De-Dollarization Explained: Why the World Is Ditching the Dollar

Latest update: April 16, 2026

For decades, the US dollar has been the operating system of global finance. Oil priced in dollars. Commodities traded in dollars. Central bank reserves stacked in dollars. If you wanted to do business anywhere on earth, you needed greenbacks. That was the deal.

Now the deal is changing.

De-dollarization is the process by which countries, central banks, and institutions reduce their reliance on the US dollar for trade, reserves, and financial transactions. It is not a conspiracy theory. Neither is it a BRICS press release. It is an observable, measurable, accelerating shift in how the world organizes its money, and it has profound implications for anyone whose savings, income, or retirement is denominated in dollars.

This page explains what de-dollarization is, why it is happening now, how far it has progressed, and what it means for ordinary investors.

What Is De-Dollarization?

De-dollarization is a reduction in the structural demand for US dollars in global commerce and finance. That includes three layers.

The first layer is trade invoicing. When two countries trade with each other, they typically price the transaction in dollars, even if neither country is the United States. This convention means that vast quantities of dollars must be held globally just to facilitate commerce. When countries begin invoicing in their own currencies, or in a third-party currency like the yuan, they need fewer dollars.

The second layer is financial transactions. Most cross-border lending, bond issuance, and interbank payments flow through dollar-denominated channels, primarily the SWIFT messaging system. When alternative payment systems (like China’s CIPS or the BRICS Pay network) allow transactions without touching SWIFT, dollar intermediation declines.

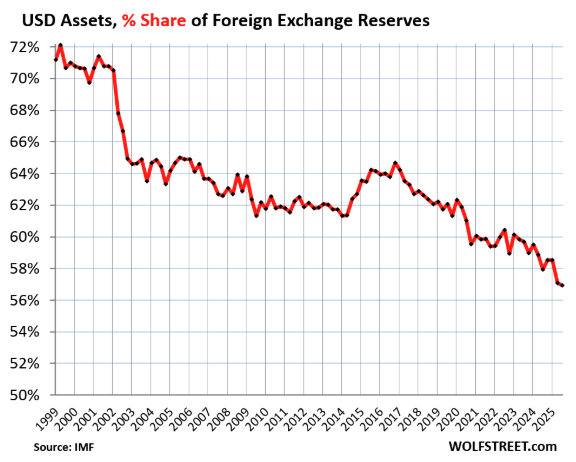

The third layer is central bank reserves. Governments hold foreign exchange reserves as a buffer against economic shocks. For decades, the dollar dominated those reserves at 70%+ of the total. As central banks diversify into other currencies, gold, and alternative assets, the dollar’s reserve share shrinks, reducing the world’s appetite for US Treasury bonds.

All three layers are eroding simultaneously. That is what makes this moment different from previous episodes of dollar skepticism.

The cumulative effect is a decline in what economists call “structural demand” for dollars. When the world needed dollars for everything, the US could run enormous trade deficits and fund them cheaply because foreign governments were essentially forced to accumulate dollar reserves. That compulsion is weakening. Not disappearing. Weakening. And in a system built on the assumption of infinite dollar demand, weakening is enough to change the math.

Why Is De-Dollarization Happening Now?

Three forces converged at once.

The weaponization of the dollar. In 2022, the US and its allies froze approximately $300 billion in Russian central bank reserves and cut Russian banks off from SWIFT. Whatever you think of the geopolitics, the financial message was unmistakable: if you cross Washington, your dollar reserves can be seized. Every central banker in Beijing, Riyadh, New Delhi, and Brazil took note. Holding dollars went from “safe” to “conditionally safe,” and the condition was political alignment with the United States. For countries that cannot guarantee permanent alignment, the rational response is to hold fewer dollars.

The rise of viable alternatives. Five years ago, there was no credible infrastructure for non-dollar trade at scale. That has changed. China’s CIPS now has 1,467 indirect participants across 119 countries, linking approximately 4,800 banks in 185 countries. Russia and China settle about 90% of their bilateral trade in rubles and yuan. China settles roughly half of all its foreign trade in yuan, up from 20% in 2022. The BRICS bloc has launched a pilot “Unit” currency backed by 40% gold and 60% member currencies. The mBridge platform enables central bank digital currency transactions between China, Hong Kong, Thailand, and the UAE. None of these systems individually match SWIFT’s scale. But they provide functional alternatives for countries that want them.

