Written by Bryan Lutz, Editor at Dollarcollapse.com:

The Fed’s regional banking crises is becoming a perennial problem.

Here’s what they’ll do to “fix it.”

About this time last year we saw the demise of Silvergate Bank, Silicon Valley Bank, Signature Bank, and First Republic Bank…

So far this year, New York Community Bank has been the only bank that’s made the news headlines.

Its poor financial performance was caused by losses from two Commercial Real Estate loans acquired from Signature Bank…

Among other bad debt…

The thing is, this is happening across board…

Pam and Russ Martens over at WallStreetonParade dot com identified a several other failing banks:

US Bancorp (5th largest bank) “…has lost over 30 percent of its market value in the past two years.”

KeyBank (22nd largest bank) “…has lost 50 percent of its value over the past two years.”

Comerica (32nd largest bank) “…has lost 50 percent of its market value in the past two years.”

Western Alliance Bank (35th largest bank) “…have lost 45 percent of their market value.”

Valley National Bank (37th largest bank) “…has lost 43 percent of its common stock market value in the past two years.”

And First Foundation Bank “…has seen its share price lose 70 percent of its market value in two years.”

If or when New York Community Bank fails…

Or when one of the above banks becomes insolvent… It will be because of two things:

1. Bad debt maneuvering (bonds)

2. Commercial Real Estate losses

A surprising amount of Commercial Real Estate loans are held by regional banks in the United States…

Reuters reports:

Real estate pain for US regional banks is piling up, say investors

“NYCB’s recent earnings release which sparked a dive of about 60% in its shares has particularly focused investors on combing through portfolios of regional banks, as small banks account for nearly 70% of all commercial real estate (CRE) loans outstanding, according to research from Apollo.”

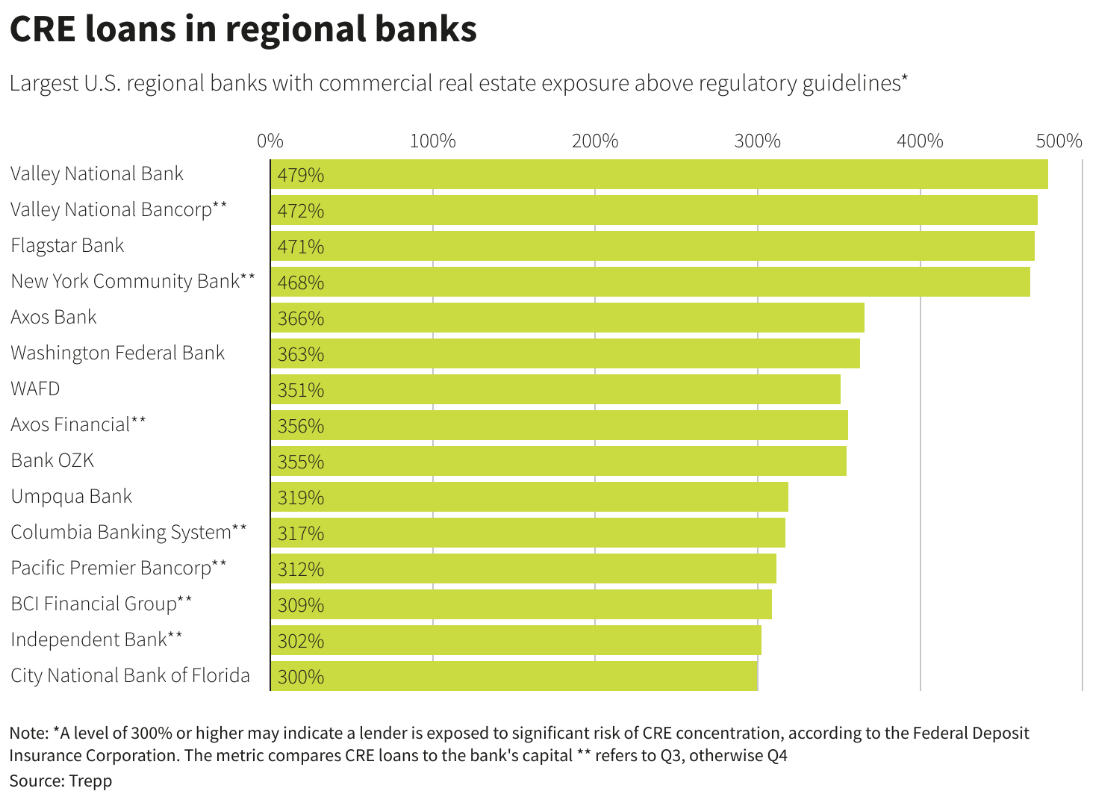

Among the banks at highest risk from CRE loans are:

As long as rates stay where they are, banks holding large amounts of real estate, particularly those with exposure above regulatory guidelines will continue to see losses.

And as losses continue to mount, more banks will perennially “pop up” into the headlines.

In order to save these banks, the Federal Reserve will choose to “fix it” by printing more money to prevent instability in the banking system and wider economy…

Here’s what they’ve been doing so far…

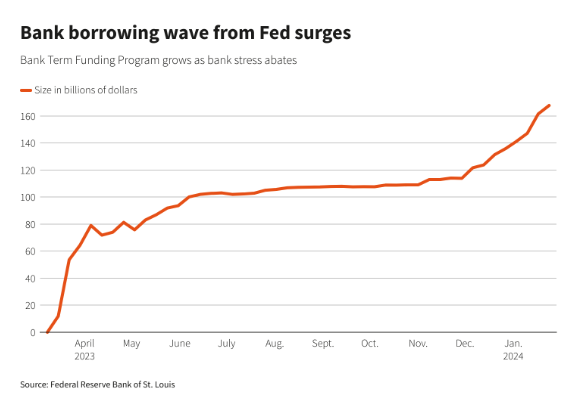

To save the loss of bad financial assets, the Fed created the Bank Term Funding Program(BTFP).

Basically, it is a slush fund banks can tap in to when running losses, but instead has been abused as an arbitrage opportunity by banks to get ahead.

So they are shutting it down as of March.11, 2024 to create more stability with another program, the Federal Reserve’s discount window.

Bloomberg reports:

US Prepares Rule Forcing Banks to Tap Fed Discount Window

“US regulators are preparing to introduce a plan to require that banks tap the Federal Reserve’s discount window at least once a year to reduce the stigma and ensure lenders are ready for troubled times…

Borrowing from the discount window, which dates back to the Fed’s creation in 1913, has often carried a stigma. The Fed itself discouraged borrowing from the facility for long periods throughout its history, and banks were reluctant to use the facility, ostensibly for institutions on the brink of insolvency, for fear that investors would see it as a sign of operational weakness.”

So most banks have avoided using the discount window for fear of appearing insolvent.

No one wants to be the guy causing the stock to drop.

Instead, this new program will implement perpetual borrowing to expand the Fed’s perennial problem…

Regional(even some national) banks constantly on the edge of insolvency.