No Summary of Economic Projections at this meeting, so the wording is the policy. The redline is the news.

By the Dollarcollapse.com Editorial Team:

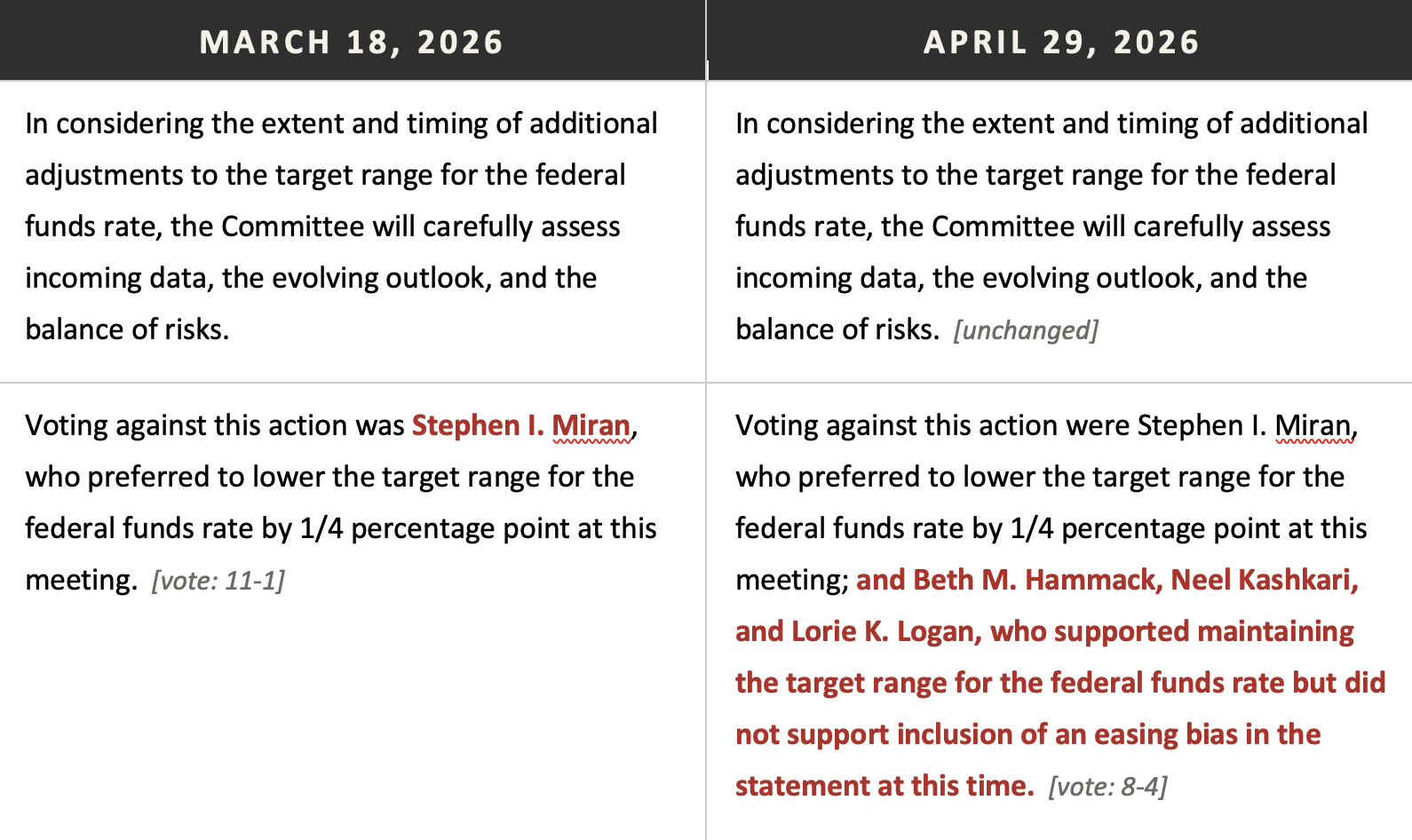

The FOMC voted 8 to 4 to maintain the federal funds target range at 3.50 to 3.75 percent at Jerome Powell’s final meeting as chair, the third consecutive hold since the September-to-December 2025 cutting cycle, with four dissents tying the most-fractured FOMC vote since October 1992. Governor Stephen Miran preferred a 25 basis point cut. Cleveland’s Beth Hammack, Minneapolis’s Neel Kashkari, and Dallas’s Lorie Logan supported the hold but voted against the inclusion of an easing bias in the statement language.

