Written by Bryan Lutz, Editor at Dollarcollapse.com:

For the past month, Jerome Powell and the rest of the PhD economists inside the Eccles Building have been hustling behind closed doors…firing billion-dollar shots of liquidity at banks to keep them from defaulting on their loans. And that means, many banks aren’t able to meet their obligations. That’s why Wednesday’s split FOMC decision became inevitable.

On December 10, 2025, the Federal Reserve cut its benchmark interest rate by 25 basis points to a range of 3.50%–3.75%. It was the third consecutive rate cut of the year. Inside the pristine white walls of the Eccles Building, this was almost certainly a contentious debate. Some officials likely argued for lower rates to support economic growth. Others pointed directly at the banks and their declining liquidity.

But here’s the problem: interest rates are supposed to serve the Fed’s dual mandate—price stability and maximum employment.

This time, the decision was clearly made outside that mandate.

The Fed is no longer focused on achieving an economy that grows faster than the national debt. It isn’t even pretending to prioritize price stability or employment. Instead, the Fed is focused on one thing: holding the financial system together at any cost.

The final vote: 9–3 in favor of lowering rates.

The official rationale likely masked the real concern: “If we lower rates, maybe we won’t have to print money directly for the banks.” In other words, a desperate attempt to avoid more overt bailouts through the Standing Repo Facility (SRF), even though the Fed had already injected hundreds of billions into the banking system over the preceding month.

The Stealth Bailout That Few Noticed

WebProNews reports:

Fed’s Stealth $125B Bank Bailout: Liquidity Crunch or Hidden Easing?

