Written by Bryan Lutz, Editor at Dollarcollapse.com:

Alright, it’s Sunday.

Here’s what we do.

Every Sunday I share a few thoughts with you, and other subscribers at Dollar Collapse.

Sometimes we’ll talk about economics, sometimes recent events, and other times, life.

Here are three thoughts for this morning:

1. Americans are suffering record-breaking losses in gambling. Here’s why they’re willing to bet so much…

Americans are gambling AND losing more than ever.

Since 2020, losses have gone up almost $100B, which sets them on track for over $250B.

Yes, prediction markets like Kalshi and Polymarket have influenced the betting markets, but that doesn’t explain why Americans are so willing to throw it all away.

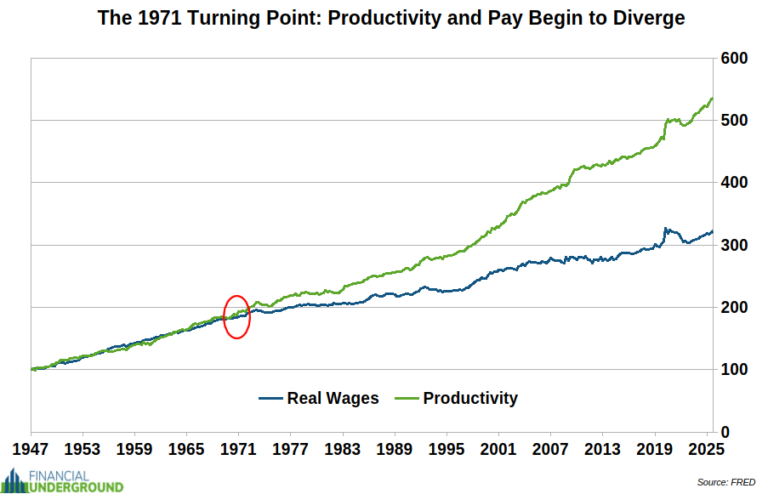

Below is a chart that shows the losses. Below that is a chart that shows why.

Since 1971, productivity and pay have gone their separate ways. Workers produce more every year, while real wages barely move.

That was the year Nixon cut the dollar loose from gold, and the year saving stopped working. When wages can’t keep up with the cost of living, the slow road to wealth closes. The only thing that’s left is the fast lane.

A $50 parlay on polymarket, or betting on the next NFL game isn’t entertainment anymore. For a lot of Americans, it’s the only ladder they can see, and they’re willing to take their chances.