There is no Summary of Economic Projections at this meeting. The next SEP releases at the June 16 to 17 meeting, by which time Kevin Warsh is expected to chair. Without a dot plot, the statement diff is the policy signal, and the diff is doing real work.

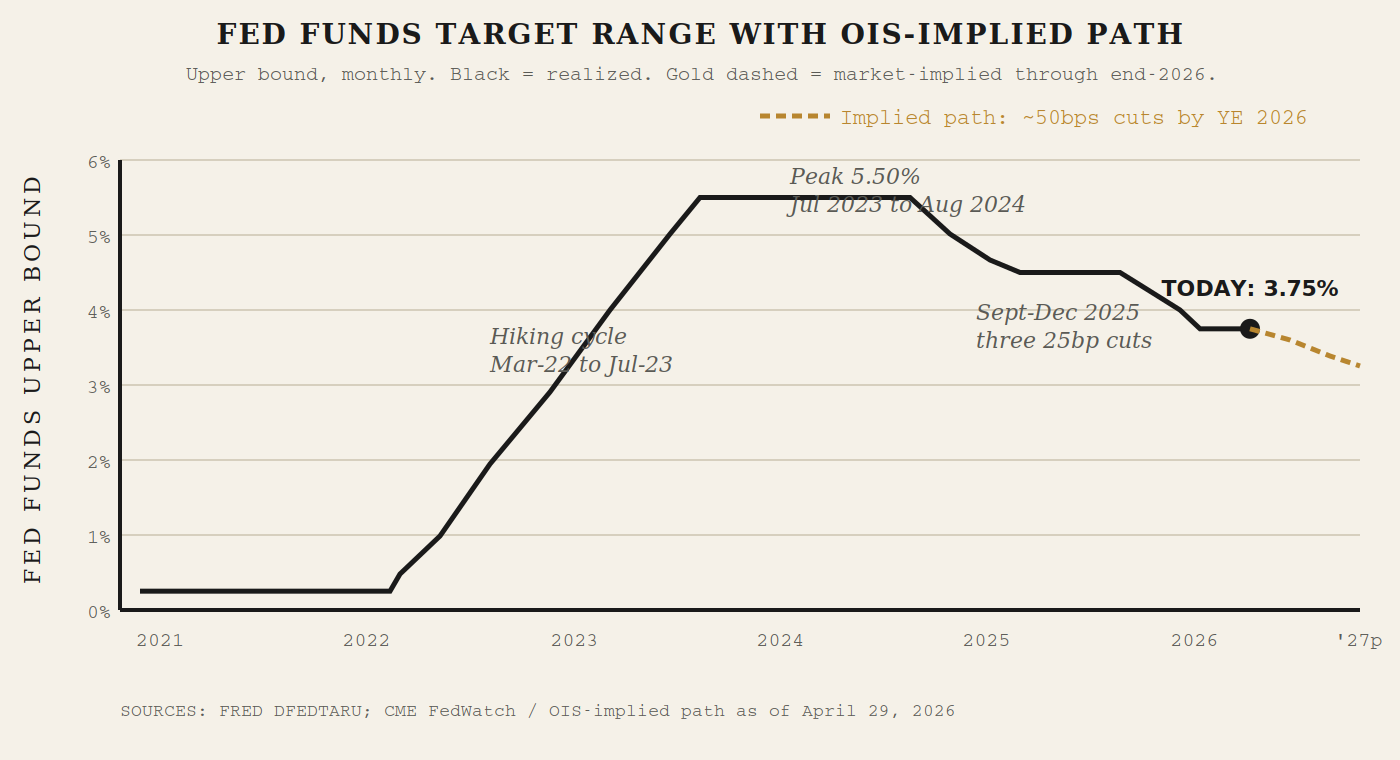

The fed funds upper bound remains at 3.75 percent (red line in chart 1) after the September, October, and December 2025 cuts. The OIS-implied path (gold dashed) prices roughly two more 25 basis point cuts by year-end 2026, putting the policy rate at 3.25 percent in 12 months. Tomorrow’s GDP advance estimate and PCE print will move that path more than today’s statement did.

The redline: March 18 vs April 29

Word-for-word comparison of the March 18 statement and today’s April 29 statement. Bold red marks language that changed. The substantive shifts are in the inflation characterization (added energy attribution and the high-uncertainty framing) and the labor description (now explicitly soft).

Three changes carry the signal. First, “available” became “recent,” a small but meaningful tightening that ties the assessment to current data rather than to a broader information set. Second, the inflation sentence shed “remains somewhat” and added explicit attribution to the global energy price increase, naming the supply shock the FOMC declined to name in March. Third, the labor description softened with “on average,” which is the kind of qualifier that previews further deterioration without committing to it. The Middle East language got tighter and more declarative.

The forward-guidance sentence is identical to March, which is precisely what produced the three regional-president dissent. Hammack, Kashkari, and Logan read the unchanged “additional adjustments” language as an embedded easing bias, given that the most recent moves have been cuts. They wanted it removed. The 8-to-4 split is the message Powell hands his successor.

