Written by Bryan Lutz, Editor at Dollarcollapse.com:

The People’s Bank of China added to its gold reserves in March 2026, the 17th consecutive month of reported purchases, bringing total holdings to 74.38 million fine troy ounces. The financial press covered this the way it covers most central bank data releases, briefly, dutifully, and without much apparent curiosity about what it actually means.

Let me tell you what it actually means.

Seventeen consecutive months of gold accumulation, maintained through the Iran war, through gold’s surge past $5,500 and its subsequent correction, through the Hormuz closure and the ceasefire and the uncertainty about whether that ceasefire will hold, is a strategic policy. The People’s Bank of China is not buying gold because is buying gold because it has decided that gold is the right asset to hold regardless of price. That distinction is more important than any individual monthly data point, and it is the story that most analysts are missing entirely.

Where Have We Seen This Before?

To understand where this ends, it helps to remember where a nearly identical story ended the last time it played out.

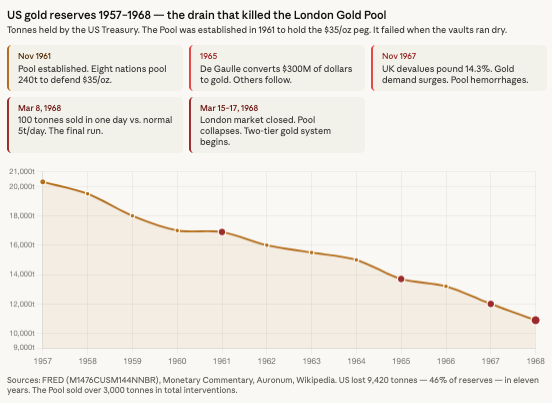

In November 1961, the United States and seven European allies formed what became known as the London Gold Pool. The arrangement was straightforward and, for a while, effective. The eight central banks would coordinate gold sales in the London market to prevent the price from rising above $35.20 per ounce, the level required to defend the Bretton Woods peg. The US provided 50 percent of the gold. The Europeans provided the rest. The Bank of England administered the daily operations. For six years, it worked.

Then it did not.

The mechanism of the collapse is worth understanding precisely, because it rhymes closely with what is happening today. The US had been running persistent deficits to finance both the Vietnam War and the Great Society programs at home, the classic guns-and-butter overreach that every overstretched empire eventually attempts. Dollars were piling up in foreign central bank vaults faster than the gold backing them could grow. France, under Charles de Gaulle, recognized the arrangement for what it was: a system that allowed the United States to acquire real goods and services from the rest of the world in exchange for paper promises it could manufacture without limit. De Gaulle began converting French dollar reserves into gold at the official rate. Other nations noticed and followed.

By early 1968, the Pool was bleeding metal at a rate that had become unsustainable. In a single week in March of that year, the consortium sold nearly 1,000 tonnes of gold into the market. On March 8 alone, 100 tonnes changed hands, compared to a typical daily sale of five tonnes. The London gold market was closed for two weeks on an emergency basis. When it reopened, the Pool was finished. The price controls were abandoned. Three years later, Nixon closed the gold window entirely, and the last formal link between the dollar and gold was gone.

The lesson the Pool’s architects never absorbed is the one that gold has been teaching governments for five thousand years: you can suppress the price of an asset that the world increasingly wants, but only for as long as you have the physical metal to sell into the market. When the metal runs out, the suppression ends, and the price moves to wherever it would have been without the intervention, usually in a hurry.

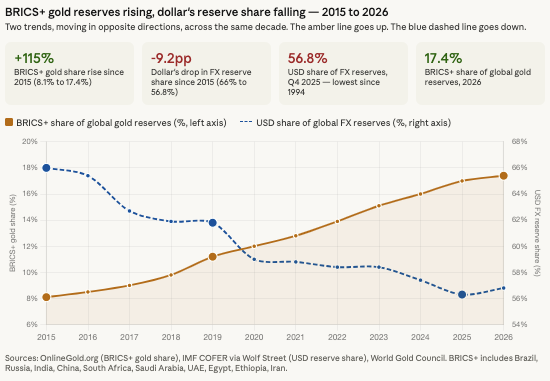

What China and its BRICS partners are doing today is the mirror image of what France did in 1965. They are converting dollar reserves into physical gold, deliberately, systematically, and at a scale that makes de Gaulle’s maneuver look modest by comparison. BRICS-aligned nations now hold 17.4 percent of global gold reserves, up from 11.2 percent in 2019. The People’s Bank of China’s current buying cycle began in November 2024. It has not missed a month since.