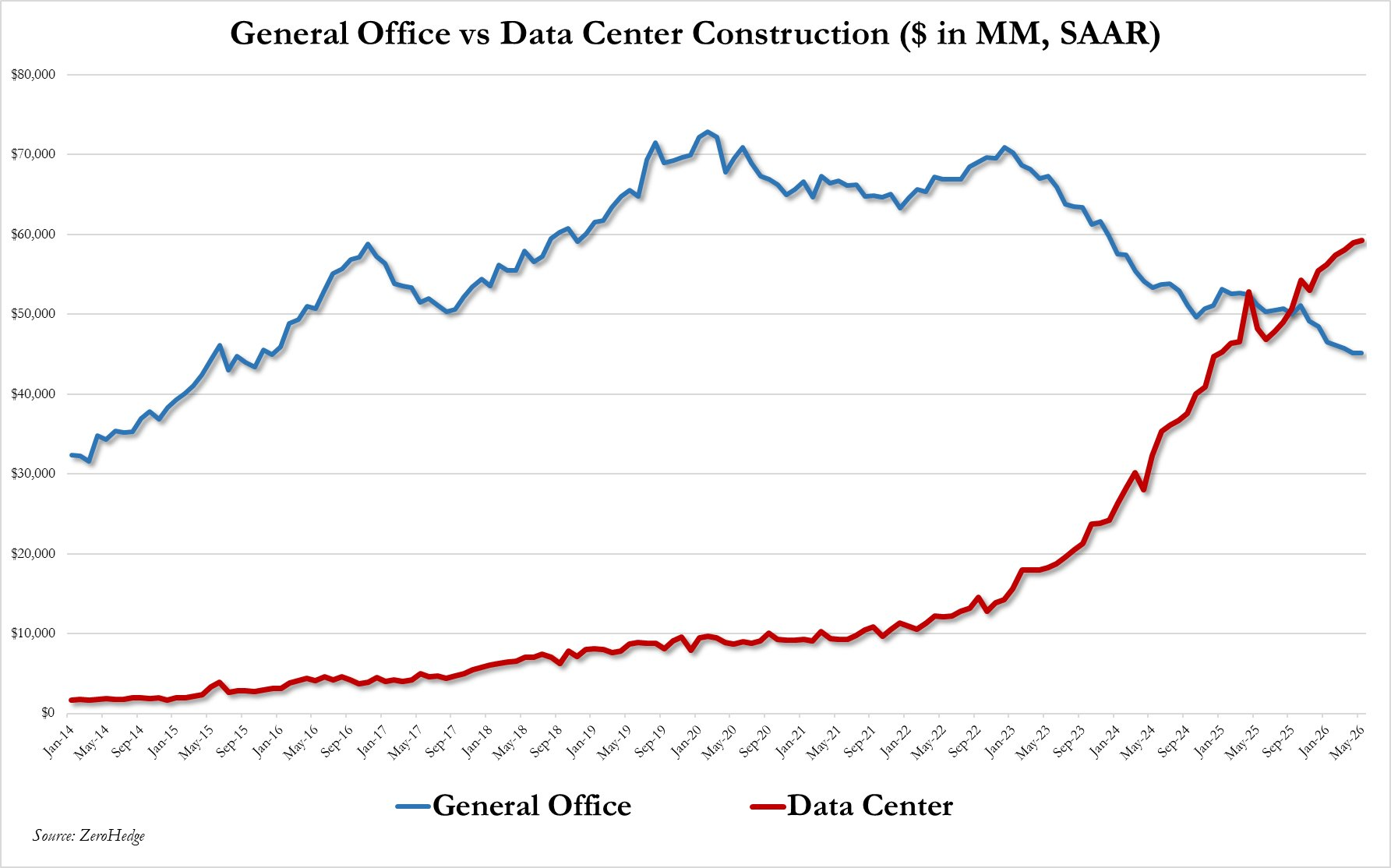

2. The rapid construction of AI data centers shows just how fast the bubble has grown. The good, long-term profit is on the back end, which is growing now.

Last year, the construction of data centers started to outpace the construction of general office space. Most of us remember that. That’s when ZeroHedge shared the chart below. In the past, I’ve shared just how many data centers have been promised, but not yet built. But some have been built, and there are specific companies already generating revenue from their maintenance. And those companies enjoy regular, steady cash flow from the arrangement. One large, global conglomerate has been servicing these AI data centers, and completed the purchase of a company for $4.75B that will help them to expand those services, even into other industries, globally.

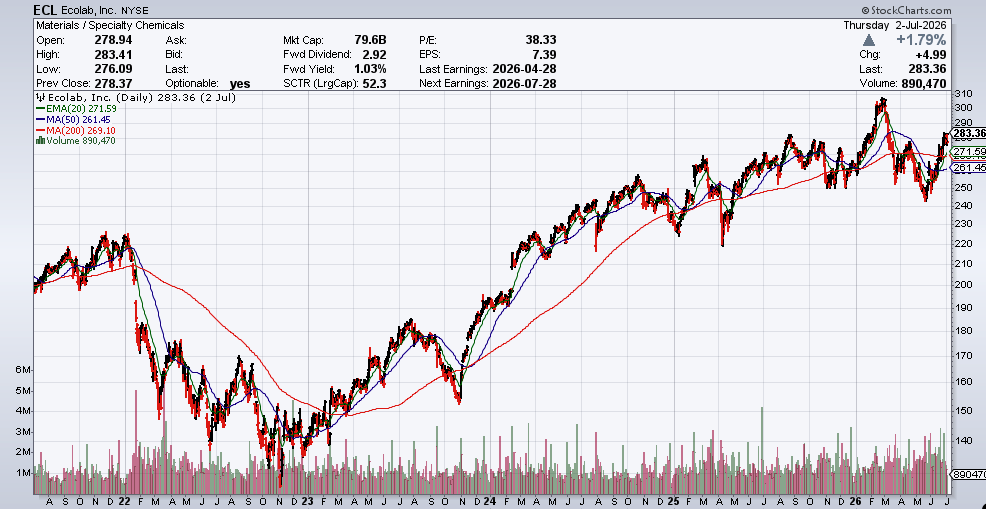

That company is Ecolab(NYSE: ECL).

