“Moore + Metcalfe = Creative Destruction squared.”

~ Bill Bonner and Addison Wiggin, Empire of Debt

Written by Bryan Lutz, Editor at Dollarcollapse.com:

The AI Bubble seems to only be growing. Two of the biggest sectors being semi-conductor/chip manufacturers, and data centers.

Let’s take a look at what’s going on with data centers so far. By the end, you’ll see what the “K-Shaped” construction of AI data centers looks like.

In the United States, the fourteen largest data center operators are on track to spend close to $750 billion this year, against a little under $450 billion last year, per Bloomberg. So, there’s still a lot of money being poured into data centers at a breakneck pace.

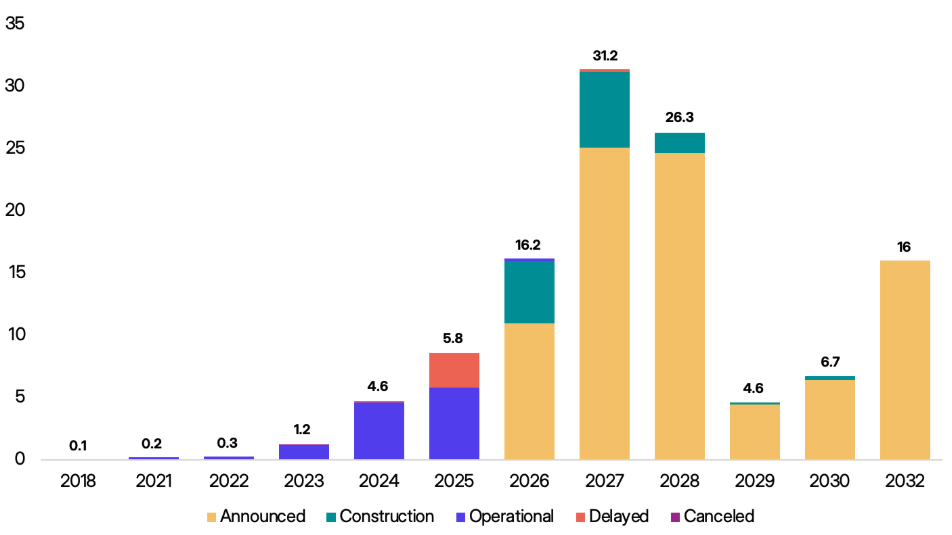

Yet, of the 16 gigawatts of capacity operators announced for delivery in 2026, only about 5 gigawatt sits under active construction. The other 11 have not broken ground. Globally, the gap looks even bigger.

The research firm, Sightline Climate reports:

Data center outlook: half of 2026 pipeline may not materialize

“We’re tracking 190GW across 777 large data centers and AI factories (>50MW) announced since 2024. At least 16GW of capacity is slated to come online in 2026 across roughly 140 projects. Yet only about 5GW is currently under construction. Around 11GW remains in the announced stage with no visible construction progress, despite typical build timelines of 12–18 months.

Projected delivery dates are getting harder to trust. In 2025, 26% of expected capacity slipped, and another 10% of projects pushed back their commercial operation dates without much notice.

Given that track record, it wouldn’t be surprising if 30–50% of the capacity slated for 2026 ends up delayed.”

source: https://www.sightlineclimate.com/research/data-center-outlook

That gap, the gap between announcement and construction has a name, and a long history.

Charles Hugh Smith made the case this week that the AI data center mania rhymes with the railroad mania of the 1870s, when the first transcontinental line convinced investors that any track laid anywhere was a license to print money. It wasn’t. The collapse that followed earned the original name “The Great Depression” before the 1930s claimed it. Smith calls the mechanism by its proper term:

“The term for speculative frenzies channeling vast sums into investments with difficult-to-assess risk profiles is mal-investment, and mal-investment on a large scale triggers financial panics and economic depressions in a well-understood feedback loop.”

