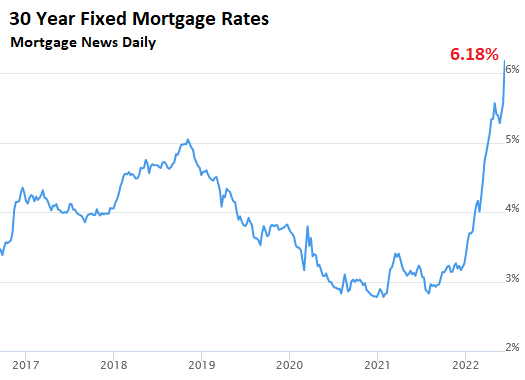

Aside from the sheer magnitude of the spike, this was also the highest mortgage rate since collection of the daily data began in April 2009. This was lightning fast, with mortgage rates nearly doubling since the beginning of the year. Something has to give. And it’s going to be price….

by Wolf Richter on Wolf Street:

The average 30-year fixed mortgage rate today spiked to 6.18%, from 5.85% on Friday, according to the daily index by Mortgage News Daily. (Chart via Mortgage News Daily):

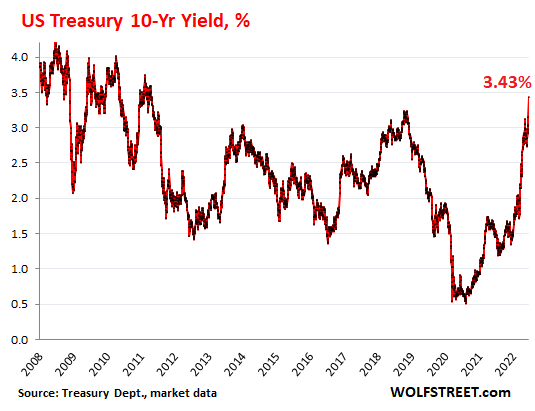

Mortgage rates follow the 10-year Treasury yield, but there is a spread between them, and the spread varies. The 10-year Treasury yield spiked by 28 basis points today, to 3.43% at the close, a huge move, and the highest since April 2011:

But wait…

Back in the day, before QE and interest rate repression, 6% mortgages were considered low, I mean super-low, and I thought I got a great deal with my 15-year mortgage in 1989 at 8%! There are folks here that remember 15% mortgage rates. We didn’t even see 6% 30-year mortgages until 2002.

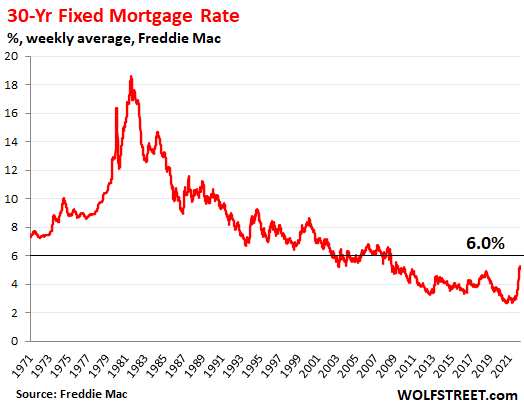

Freddie Mac’s data goes back to the early 1970s (though the June 9 release lags today’s daily measure by about a week). It shows just how fast mortgage rates have bounced off from record low levels, and how comparatively low they still are:

So let’s see. The Greenspan Fed ginned up the idea to cut interest rates following the dotcom bust to create a housing bubble in order to take over from the imploded stock market bubble. This worked, and we got a housing bubble, to which the Fed responded by raising interest rates again to over 5%, which worked and caused the housing bubble to implode, which triggered the mortgage crisis, which performed a rug-pull under the over-leveraged banks, upon which the Fed rolled out its new dual-weapon QE and 0% interest-rate policy, which worked, and it inflated all asset prices, bailed out the bondholders and stockholders of the banks, and soon it triggered the next housing bubble, but much more magnificent than anything before, etc. etc.

You know the drill. But this time, we got a new thingy: Raging consumer price inflation, like we haven’t seen in 40 years, and all bets are off. Raging inflation does a lot of long-term damage to the economy, to the currency, to businesses, and to the people, and it’s time to crack down.

Well, not really cracking down, just slowly raising short term policy rates from near 0% to still very low levels, and ending QE finally, and slowly starting QT.

So that’s not really a crackdown, but seeing how massively markets have reacted to this little bitty policy action shows just how overinflated all assets have become, thanks to 12 years of QE and interest rate repression – 12 years of Fed policy errors – and how hard it will be to unwind all this craziness back to some normalcy. But inflation is now raging, and all bets of a Fed put are off.

After 12 years of money printing and interest rate repression, home prices have ballooned to the point where higher mortgage rates have a very different impact than they had back in the day.

Each time mortgage rates rise just a little at current prices, they take a new layer of potential buyers out of the market. And transaction volume sags, and homes begin to sit on the market, and inventory is piling up. So it cannot happen here, they say, but it’s already happening, even in May before the current spike in mortgage rates, as inventories jumped in amid price reductions and sagging sales, because there is one way for sellers to nail down a deal: Cut the price enough to where the next buyers can afford the mortgage.

Enjoy reading WOLF STREET and want to support it? Click on the beer and iced-tea mug to find out how:

Bear Market Opportunities…

Bear markets typically begin when investors lack confidence in a market and believe that prices will continue to fall. But these markets also provide incredible opportunities to accumulate assets that are trading at a huge discount.

Just like these 3 opportunities right here.