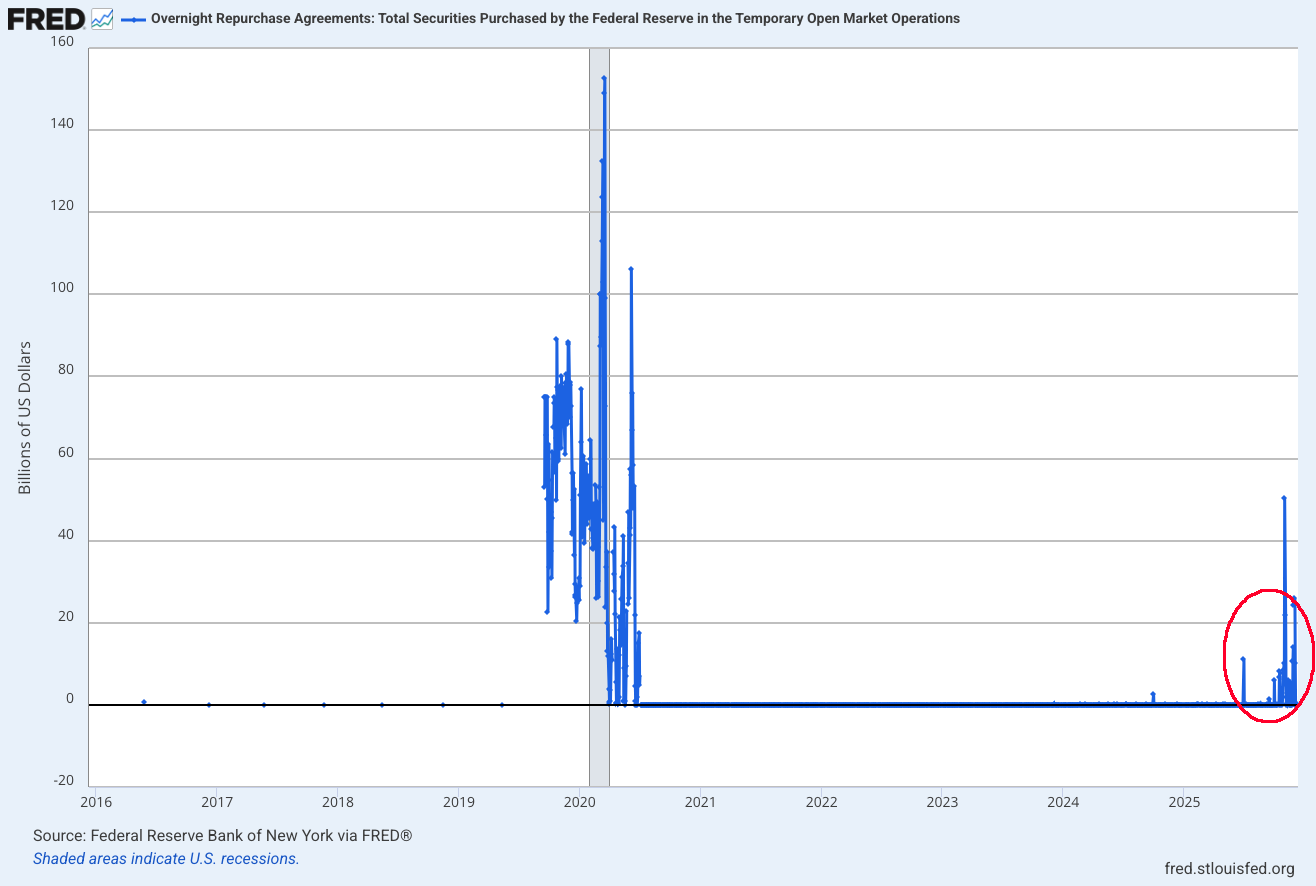

“In the waning days of October 2025, the Federal Reserve executed a series of overnight repurchase agreements that injected a staggering $125 billion into the U.S. banking system over just five days. This move, largely under the radar, culminated in a single-day record of $29.4 billion on October 31, marking the largest such operation since the 2020 pandemic. According to reports from The Economic Times, banks exchanged Treasuries for cash to alleviate funding pressures amid dwindling reserves.