On July 2, 2026, they completed the acquisition of CoolIT Systems for ~$4.75 billion cash.

If you’re interested in reasonably safe backdoor exposure to AI data centers, this is one of them. Ecolab’s services are positioned on the back-end of the growth curve. So, once these data centers are built they receive continual revenue.

Here’s how Ecolab’s recent acquisition is expected to affect their profit.

What you’re seeing here is no AI fantasy story. The company recovered after 2020 with the rest of the stock market. AI and data centers are just now entering the company’s story.

CoolIT’s year-to-date sales have reportedly grown more than 100% on AI liquid-cooling demand, and Ecolab’s Global High-Tech business (which now houses CoolIT plus the earlier Ovivo deal) is approaching ~$1.5 billion in 2026 annualized sales, up from about $150 million in 2021. Ecolab is targeting that unit to reach $4 billion in annual sales by 2030 at ~25% operating margins. It’s now described as the company’s largest growth engine.

Cooling can represent up to 40% of data center operating costs, and as AI pushes rack densities past what air cooling can handle, direct liquid cooling becomes essential. Ecolab’s plan is to scale CoolIT globally by pushing it through Ecolab’s existing sales network — pairing CoolIT’s cooling hardware with Ecolab’s water-chemistry and service expertise.

As a bonus, the company generated $1.9 Billion FCF in 2025.

From what I am reading, some analysts are a buy up to $325.

But the stock is more of a long-term hold. As of right now, the stock provides:

- An annual dividend of $2.92/share ($0.73 quarterly), yielding roughly 1.1%

- A payout ratio at a comfortable ~37% — plenty of coverage

- And a 89-year history of consistent dividend payments with 30+ consecutive years of increases.

In my opinion, Ecolab(NYSE: ECL) is a great, long-term income stock with expectations to grow as more data centers are implemented.