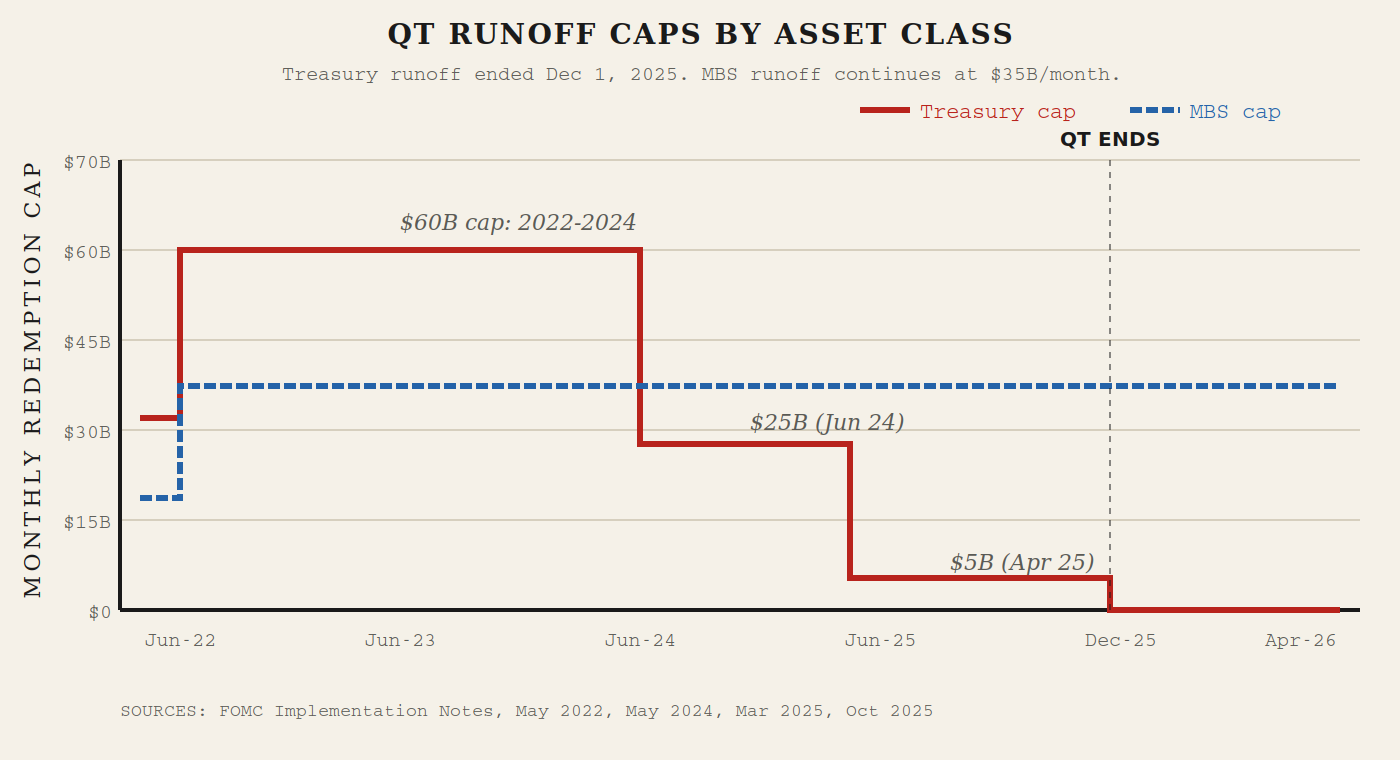

The quantitative tightening framework is the other piece of plumbing under review. Treasury runoff (red line in chart 2) ended on December 1, 2025. The MBS cap (blue dashed) remains at $35 billion per month and continues to drain. Today’s implementation note made no change to the MBS cap, which means the Fed is still passively shrinking its mortgage book even as it has stopped shrinking its Treasury book.

Treasury cap stepped down 60 to 25 to 5 to 0; MBS cap held at 35 throughout. Sources: FOMC Implementation Notes, May 2022 through October 2025.

