, foreign nations benefit as manufacturing shifted away from the United States to their countries. As this occurred, increased demand for their products supported employment and income growth, thus raising the prosperity of their respective citizens.

A Win-Win or a Ponzi Scheme?

While it may appear the post-Bretton Woods covenant is a win-win pact, there is a massive cost accruing to everyone involved.

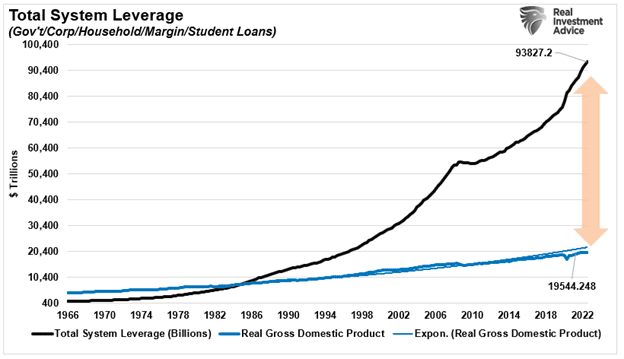

The U.S. has too much debt. As such, it has become increasingly dependent on low-interest rates to spur debt-driven consumption and to pay interest and principal on existing debt.

Lower than appropriate interest rates lead to unproductive debt, as can be seen with debt outstanding rising at a much faster pace than GDP. Simply the growing divergence between debt and the ability to pay for it, GDP, is unsustainable.

Summary

Triffin’s paradox states that with the benefits of the reserve currency also comes an inevitable tipping point or failure.

As we see with the current instance of rising interest rates and inflation, that point of failure is closing in on the U.S. and the rest of the world.

Part two of this article will focus on the dollar and Fed monetary policy and what it may entail as the Fed continues to push interest rates higher.

Guest post by Michael Lebowitz from Real Investment Advice.

How to Own Tens of $Billions in Gold for Just US$1 Per Share

A brand new gold bull market has arrived as nervous investors continue to flock to the safety of the yellow metal.

Yet, the biggest gains won’t be in gold…they’ll be in select gold stocks with proven ounces in the ground.

This soon-to-be-known gold company provides investors with exposure to over 30 million ounces of gold…worth tens of $Billions…at a ridiculously low US$1 per share.