Why Central Bank Demand Is Different from Every Other Kind

When a hedge fund buys gold, it is making a bet. It has a thesis, a price target, a stop loss, and a redemption schedule to worry about. When the gold trade goes against it, even temporarily, the pressure to cut losses is real and immediate. This is why speculative gold demand is inherently volatile. Funds buy on the way up and sell on the way down, amplifying moves in both directions.

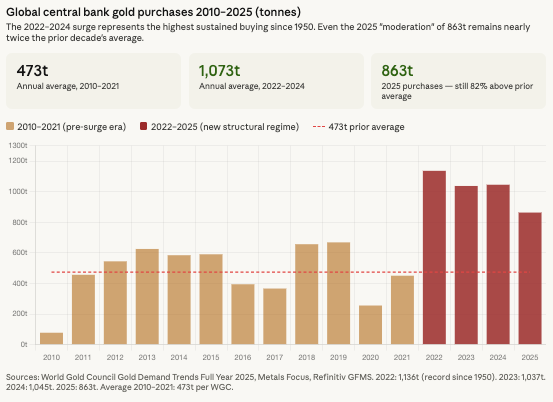

Central bank demand operates on an entirely different logic. As the World Gold Council noted in its most recent survey, 95 percent of central banks expect global official gold reserves to increase over the next twelve months, the highest level of optimism in the survey’s eight-year history. A record 43 percent of central banks indicated plans to increase their own holdings, up from 29 percent in 2024. Not one central bank anticipated a reduction.

These institutions are buying gold because they have made a long-term strategic decision to hold less of their reserves in dollar-denominated paper assets and more in an asset that carries no counterparty risk, cannot be sanctioned, cannot be printed, and has served as money for the entirety of recorded human history. When the price dips, they buy more. When the price rises, they buy slightly less. But they do not stop. The People’s Bank of China barely paused when gold was trading above $5,500. They kept buying.

This kind of demand creates something that speculative demand never does: a structural price floor. There is a level, currently estimated by most analysts at around $4,500 to $4,600 per ounce, below which sovereign buyers become aggressively active. That floor rises as the buying continues and as more central banks join the accumulation trend. It is not a guarantee against short-term volatility. It is a guarantee against the kind of prolonged bear market that gold endured between 1980 and 2000, when the strategic case for gold accumulation was not yet widely understood in the developing world.

The Paper Problem Nobody Is Talking About

There is a dimension to the China buying story that the mainstream financial press almost never mentions, which is the relationship between the physical gold that China is accumulating and the paper gold that Western financial markets have built on top of a shrinking physical base.

At the Comex futures exchange, paper claims on gold have historically run at roughly 60 ounces for every ounce of physical inventory available for delivery. This is a fractional reserve system for gold, in which the promises to deliver vastly outnumber the metal that could actually be delivered if a significant portion of those promises were called in at once.

China is not calling them in. Not yet. It is simply buying physical metal, month after month, and moving it to Shanghai. Every tonne that moves from Western vaults to Eastern ones is a tonne that is no longer available to satisfy paper claims. Every month that the buying continues, the gap between outstanding paper promises and available physical metal grows a little wider. At some point, that gap becomes the story. When it does, the resolution will not be orderly.

This is exactly what happened at the tail end of the London Gold Pool. The pool’s architects were not dishonest men. They genuinely believed they could manage the gap between the official price and the market’s preferred price through coordinated intervention. What they could not manage was the physical reality of a vault that was being steadily drained by buyers who preferred metal to promises. The math eventually won, as the math always does.

Now Consider What Happens When Pension Funds Notice

China’s central bank holds approximately 2,306 tonnes of gold as of the latest reported figures. That sounds like a lot, but in the context of the global gold market, it isn’t.

The world’s pension funds manage approximately $30 trillion in assets. Their allocation to gold is roughly one-third of one percent. If they were to increase that allocation to just one percent, still an almost absurdly modest position by any historical standard, the resulting new demand would be approximately $200 billion worth of gold. At current prices, that represents demand roughly equal to an entire year of global mine production, from institutions that currently own almost none.