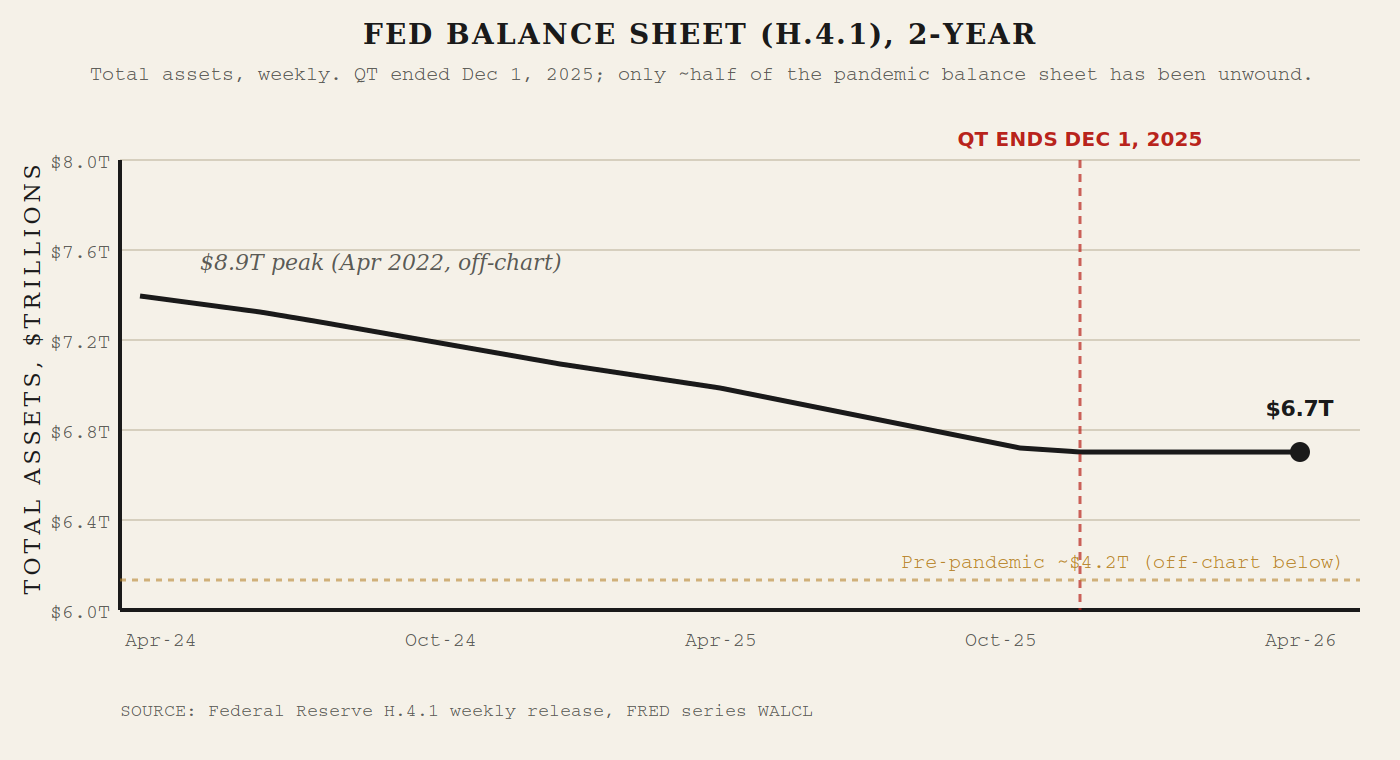

Total assets on the balance sheet sit at $6.7 trillion as of the April 22 H.4.1 release (black line in chart 3), down from the April 2022 peak of $8.9 trillion. That represents about a $2.2 trillion reduction over three and a half years. The pre-pandemic level (gold dashed reference, off the chart axis below) was approximately $4.2 trillion. Roughly half the pandemic balance sheet has been unwound. The other half is now permanent unless a future committee chooses otherwise.

Two-year window. Source: Federal Reserve H.4.1, FRED series WALCL.