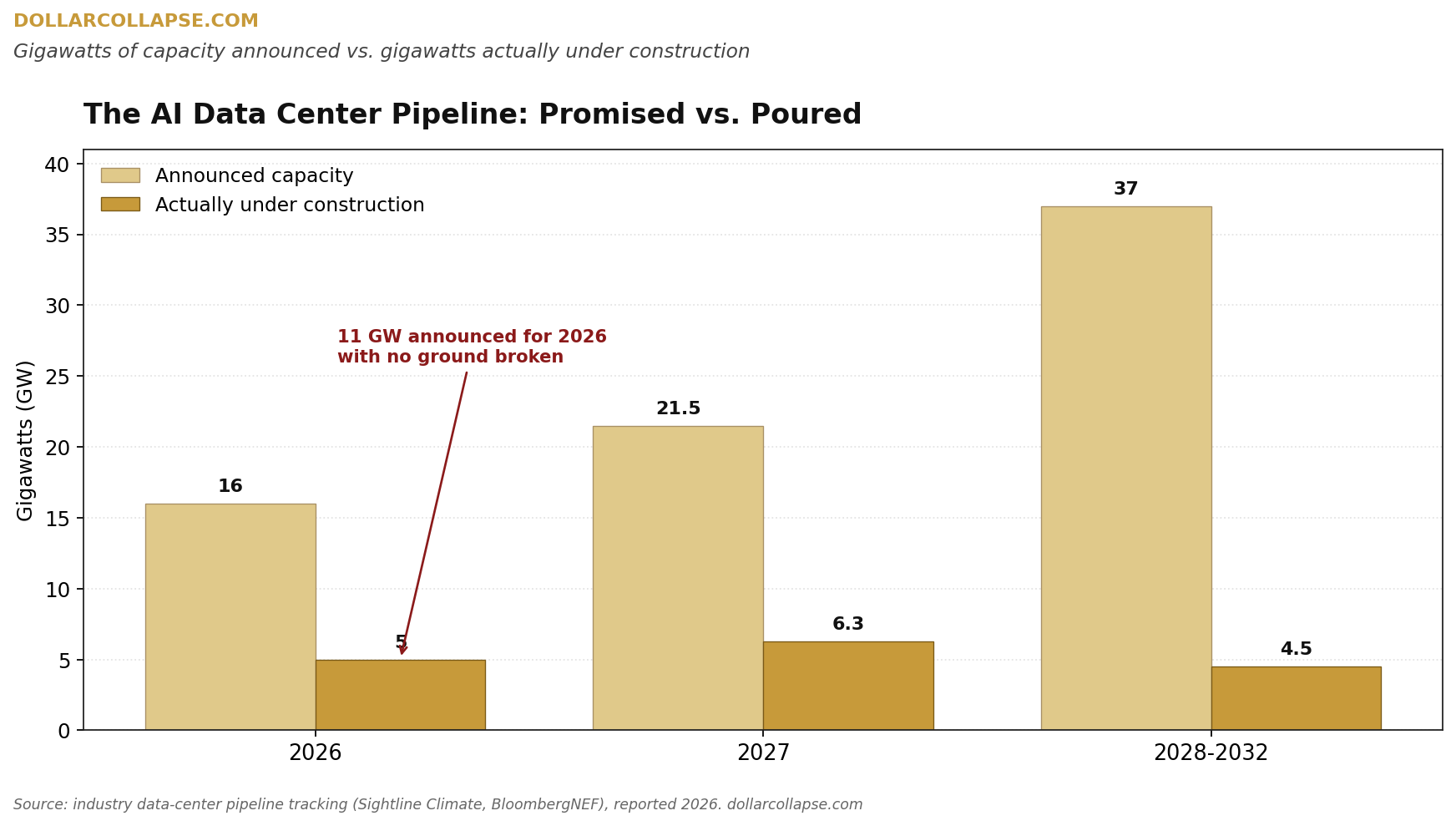

So, since we’re looking at what mal-investment may look like in the future, the most recent data on actual follow through, concrete poured etc., will show us what we want to know. We already saw the 2026 numbers – 16 gigawatts promised, 5 delivered.

For 2027, operators have announced 21.5 gigawatts and broken ground on 6.3. For the 2028 to 2032 window, 37 gigawatts are planned and 4.5 are under construction. Stack it up and more than 50 gigawatts of announced capacity has no concrete behind it.

Now for the power bottleneck. The US interconnection queue runs about five years from application to switched on, while a data center itself takes 18 to 30 months to build. You can pour the slab and still wait years for the grid to say yes.

