“Like A Lot Of Things In Life, We Laugh Because It’s Funny And We Laugh Because It’s True.”

— Al Capone, The Untouchables (1987)

—

Written by Bryan Lutz, Editor at Dollarcollapse.com:

One of the first crime novels I read was ‘Wise Guy.’

Maybe wise because they chose the untouchable life…

A life where one became a “made man.”

All you needed (but not required) was a Sicilian heritage, a history of crime, and loyalty to the Omerta (the mafia code of silence).

It just took time… When you paid your dues, you were in.

Then you get protection, for life. Kapeesh?

Well, if you saw trouble coming, a hard life, and you were already on the lower-end of society…

Would you choose a way out? If it were all legal?

Wouldn’t you want to be “untouchable?”

Well, you can.

The current economic system’s been set up so you can.

After spending your life paying taxes, and witnessing inflation driven by printing money, you’ve earned your dues.

You get protection AND lifelong membership.

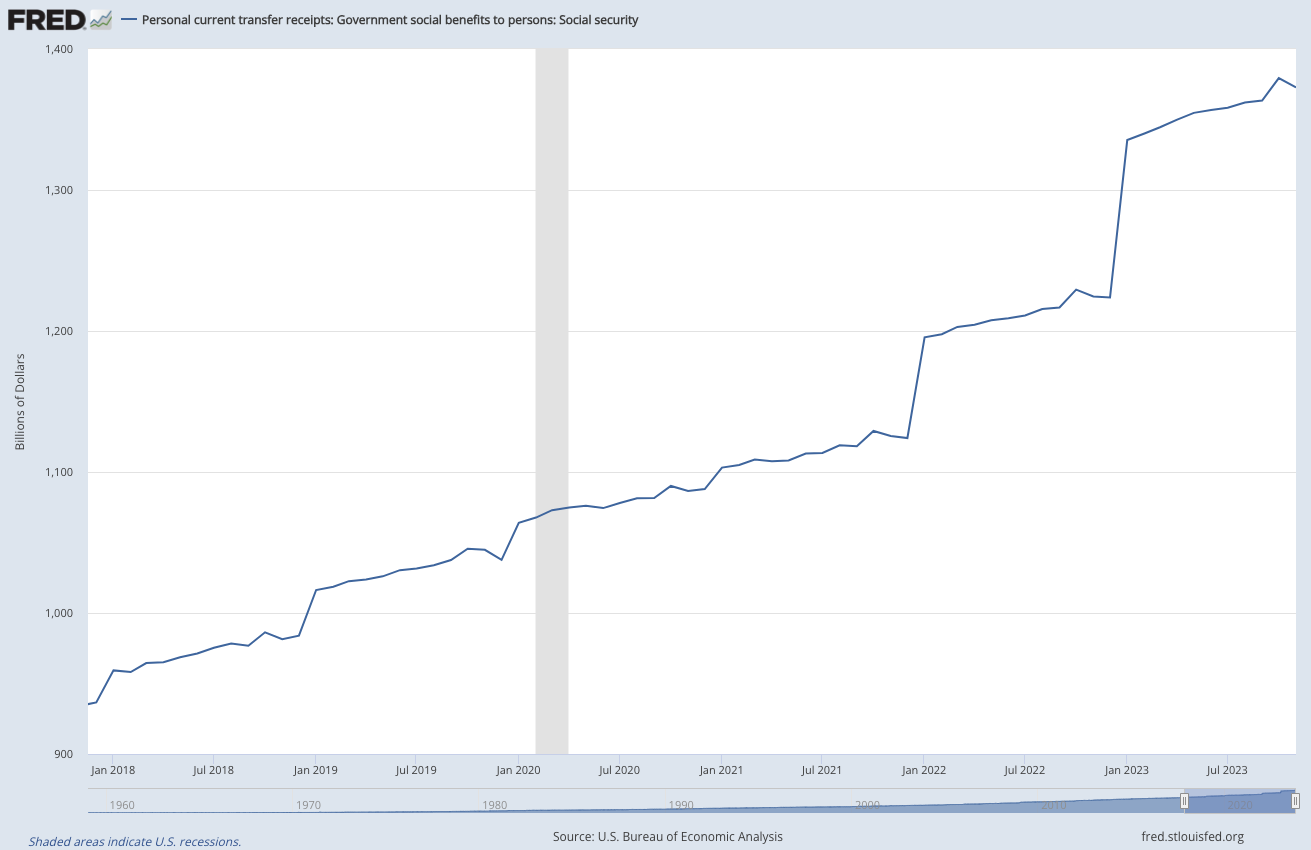

Millions of Americans are already choosing to become untouchable. They’re cashing in on the government’s guaranteed inflation hedge, without spending any investment money of their own.