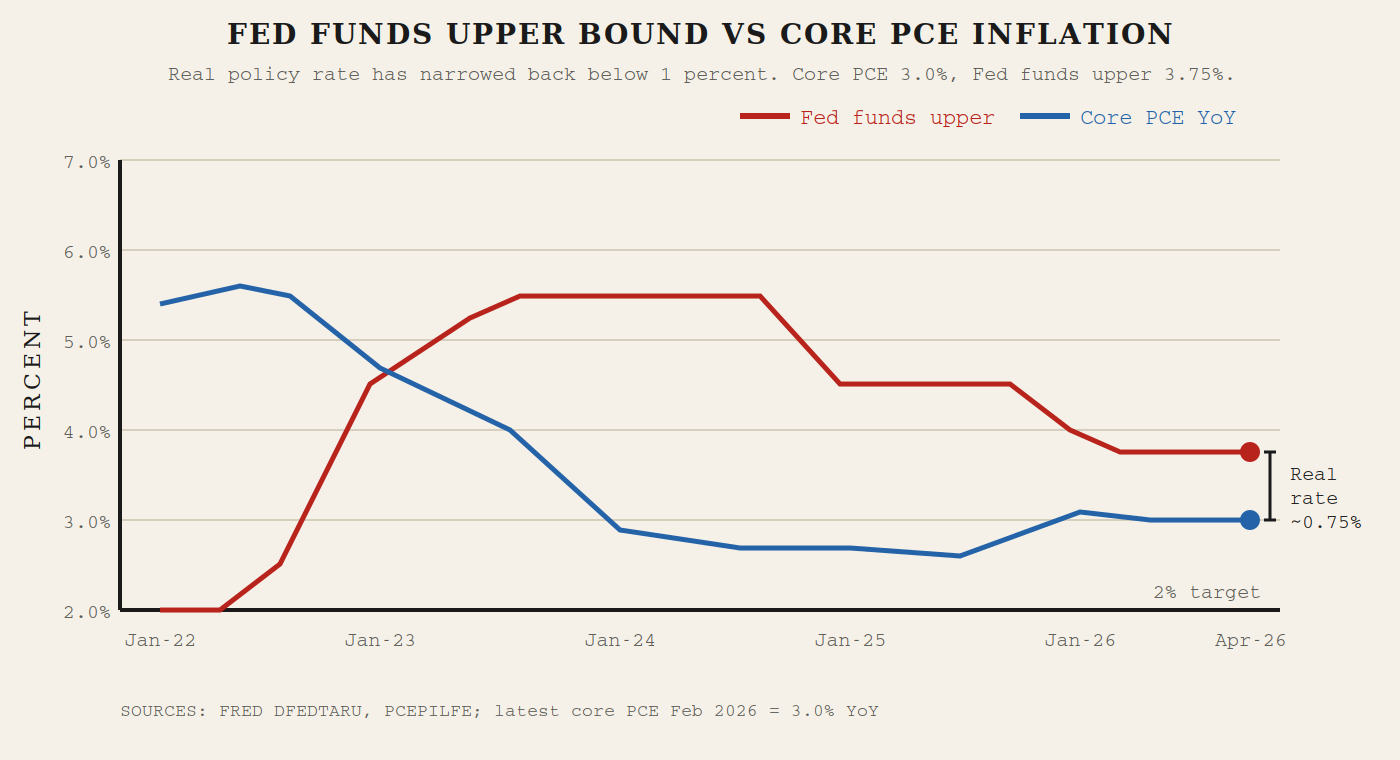

The real policy rate has narrowed meaningfully over the past nine months. The fed funds upper bound (red in chart 4) sits at 3.75 percent. Core PCE (blue) printed 3.0 percent year-over-year in February 2026, the most recent observation, with January at 3.1 percent. The implied real policy rate is approximately 0.75 percent, down from a peak of nearly 3.0 percent in mid-2024. By the metric the Fed itself uses to gauge restrictiveness, current policy is barely restrictive at all.

Real policy rate has compressed from ~3% peak in mid-2024 to ~0.75% today. Sources: FRED DFEDTARU, PCEPILFE.

This is the data Hammack, Kashkari, and Logan are reading. With inflation sticky at 3 percent and the policy rate already near neutral, they see no case for an easing bias. Miran reads the same data and concludes the Fed should cut anyway. Powell’s last act as chair is to preside over the disagreement without resolving it.

