US Dollar Collapse: What You Need to Know

Lastest update: April 16, 2026

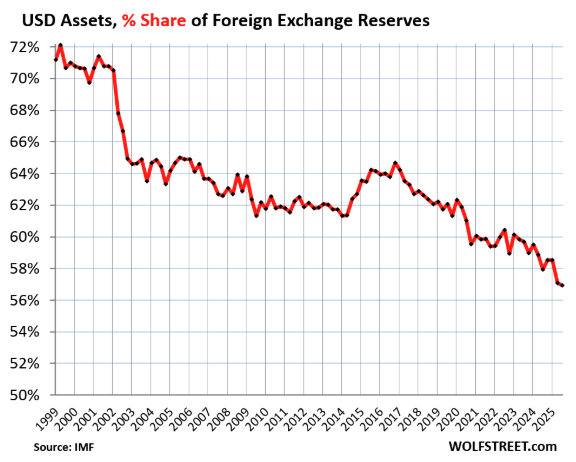

The US dollar’s share of global foreign exchange reserves just dropped to 56.8%, a 31-year low. The national debt crossed $39 trillion during the Iran war. Interest payments on that debt are now the fastest-growing line item in the federal budget. Morgan Stanley estimates the dollar could lose another 10% by the end of 2026. And 68% of the world’s central banks are buying gold like their monetary future depends on it.

The dollar is not dying in a single dramatic event. It is dying the way Hemingway described going bankrupt:

Gradually, then suddenly.

We are deep into the “gradually” phase. The “suddenly” part is what this page is about.

At DollarCollapse.com, we have tracked this trajectory since 2004. The thesis has not changed in twenty years: fiat currencies are a failed experiment, governments cannot stop printing, and real assets are the lifeboats. What has changed is the speed. The data points that used to arrive quarterly now arrive weekly.

This page covers what a dollar collapse actually means, how far along we are, what triggers could accelerate it, and what you can do to protect your purchasing power before the rest of the world figures out what is happening.

What Does a US Dollar Collapse Actually Mean?

A dollar collapse does not mean the currency disappears overnight. No reserve currency in history has vanished in a flash. The British pound’s transition from the world’s dominant currency to a secondary player took roughly 30 years, from the 1920s to the 1950s. So, the process looks more like erosion than an explosion.

In practical terms, a dollar collapse means a sustained, significant decline in the dollar’s purchasing power and its role in global trade. It means the things you buy get more expensive, not because those things are worth more, but because the currency you use to buy them is worth less. It means your savings lose value while you sleep. It means the US government’s ability to borrow cheaply from the rest of the world slowly evaporates.

The mainstream financial press frames this as a debate between “collapse” and “no collapse,” as though those are the only two options. They are not. We are not pretending that the dollar will instantly go to zero and your savings will get vaporized… It’s more like this. You’ll feel it more like this. The loss of value. Maybe it will be fast enough, to devastate the purchasing power of people who hold their savings in dollar-denominated assets. Maybe not.

The answer to that question, based on every data point available, is yes.

How Far Along Is the Dollar’s Decline?

The numbers tell the story more clearly than any commentary.

The dollar’s share of global foreign exchange reserves has fallen from 71% in 1999 to 56.8% as of the latest IMF data. That is a decline of nearly 15 percentage points in a quarter century. Central banks are not dumping dollars dramatically. They are buying everything else faster: euros, yen, renminbi, and above all, gold.

The IMF’s COFER data shows that what they call “non-traditional reserve currencies,” a basket of dozens of smaller currencies, have more than doubled their share since 2021, now standing at 6.1%. The world’s central banks are quietly building exits while the building is still standing.