The US fiscal trajectory. The dollar’s share of global reserves has historically tracked the US share of global GDP and exports. Both are declining. The US national debt past $39 trillion, with structural deficits projected as far as the eye can see, makes foreign central banks uncomfortable about concentrating their reserves in a currency backed by an increasingly indebted government. As JP Morgan’s research notes, the main de-dollarization trend in reserves is the growing demand for gold, seen as an alternative to heavily indebted fiat currencies.

How Far Has De-Dollarization Progressed?

This is where the debate gets heated, because the answer depends on which data you look at.

Where the dollar is losing ground: Central bank reserves. The dollar’s share has dropped from 71% in 1999 to 56.8% in the latest data, the lowest since the early 1990s. The share of gold in emerging market reserves has doubled from 4% to 9% over the past decade. Central banks bought over 1,000 tonnes of gold in each of 2022, 2023, and 2024, with 850 tonnes projected for 2026. This is the clearest, most measurable de-dollarization signal.

Where the dollar is losing ground slowly: Trade invoicing and bilateral settlements. China’s yuan share of its own cross-border transactions has risen to roughly 50%. India has begun purchasing Russian oil in rupees and dirhams. Standard Bank, Africa’s largest, linked directly into CIPS in early 2026, enabling direct renminbi settlements without dollar intermediation. These are real shifts, but they remain concentrated in trade between BRICS members and their partners.

Where the dollar remains dominant: FX trading volumes. The BIS 2025 survey found the dollar on one side of 89.2% of all foreign exchange transactions, actually up from 88.4% in 2022. Cross-border debt issuance in dollars holds steady at roughly 70%. The US Treasury market remains the deepest and most liquid sovereign bond market in the world.

Comments: The people who say de-dollarization is a “myth” point to the FX trading data. The people who say it is imminent point to the reserve data. Both are reading different chapters of the same book. The reserves data tells you where central banks think the world is going. The FX trading data tells you where it is right now. In a transition, the destination matters more than the current location.

The historical analogy matters here. The British pound’s decline as the world’s reserve currency took three decades and was not obvious until it was over. At no point during the transition did the pound lose its role in a dramatic crash. It simply became less necessary, one trade agreement and one reserve reallocation at a time. That is exactly what the dollar data looks like today.

The BRICS Factor

BRICS (Brazil, Russia, India, China, South Africa, plus newer members Egypt, Ethiopia, Indonesia, Iran, and the UAE) represents roughly 45% of the world’s population and over 35% of global GDP. The bloc’s de-dollarization efforts deserve separate attention because they represent the most coordinated challenge to dollar hegemony since Bretton Woods.

The headline initiatives include BRICS Pay, a decentralized system linking national payment networks that has already reduced dollar usage in intra-bloc trade by roughly two-thirds. The New Development Bank is targeting 30% of all lending in local currencies by 2026. The pilot BRICS Unit, launched in late 2025, is backed by gold and member currencies and has established cross-border trade mechanisms that bypass dollar intermediation entirely.

But there are important caveats. BRICS is not a monolith. India’s External Affairs Minister explicitly stated that India has “no policy to replace the dollar” and views dollar reserve status as a source of global stability. Russia’s enthusiasm for de-dollarization is driven by sanctions necessity, not ideological commitment. Brazil and India maintain deep economic ties to Western financial institutions and are cautious about antagonizing Washington, especially after Trump threatened 100% tariffs on BRICS exports.

The most honest assessment is that BRICS is building optionality, not a revolution. Member nations want the ability to trade without dollars when it suits them. They do not necessarily want to abandon the dollar entirely. The difference matters, but the outcome for dollar demand is the same: lower.

The analogy is insurance. Nobody buys fire insurance because they want their house to burn down. They buy it because they recognize the risk. BRICS nations are buying insurance against a dollar-dependent world that has shown it will weaponize that dependence. The more insurance they buy, the less the dollar matters. And the less the dollar matters, the harder it becomes for the United States to fund its deficits at current rates.

This creates a feedback loop that the mainstream analysis consistently underestimates. Dollar weakness causes more de-dollarization, which causes more dollar weakness. Trump’s threat of 100% tariffs on BRICS exports is an attempt to break the loop through coercion. But as Brad Setser of the Council on Foreign Relations has observed, coercing countries to use the dollar through tariff threats could actually accelerate de-dollarization, a paradox Washington has not resolved.