If pension funds moved to a five percent allocation, which would still be conservative by pre-1971 standards, the resulting demand would be approximately $1.4 trillion. One-point-four trillion dollars chasing a market in which total annual mine supply is worth less than $250 billion at current prices. Add the other institutional investors, mutual funds, hedge funds, insurance companies, and sovereign wealth funds, who collectively manage another $70 trillion and also own virtually no gold, and a one-percent swing in their allocation would send another $700 billion into this already supply-constrained market.

None of this is happening yet. Pension fund managers are cautious, consensus-driven, and acutely aware that their peers are not yet buying. But consensus shifts. The question is what shifts it.

China buying gold for 17 consecutive months while Iran disrupts the oil market and BRICS pilots a gold-backed digital settlement currency is the kind of accumulation of evidence that eventually moves institutional consensus. When the first major pension fund raises its gold allocation to one percent and publishes a paper explaining why, others will follow. That is how institutional money moves. It acts like a cascading, or domino effect.

What $74 Million Ounces Is Telling You

Strip away the geopolitics, the Hormuz crisis, the ceasefire optimism, and the daily noise of gold’s price volatility, and what you are left with is a simple, durable story.

The world’s second-largest economy has spent 17 months converting paper dollar reserves into physical gold. It is doing this openly, reporting the purchases monthly, making no effort to conceal the direction of policy. The Chinese government’s own state media explained the strategy with admirable clarity back in 2013, from the The Money Bubble:

“The US and Europe have always suppressed the rising price of gold. They intend to weaken gold’s function as an international reserve currency. They don’t want to see other countries turning to gold reserves instead of the US dollar or Euro. China’s increased gold reserves will thus act as a model and lead other countries towards reserving more gold. Large gold reserves are also beneficial in promoting the internationalization of the yuan.”

That was twelve years ago. China has been executing that strategy ever since. The current 17-month buying streak is not a new development. It is the continuation of a policy that was articulated publicly, implemented consistently, and is now, finally, being validated by the price of gold above $4,700 per ounce.

The London Gold Pool collapsed because France decided that physical gold was preferable to American paper promises, and because the math of an overextended monetary system eventually proved the French right. The People’s Bank of China has reached the same conclusion, at ten times the scale, with 140 other countries watching and drawing their own conclusions.

Seventeen months is a verdict on the dollar system, one month at a time, in the oldest and most honest currency the world has ever known.

—-

References

Primary data and current news sources

CoinCentral. “Gold Prices Fall as Trump Sets Iran Deadline Over Strait of Hormuz.” April 2026. https://coincentral.com/gold-prices-fall-as-trump-sets-iran-deadline-over-strait-of-hormuz/

Bloomberg. “China’s PBOC Extends Gold-Buying Streak as Metal’s Rally Cools.” December 7, 2025. https://www.bloomberg.com/news/articles/2025-12-07/china-s-pboc-extends-gold-buying-streak-as-metal-s-rally-cools

Bloomberg. “China’s PBOC Adds Gold for 14th Month As Prices Hit Record.” January 7, 2026. https://www.bloomberg.com/news/articles/2026-01-07/china-s-pboc-adds-gold-for-14th-month-as-prices-hit-record

Central Banking. “China Goes Long Gold, Short Treasuries.” February 9, 2026. https://www.centralbanking.com/central-banks/reserves/gold/7974984/china-goes-long-gold-short-treasuries

WorldGoldPricePro. “People’s Bank of China Boosts Gold Reserves for Seventeenth Month Despite Market Volatility.” April 2026. https://www.worldgoldpricepro.com/archives/19707

Mining.com. “China’s Central Bank Buys Gold for 14th Consecutive Month.” January 7, 2026. https://www.mining.com/web/chinas-central-bank-buys-gold-for-14th-consecutive-month/

World Gold Council

World Gold Council. “Gold Demand Trends: Full Year 2025 — Central Banks.” January 29, 2026. https://www.gold.org/goldhub/research/gold-demand-trends/gold-demand-trends-full-year-2025/central-banks

World Gold Council. “China Gold Market Update: November Demand Feels the VAT Reform.” December 2025. https://www.gold.org/goldhub/gold-focus/2025/12/china-gold-market-update-november-demand-feels-vat-reform

World Gold Council. “China Gold Market Update: Wholesale Demand Rebounded.” October 2025. https://www.gold.org/goldhub/gold-focus/2025/10/china-gold-market-update-wholesale-demand-rebounded