You get social security payments.

The DailyMail reports:

Social Security payments will rise by 3.2% this year

“Increased Social Security payments for 66 million Americans began rolling out this month and will continue throughout January.

Compensating for inflation, a 3.2 percent cost-of-living adjustment (COLA) will be applied to Social Security checks.

That means in 2024 the average retired worker can expect to net $1,907 a month, up from $1,848 last year, according to the latest Social Security Administration (SSA) Fact Sheet…

This year’s hike was significantly smaller than in the previous two years – 5.9 percent in 2022 and an unprecedented 8.7 percent a year ago.

On average the benefit has increased by 2.6 percent each year for the past 20 years.”

Over the past twenty years, social security has risen on par with inflation. Even during the massive inflation generated by pandemic printing in 2021 and 2022.

It’s a rough working to pay off a mortgage your whole life, and since massive pandemic money printing has boosted home prices that extra increase could go towards retirement.

That could be what many are thinking.

Millions of Americans already decided it was time to exit the workforce in January 2021, and 2022, but can you blame them?

No.

Costs are skyrocketing. You’ve only got so many years left. You only need a certain standard of living. And if your home is paid off you can always give it a sell, and move to a small town in the mid-west. If the government is matching inflation, why not?

Forbes gives us some insight.

Why Are So Many Americans Choosing To Retire Earlier Than Planned?

“The rise in household wealth among affluent Americans, increasing home prices, a surging stock market, workplace health and safety concerns, and pandemic fatigue have all played a role in driving this increase. Burnout has also played a role, leading employees across all age groups to leave the workforce in what has been coined “the great resignation.”

According to a survey conducted by Indeed, more than half (52%) of respondents said they experienced burnout and 67% said feelings of burnout had worsened over the course of the pandemic.”

Why try to keep up when you’ve heard the stories of grandparents living below their means because they MUST?

And you’ve worked your whole life for your mortgage?

And you read headlines about millennials and young people struggling…

You know it’s not the same.

Bloomberg reports:

US Consumer Borrowing Surges on Jump in Credit-Card Balances

“US consumer borrowing surged in November by the most in a year on a jump in credit-card balances as the holiday-shopping season kicked into high gear.

Total credit rose $23.8 billion after rising a revised $5.8 billion in October, according to Federal Reserve data out Monday. The figure well exceeded the highest estimate in a Bloomberg survey of economists, which had a median forecast of $8.6 billion.

Revolving credit outstanding, which includes credit cards, increased $19.1 billion in November, the most since March 2022. Non-revolving credit, such as loans for vehicle purchases and school tuition, climbed $4.6 billion. The figures aren’t adjusted for inflation…

New York Fed data also showed the rate of credit-card debt becoming newly delinquent rose in the third quarter. The increases were largest for millennials, or those born between 1980 and 1994, as well as people who also have auto loans and student debt.”

It’s a frightening thought, but at some point, the system won’t be able to sustain itself.

Made-men, retired men and women won’t be untouchable anymore because there’ll just be less to give.