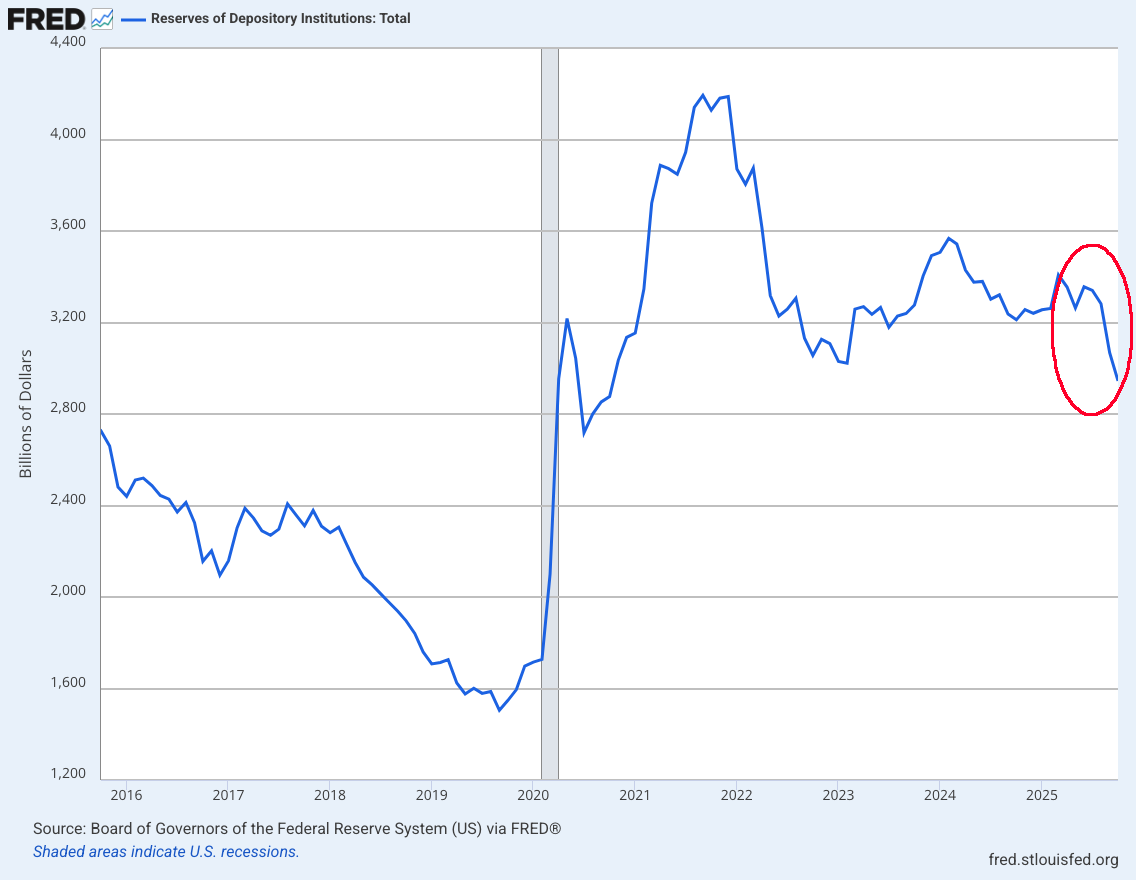

U.S. bank reserves have plummeted to $2.8 trillion, the lowest level in four years, as confirmed by official data from the Federal Reserve Economic Data (FRED). This sharp decline echoes the liquidity strains of 2020, when reserves similarly tightened, prompting emergency interventions. The Fed’s actions, while not outright quantitative easing, have been dubbed ‘stealth easing’ by market observers, as Chair Jerome Powell maintains a hawkish stance on inflation.”

The troubling part is that bank reserves were collapsing at the same time the Fed was cutting interest rates.

The Return of the Standing Repo Facility

So in late October and throughout November, the Fed hit one of their red buttons and began using something they haven’t used since the pandemic. Without announcement, the Fed began purchasing securities from banks through their Standing Repo Facility(SRF).

Faced with falling reserves and rising funding stress, the Fed quietly reached for one of its red-button tools called the Standing Repo Facility (SRF). Used heavily during the pandemic, it had been set aside for years.

Until now.

Through late October and November, the Fed began buying securities from banks again through the SRF—with no announcement. It was an emergency maneuver designed to keep banks liquid.

Now, in December, the Fed is not only cutting rates but openly signaling that more of these operations are coming.

Seeking Alpha reports:

FOMC December 2025: $40B In 30 Days – The Fed Knows Something You Don’t

“The Standing Repo Facility (SRF) is a long-term facility through which the Federal Reserve offers overnight liquidity to the market when banks are finding it hard to obtain funding. The SRF hasn’t been used much in the last few years but it has come back to life and was in fact activated 16 out of 26 days in the weeks before the meeting.”

The $40 billion in Treasury bill purchases starting December 12 is framed as “reserve management,” but that is cover for cracks in the banking system, and the system as a whole. When the Fed needs to inject liquidity at this scale to prevent market dysfunction, it signals that leverage (bank’s loans, derivative risk, and the inability of the bank to back their own loans) is unwinding. Counterparty risks are rising for banks.

What Comes Next: Larger Interventions and Faster Debasement

The logical conclusion is unavoidable:

More interventions are coming and they will likely be larger than planned.

And the burden will fall on the U.S. government and the Federal Reserve to provide whatever funds are necessary to keep the banking system afloat.

That means:

- accelerated national debt,

- accelerated liquidity injections,

- and accelerated currency debasement.

The Fed is no longer operating within its mandate.

It is operating in panic mode… Fighting to prevent systemic collapse. At the same time, they’re hoping the public doesn’t notice what’s happening behind the white walls of the Eccles Building.

8 thoughts on "The Fed is in Panic Mode, No Longer Functioning On Its Mandate"

Yes, in full agreement hard assets, Bullion & property is what will protect wealth values against inflationary monopoly money.

Appreciate your feedback, Ben.

Save, save SAVE … but save in ‘ounces’ not ‘dollars.’

What’s a ‘dollar’ anyway but a dubious unit of account that’s lost 97% of its value in the last 55 years.

THE ‘DOLLAR’ CANNOT BE TRUSTED.

Rather, the objective value inherent in both metals (Gold and Silver) will (has) become God’s anchor to your financial survival tomorrow.

Yes, and it’s about to lost even more value, faster.

Exactly! Continuing the economic fiction and manipulation.

Thanks, Richard. Appreciate you.

Silver, gold, toilet paper. Be prepped and ready. Seriously thinking of cashing out, and buying more hard assets and will be in a position of safety to barter. Luck to all.

Thanks for your reply, John. Much appreciated.