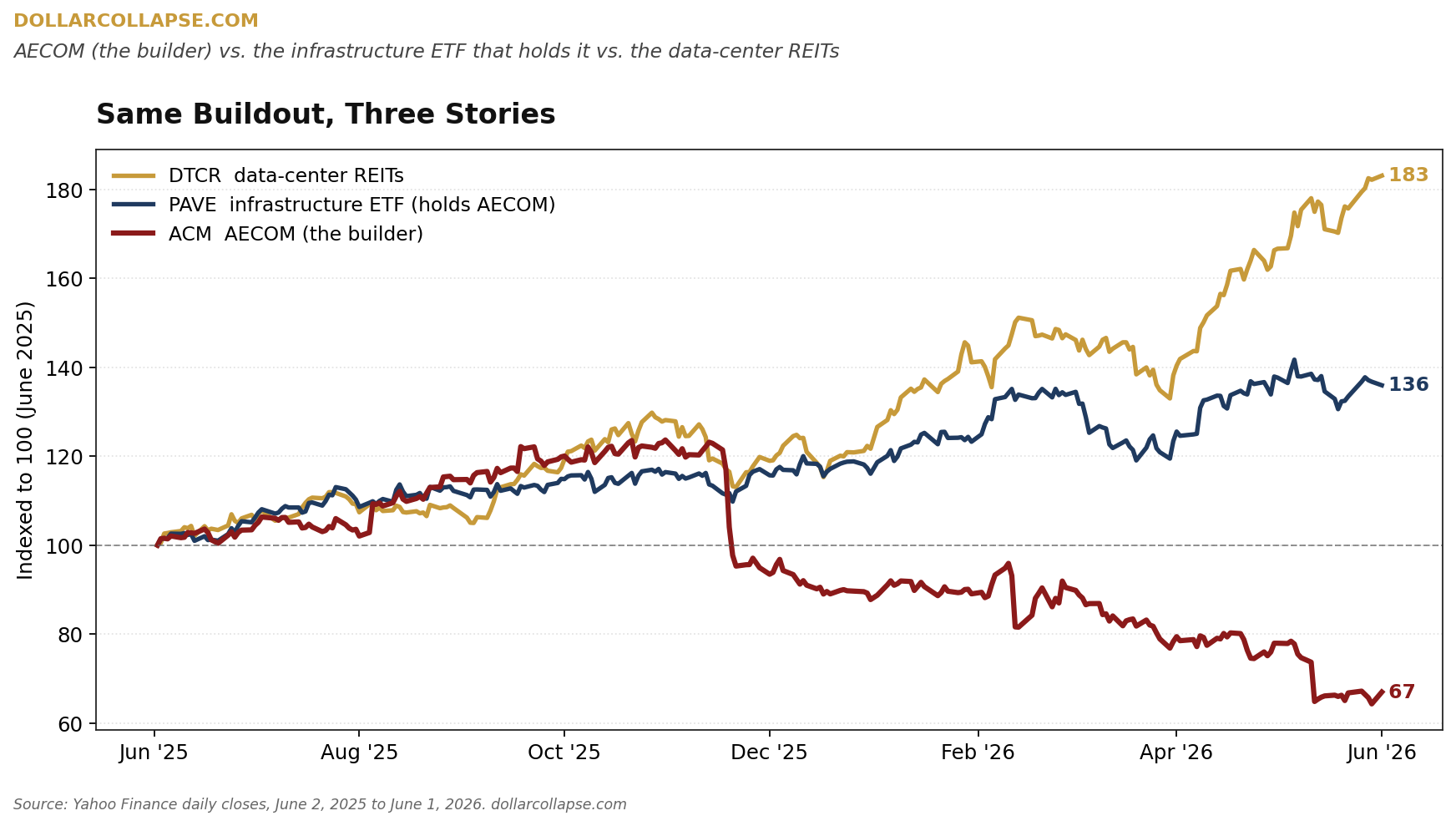

Which brings us to AECOM, one of the biggest billion-dollar companies laying the concrete to build these things…

On May 12 it reported a record fiscal-second-quarter backlog of $26.2 billion, up 8 percent, its 22nd straight quarter booking more work than it burned. Record margins. Record adjusted earnings. It raised full-year guidance for the second quarter running and named data centers as a driver. As an example, AECOM Tishman is the general contractor on DataBank’s 192-megawatt campus in Culpeper, Virginia, a 1.4-million-square-foot build that was contracted in 2024 and is not due online until the first quarter of 2027. By every line on the income statement, AECOM is winning the buildout.

However, the stock closed June 1 at $72.25. That is 46 percent below its October high and down a quarter on the year.

Here is what you want to pay attention to: Cash.

AECOM’s operating cash flow from continuing operations fell to $4 million in the quarter, down from $190.7 million a year earlier, and free cash flow turned negative at minus $27 million. AECOM blames delayed Middle East payments and a one-time charge on a discontinued project and expects the cash to recover, but the company is also sitting with a record backlog in orders.

Zoom out and you can see AECOM compared to the larger group of data center infrastructure provider in the PAVE ETF. Also, the data center REITs, stocks collecting on rent via data center income, represent the expectations of what investors believe will outperform in the future.

Indexed to a year ago, the data center REITs, the landlords who collect rent on the buildout, are up 83 percent. PAVE, the infrastructure ETF that holds AECOM, is up 36%. AECOM, the firm doing the physical work, is down 33.

This is the “K-Shaped” Construction of AI Data Centers.

All a backlog of orders does is record promises. So, this is what the market is doing.

It’s repricing those promises for the one big player whose revenue depends on orders transforming into poured concrete.

Read it as one data point in a longer story. Investors are committing capital at railroad-mania scale to assets that may be obsolete before they are energized, and the people closest to the start of construction feel it first.

This is what mal-investment looks like from the inside, before the feedback loop kicks in.

One thought on "The “K-Shaped” Construction of AI Data Centers"

Looks like the ROI isn’t going to keep up with the potential. I’ll stick with silver, gold, toilet paper.