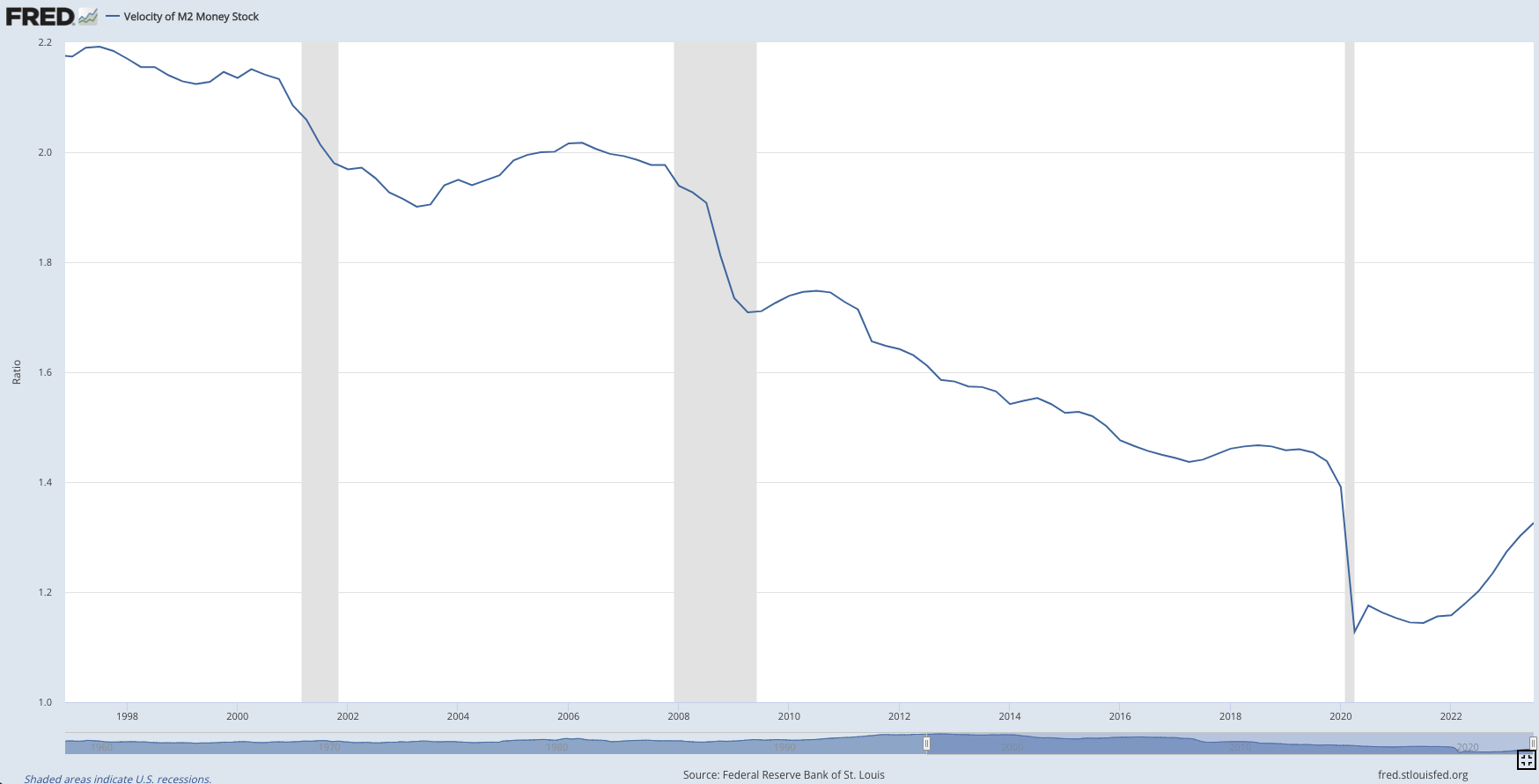

Because their protection comes from something natural law will eventually correct: Fiat money.

And much of the fiat money in the world isn’t being exchanged for anything of real value. More money is being printed unattached to any real value.

Take a look at the decline in the velocity of money, which is the rate at which money is exchanged for goods or services.

And that means less purchasing power for the untouchables on social security.

You see, in a fiat system, money must be created at par with market value. Otherwise, you get too much misallocated supply, and the economy gets bloated… Leading to what’s called The Money Bubble.

Unfortunately, as more people choose retirement, resignation, or job loss occurs, money will need to be printed for the untouchables of the United States until…

There are no longer any untouchables.

An interesting answer to this proposition will be to see whether or not this trend continues this January, and for how long.

Your thoughts?

2 thoughts on "The Untouchables: Will this January See More Millions of Americans Claim their Inflation Hedge?"

My wife and I just bought a 800k house. In Texas thats a lot of house. Our bet is that we will be paying off the mortgage for pennies on the dollar. Wish us luck!

Inflation is good for you then, Mark. Thanks for sharing.