What Does De-Dollarization Mean for Your Money?

If the world needs fewer dollars, the consequences flow directly to Americans who hold dollar-denominated assets.

Higher inflation. A core benefit of reserve currency status is that global demand for dollars keeps the currency stronger than it would otherwise be. As that demand declines, the dollar weakens, and imports get more expensive. The US imports roughly $3.2 trillion in goods per year. A weaker dollar means higher prices for everything from electronics to food.

Higher interest rates. If foreign central banks buy fewer Treasuries, the US government must offer higher yields to attract buyers. Higher government borrowing costs ripple through the entire economy: mortgages, car loans, business loans, credit cards. The era of cheap money relied on foreign governments subsidizing US borrowing. That subsidy is shrinking.

The “exorbitant privilege” unwinds. French finance minister Valery Giscard d’Estaing coined this phrase in the 1960s to describe America’s unique ability to borrow in its own currency at artificially low rates because the world had no choice but to hold dollars. As choices multiply, the privilege erodes. The US will not immediately lose the ability to borrow cheaply, but the cost will increase at the margins, and with $39 trillion in debt and 70% of Treasuries issued as short-duration securities requiring frequent refinancing, the margins are where the math breaks.

Gold and silver outperformance. When the monetary system’s anchor currency weakens, hard assets benefit. Gold has gained roughly 15.6% since January 1, 2026, while the Dow is up just 2.7% over the same period. Central banks are telling you what they think of the dollar’s future by buying gold at the fastest pace in recorded history. Silver adds industrial demand on top of monetary demand, making it arguably the more compelling play.

The need for diversification becomes urgent. International stocks, foreign-currency bonds, real estate, commodities, and precious metals all provide exposure outside the dollar system. This is not exotic advice. It is what every major central bank on earth is doing right now.

What De-Dollarization Is Not

Misconceptions about de-dollarization are almost as dangerous as ignoring it entirely. A few clarifications.

It is not the dollar going to zero. No serious analyst, including us, argues that the dollar will become worthless. The dollar will remain a major global currency for decades. The question is whether it will remain the dominant currency, with all the privileges that entails. The British pound is still a functional currency. It just does not run the world anymore. That transition cost the British public dearly in purchasing power, and it will cost Americans similarly.

It is not a BRICS conspiracy. The media loves to frame de-dollarization as a coordinated attack by America’s adversaries. In reality, it is a rational response by dozens of countries to observable US fiscal and foreign policy choices. When the US weaponized the SWIFT system against Russia, it did not just punish Moscow. It taught every other country that their dollar reserves could be frozen if they fell out of political favor. So you know the de-dollarization impulse is not ideological. It is self-preservation.

It is not happening overnight. The pound’s transition took 30 years. The dollar’s transition, if it follows the same arc, could take just as long. But the early stages of a transition are precisely when the opportunities are greatest and the risks of inaction are highest. By the time the transition is obvious to everyone, the price of protection (gold, silver, real assets) will reflect the new reality. The time to act is while most people are still debating whether de-dollarization is real.

It is not reversible through threats. Trump’s warning of 100% tariffs on BRICS nations that attempt to bypass the dollar may slow specific initiatives. But it cannot reverse the underlying incentives. Every tariff threat reminds trading partners why they want alternatives in the first place. Coercion is a short-term tool, but the second and third order effects make the incentives to de-dollarize permanent.

The bottom line is that de-dollarization is a structural, multi-decade process with measurable progress on multiple fronts. It does not require a crisis or a dramatic event. It only requires continued self-interested behavior by the world’s central banks and trading partners. And self-interest, unlike policy, never takes a day off.

Conclusion

De-dollarization is not a prediction. It is a process that is already underway, measurable in IMF data, visible in central bank gold vaults, and audible in the diplomatic language of nations that represent nearly half the world’s population.

The mainstream framing is that this is “gradual” and therefore not urgent. But gradual is precisely how reserve currency transitions have always worked. The pound did not crash. It eroded. And by the time the British public understood what had happened, the adjustment had already been priced into their standard of living.

The infrastructure for a post-dollar world is being built right now, by serious governments, with real money. Whether it takes five years or twenty-five is unknowable. What we do know is the direction.

The world is hedging its dollar exposure. You should too.