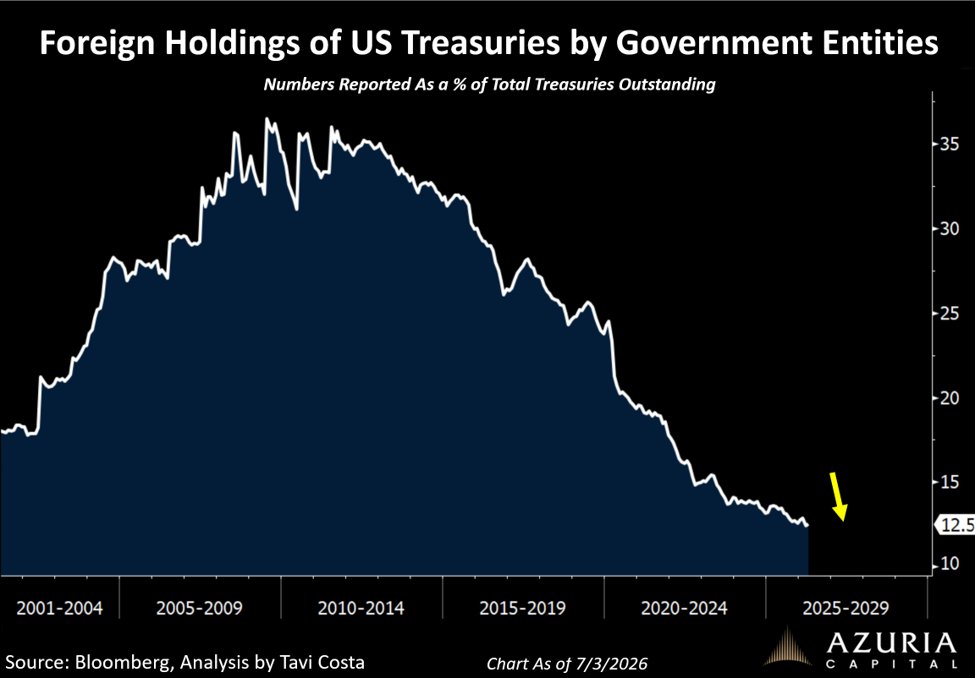

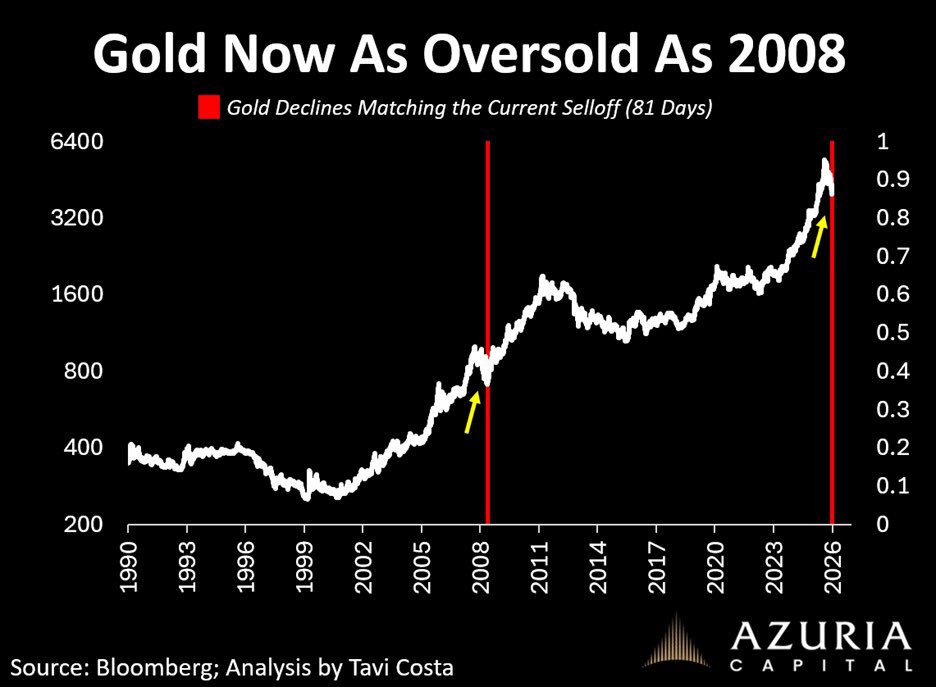

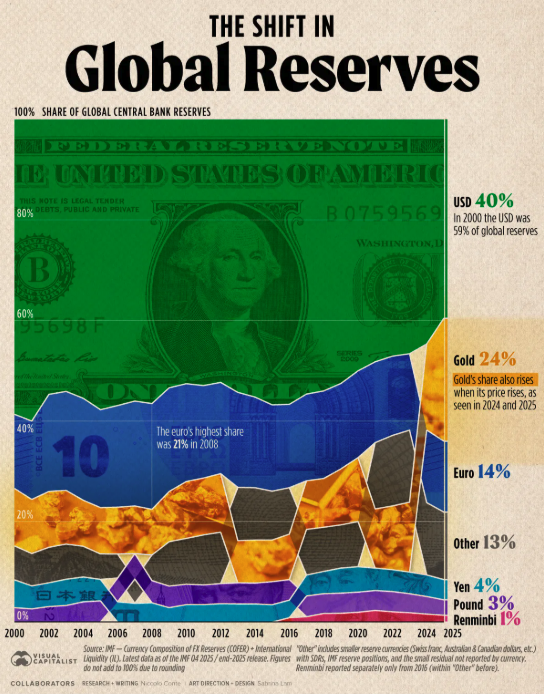

3. Fewer and fewer foreign buyers want US Treasuries. Gold is currently most oversold since 2008. Yet, Central Bank gold reserves keep climbing. This should tell you something.

As long-term gold and silver stackers, we want to look at the bigger picture. So, instead of looking day-to-day, or even month-to-month at what the Fed chooses to do with interest rates, or the value of the US dollar, we look at something else.

We are looking at reserve assets – what central banks and governments are choosing to store their wealth in.

For the past several decades that store of wealth has been US Treasuries, because they are liquid and central banks receive a return. But now, less governments trust US Treasuries to hold their value. We have seen a huge downward slope since Quantitative Easing kicked in around 2009.

Now, the current mindset in the market has been to sell off gold. Bankers and investors are expecting the Fed to raise interest rates come September. So much so that gold is as oversold as it was in 2008. (And look what happened after 2008).

Make no mistake. Kevin Warsh has some tough choices to make, but I am doubting the “tough guy” act he’s playing against inflation. The markets are fragile. Hiking rates will do damage… Job losses…Bankruptcies…Bank runs…etc. Whether he’s the guy to do that or not remains to be seen.

Meanwhile, Central Banks will keep selling off fiat currencies and treasuries to buy gold. This should tell you something about where gold is heading next.

Have a great Sunday.