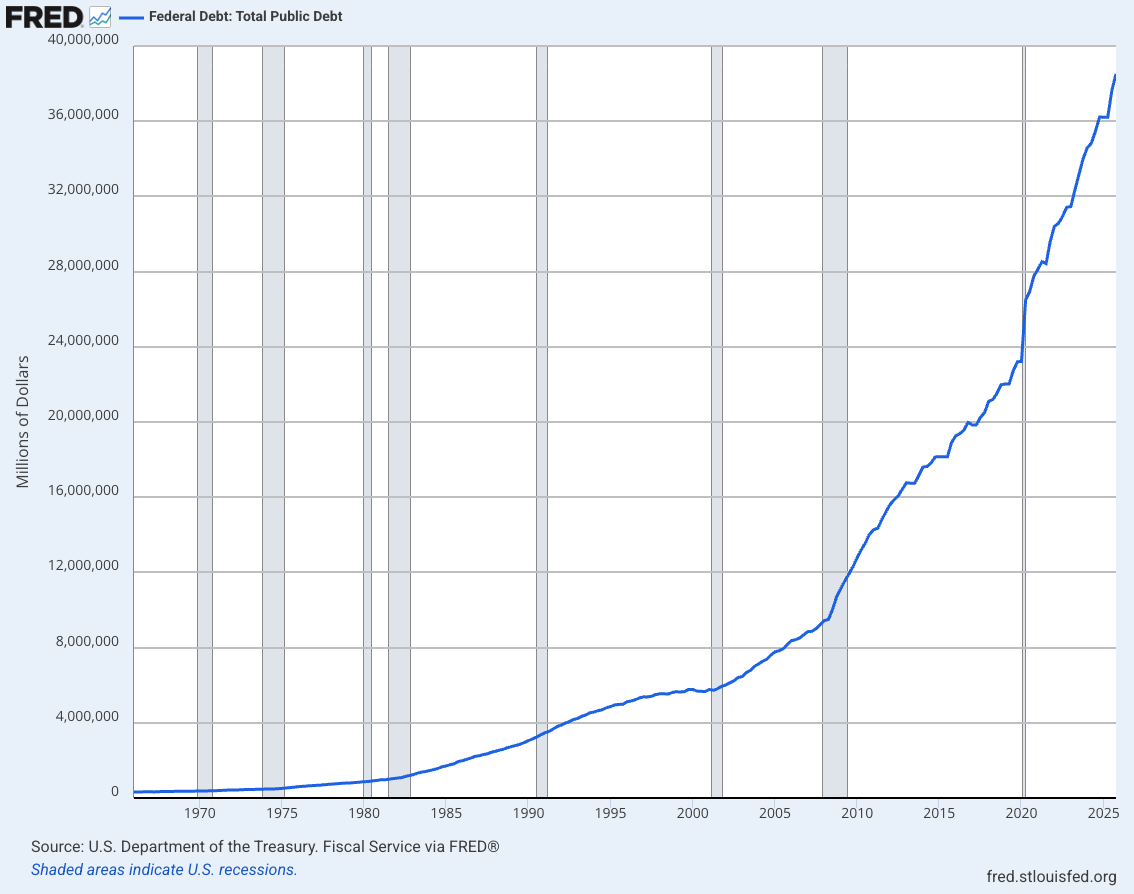

Meanwhile, the US national debt has crossed $39 trillion. A few numbers to make that visceral: a million seconds is about 12 days. A billion seconds is 32 years. A trillion seconds is roughly 32,000 years. The US government owes 39 trillion of those seconds. And the debt is growing by roughly $1 trillion every six months.

Interest payments on that debt have become the federal government’s fastest-growing expense. At current rates, debt service consumes more of the budget than defense spending. And here is the trap: if rates stay elevated, interest costs keep compounding. If rates fall, the dollar weakens and inflation returns. If the government cuts spending to slow the debt, the economy contracts and tax revenue falls, making the deficit worse. All roads lead to the same destination.

Morgan Stanley estimates the dollar could lose another 10% by the end of 2026, following an 11% decline in the dollar index during the first half of 2025, the biggest half-year drop since 1973. The Atlantic Council’s Dollar Dominance Monitor confirms the direction of travel, even if it disputes the speed.

Here is what the mainstream analysis misses:

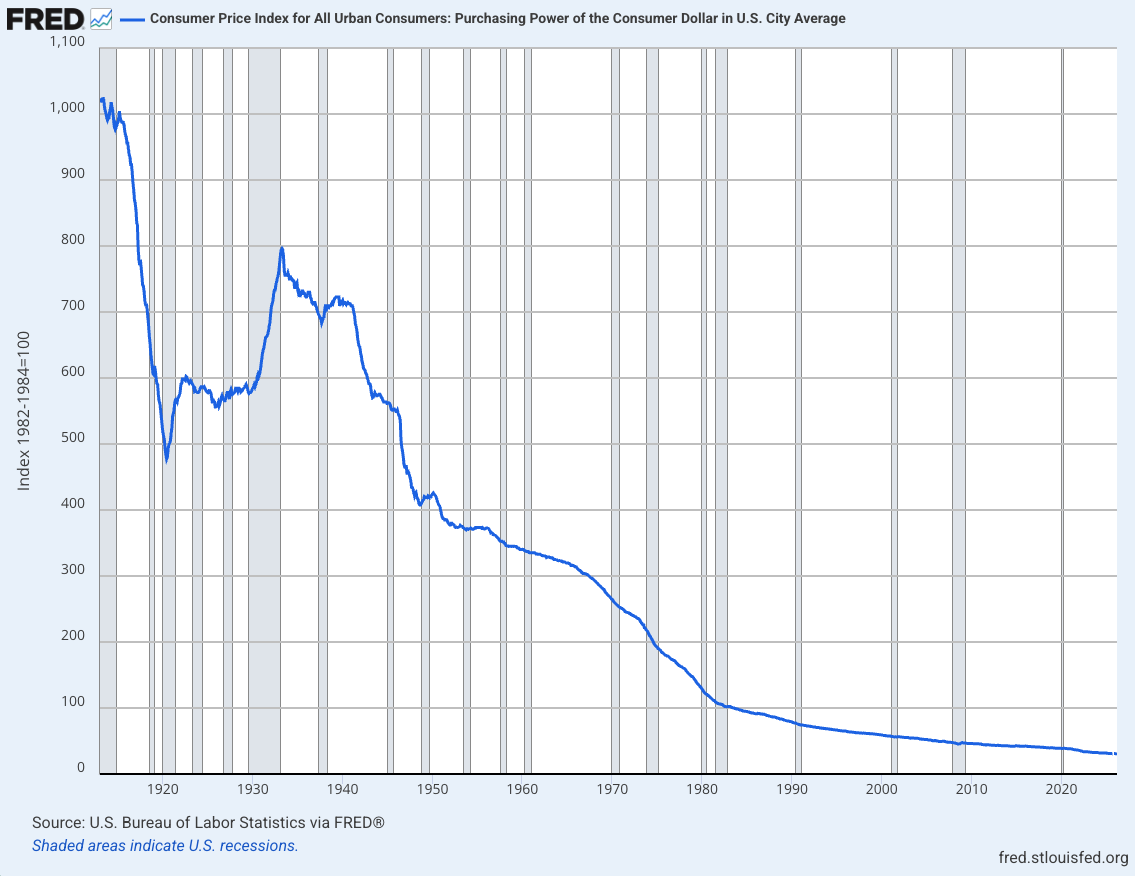

The dollar does not need to lose its reserve status to destroy your purchasing power. It just needs to keep doing what it has been doing. Since 1971, when Nixon severed the last link between the dollar and gold, the currency has lost over 85% of its purchasing power. A dollar from 1971 buys about 14 cents worth of goods today. That is not a prediction. That is a fact, measured by the government’s own inflation data. The question is whether the next 85% takes another fifty years or happens much faster.

The structural answer points to faster. The debt-to-GDP ratio is higher than at any point since World War II, but unlike the 1940s, the debt was not incurred building productive capacity. It was incurred funding transfer payments, financial bailouts, and military operations. There is no postwar industrial boom waiting on the other side to grow the economy out of the hole. There is just more debt.

The BIS 2025 Triennial Survey found the dollar on one side of 89.2% of all foreign exchange transactions, which dollar optimists cite as proof of continued dominance. What they fail to mention is that FX trading volume reflects current plumbing, not future direction. Reserve allocations reflect where central banks think the world is heading. And reserve allocations are heading away from the dollar at the fastest pace in three decades.

What Would Trigger an Acceleration?

A slow decline can become a fast one. Here are the catalysts that could compress decades of erosion into years.

A loss of confidence in US fiscal management.

The Congressional Budget Office projects large deficits and a rising debt path through the next decade. Markets have tolerated this because Treasury bonds remain the deepest and most liquid sovereign debt market on earth. But tolerance is not the same as confidence. If a debt ceiling crisis, a credit downgrade, or a political miscalculation causes foreign buyers to demand significantly higher yields, the debt spiral accelerates.

De-dollarization reaching a tipping point.

Russia and China now settle approximately 90% of their bilateral trade in rubles and yuan. China settles roughly half of its foreign trade in yuan, up from 20% in 2022. The BRICS bloc has launched a pilot “Unit” backed by 40% gold and 60% member currencies. The CIPS payment system has 1,467 indirect participants across 119 countries. None of these individually replace the dollar. Together, they build the infrastructure for a world that does not need it as much.

An energy market shock.

The petrodollar system, established in 1973, required oil-purchasing nations to accumulate dollars for energy transactions. The Iran war and the Strait of Hormuz crisis have demonstrated that alternative energy settlement arrangements are operationally viable under pressure. If oil is routinely priced and settled in non-dollar currencies, one of the foundational pillars of dollar demand disappears.

A Federal Reserve policy error.