World Gold Council. “China Gold Market Update: Seasonal Strength in December.” January 15, 2025. https://www.gold.org/goldhub/gold-focus/2025/01/chinas-gold-market-update-seasonal-strength-december

World Gold Council. “Central Bank Gold Statistics: Central Banks Ramp Up Gold Buying in October.” December 2, 2025. https://www.gold.org/goldhub/gold-focus/2025/12/central-bank-gold-statistics-central-banks-ramp-gold-buying-october

Central bank reserve data and de-dollarization

Wolf Street. “Status of US Dollar as Global Reserve Currency: USD Share Drops to 31-Year Low as Central Banks Diversify into Other Currencies and Gold.” March 28, 2026. https://wolfstreet.com/2026/03/28/status-of-us-dollar-as-global-reserve-currency-usd-share-drops-to-31-year-low-as-central-banks-diversify-into-other-currencies-gold/

Wolf Street. “Status of the US Dollar as Global Reserve Currency: Share Drops to Lowest Since 1994.” December 26, 2025. https://wolfstreet.com/2025/12/26/status-of-the-us-dollar-as-global-reserve-currency-usd-share-drops-to-lowest-since-1994/

IMF. “Currency Composition of Official Foreign Exchange Reserves (COFER) — Q2 2025.” October 2, 2025. https://data.imf.org/en/news/october%201%202025%20cofer

BestBrokers. “Global Reserve Currency Landscape 2025: US Dollar Shifts from Dominant Force to Record-Low Share.” November 14, 2025. https://www.bestbrokers.com/forex-brokers/global-reserve-currency-landscape-2025-u-s-dollar-shifts-from-dominant-force-to-record-low-share/

OnlineGold.org. “Central Banks Added 1,200 Tonnes in 2025 — What It Means for Gold in 2026.” February 17, 2026. https://onlinegold.org/analysis/central-bank-gold-reserves-2026/

Federal Reserve Board. “The International Role of the US Dollar — 2025 Edition.” July 18, 2025. https://www.federalreserve.gov/econres/notes/feds-notes/the-international-role-of-the-u-s-dollar-2025-edition-20250718.html

London Gold Pool history

Wikipedia. “London Gold Pool.” Accessed April 2026. https://en.wikipedia.org/wiki/London_Gold_Pool

Monetary Commentary (Substack). “London Gold Pool’s Collapse: The 1968 Crisis That Shook Bretton Woods.” August 10, 2025. https://monetarycommentary.substack.com/p/london-gold-pools-collapse-the-1968

Auronum. “The London Gold Pool: A Forgotten War Between Central Banks and the Market.” Accessed April 2026. https://auronum.co.uk/the-london-gold-pool-a-forgotten-war-between-central-banks-and-the-market/

APMEX. “The London Gold Pool Collapse in 1968.” August 12, 2025. https://learn.apmex.com/learning-guide/history/london-gold-pool/

Numismatic News. “The Failure of the 1960s London Gold Pool.” August 16, 2019. https://www.numismaticnews.net/coin-market/the-failure-of-the-1960s-london-gold-pool

Bordo, Michael D., Monnet, Eric, and Naef, Alain. “The Gold Pool (1961–1968) and the Fall of the Bretton Woods System: Lessons for Central Bank Cooperation.” NBER Working Paper No. 24016, 2017. https://www.nber.org/system/files/working_papers/w24016/w24016.pdf

Federal Reserve Bank of St. Louis (FRED). US Gold Reserves historical series M1476CUSM144NNBR. https://fred.stlouisfed.org/

Pension funds, paper gold, and institutional demand

Turk, James, and Rubino, John. The Money Bubble. DollarCollapse.com / GoldMoney, 2013. Specifically: Chapter 21 (Why Gold Is About to Soar), Chapter 22 (The Case for $10,000+ Gold), Chapter 23 (The Case for $100+ Silver), and Chapter 24 (Bullion: Money, Not an Investment).

Visual Capitalist / BullionVault. “Charted: A Decade of Central Bank Gold Purchases.” October 30, 2025. https://www.visualcapitalist.com/sp/charted-a-decade-of-central-bank-gold-purchases/

Discovery Alert. “Central Bank Gold Buying Reaches Unprecedented Levels in 2025.” November 5, 2025. https://discoveryalert.com.au/gold-accumulation-2025-central-bank-strategies/