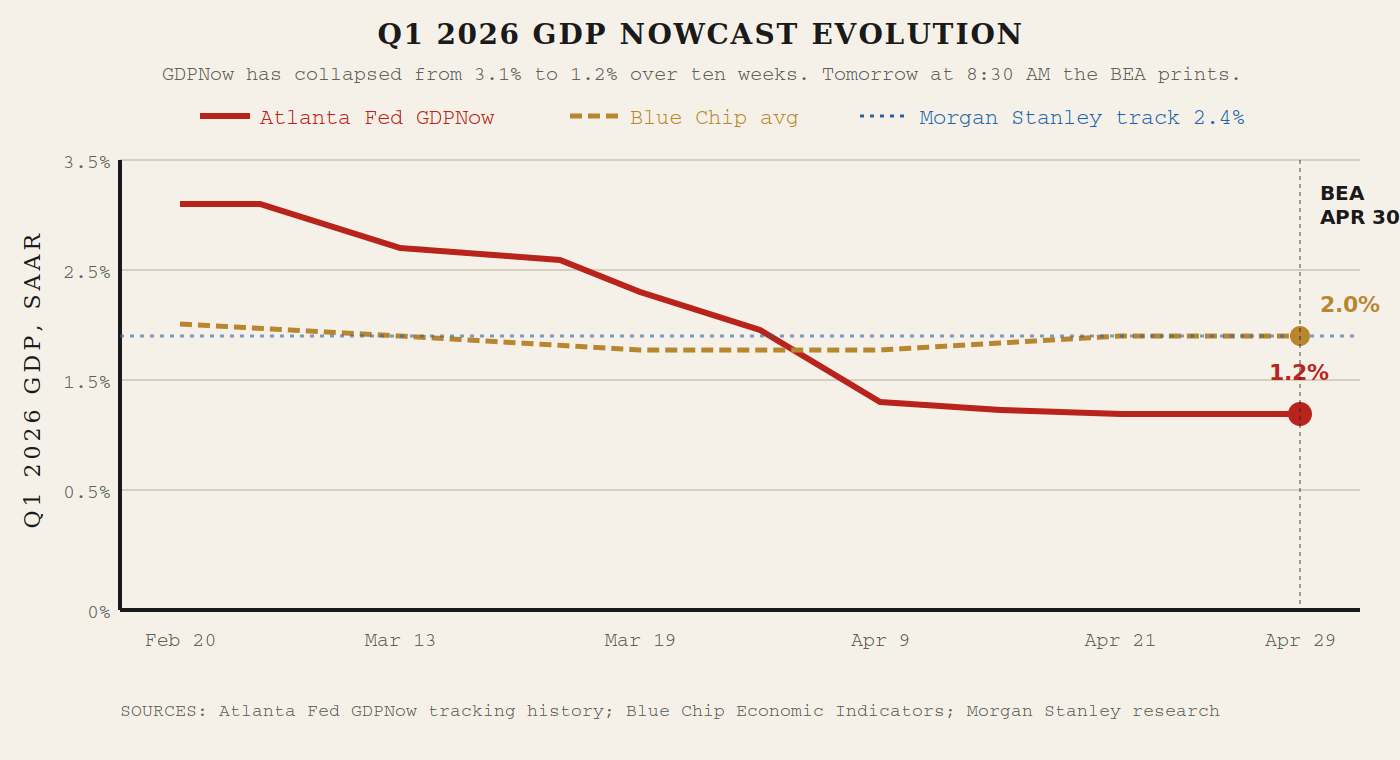

The growth picture going into tomorrow’s 8:30 AM advance estimate is the most contested input on Powell’s desk. The Atlanta Fed GDPNow (red in chart 5) collapsed from 3.1 percent in late February to 1.2 percent on April 29. Blue Chip consensus (gold dashed) drifted from 2.0 to 2.0 over the same window. Morgan Stanley’s in-house tracker (blue dotted) sits at 2.4 percent. The dispersion is the story: nowcasters disagree about Q1 GDP by more than a full percentage point on the day before the print. Whatever the BEA reports tomorrow will revise this picture for at least one of the three.

Q1 2026 GDP nowcast trajectory by source. BEA advance estimate prints April 30.

Sources: Atlanta Fed GDPNow, Blue Chip Economic Indicators, Morgan Stanley research.

A 1.2 percent print supports the easing-bias argument. A 2.4 percent print supports the no-easing-bias dissent. A 2.0 percent print leaves both camps where they were. The Fed voted today on a state of the world it will know more about in 18 hours.

The trimmed-mean PCE inflation rate published by the Dallas Fed printed 2.3 percent for the 12 months ending February, against the 3.0 percent core PCE reading. That 70 basis point gap is the gauge Warsh has publicly proposed substituting for core PCE. Today’s statement still uses the institution’s legacy framing. The next statement, in June, may not.

The frame

When there is no Summary of Economic Projections, the wording is the policy. Today’s redline says the Fed is pretending to be data-dependent while the data is telling it to do two opposite things at once. Inflation is sticky and the energy shock is now being named explicitly in the statement, which argues for holding rates. The labor market is softening at the margin and Q1 growth has decelerated by half on the Atlanta Fed model, which argues for cutting. Powell’s final committee resolved this by holding and inserting an easing bias that three of his regional presidents would not endorse. The 8 to 4 vote and the four dissents are not noise. They are the signal Warsh inherits in mid-May.