The Fed faces an impossible trilemma: it cannot simultaneously fight inflation (high rates), support the economy (low rates), and keep the government’s borrowing costs manageable. Any choice it makes damages the other two objectives. The market is watching the Fed the way a patient watches a surgeon who keeps glancing at the clock.

What Happens to You If the Dollar Collapses

This is the part that matters to ordinary people, not the macroeconomic abstractions.

If the dollar loses significant value, the price of everything imported rises. The US imports roughly $3.2 trillion in goods annually. Everything from electronics to food to energy gets more expensive. This is not theoretical. Americans watched it happen in real time during the 2025 tariff shock and again when the Iran war spiked oil prices.

Your savings lose purchasing power. A dollar in a savings account earning 4% while real inflation runs at 7% is losing value every month. Your bank balance stays the same. What it buys does not.

Fixed-income investments suffer. Bonds pay fixed amounts of dollars. If those dollars buy less, your real return is negative. Retirees living on bond income and Social Security are the most vulnerable population in a dollar decline scenario, and they are the ones least equipped to adapt.

Debt becomes a double-edged sword. If you hold fixed-rate debt (like a 30-year mortgage), a weaker dollar actually helps you: you repay the loan in cheaper dollars. Variable-rate debt, on the other hand, becomes more expensive as the Fed raises rates to defend the currency.

Asset prices get distorted. Stocks can rise in nominal terms during a currency decline, not because companies are more valuable, but because the measuring stick is shrinking. Real estate tends to hold value because it is a tangible asset priced in local currency. Gold and silver historically outperform during periods of currency weakness, which is precisely why central banks are accumulating them at record pace.

The 1970s parallel is instructive. The last time the dollar experienced a major confidence crisis, from 1971 (Nixon closing the gold window) through 1980, consumer prices roughly tripled. Gasoline went from 36 cents to $1.19. A median home went from $24,000 to $62,000. Gold went from $35 to $850. Silver went from $1.50 to nearly $50. The people who saw it coming and positioned in real assets preserved and grew their wealth. The people who stayed in cash and bonds watched their purchasing power evaporate.

The circumstances today are not identical, but the pattern is recognizable. An overstretched government running structural deficits. A central bank trapped between fighting inflation and funding the government. Rising geopolitical tensions disrupting energy markets. A currency that the rest of the world is slowly, methodically, replacing.

We have seen this movie before. The ending does not change because the actors are different.

How to Protect Your Wealth

The playbook is straightforward, even if executing it requires discipline.

Own real assets. Gold, silver, and real estate have survived every currency crisis in recorded history. They cannot be printed, debased, or inflated away. Central banks are telling you exactly what they think of the dollar by buying 850 tonnes of gold in 2026 alone. Follow the smart money.

Diversify out of dollar-only holdings. International stocks, foreign-currency bonds, and commodity exposure all reduce your dependence on a single currency. This is not disloyalty. It is basic risk management. Even Charles Schwab, hardly a fringe outfit, now recommends investors consider non-USD international bonds given the dollar outlook.

Reduce variable-rate debt. If rates spike during a currency defense, variable-rate borrowers get crushed. Lock in fixed rates while they are available. Conversely, do not rush to pay off a low fixed-rate mortgage. In a dollar decline, that 3% mortgage becomes the best trade you ever made.

Hold physical cash and hard assets outside the banking system. Not all of it. But enough to weather a disruption. When the system seized up in 2008, access to bank accounts and credit lines was not guaranteed. A portion of your wealth should be outside the reach of any institution that can freeze it, restrict it, or bail it in.

Stay informed. The mainstream financial press will tell you the dollar is fine right up until it is not. That is not a conspiracy. It is an incentive problem: their advertisers, their sources, and their worldview all depend on the current system continuing. At DollarCollapse, our incentive is different. We have been tracking this since 2004, and we will keep tracking it until the last fiat domino falls.

The Bottom Line

The US dollar is not going to zero. It does not need to. A 30-50% decline in real purchasing power, which has already begun, is enough to devastate the savings of a generation of Americans who were told to keep their money in dollar-denominated assets.

Take a look at the data. The dollar’s reserve share is declining. The debt is compounding. The alternatives are being built. The central banks of the world are telling you with their actions (gold, gold, more gold) what they will not tell you with their words.

The mainstream view is that de-dollarization is “gradual” and “manageable.” That was also the mainstream view of subprime mortgages in 2006. Gradual processes have a way of becoming unmanageable on a Tuesday afternoon when nobody is expecting it.

Make sure to reposition before the crowd figures it out. By then, the lifeboats will be full.