***Obligatory forward-looking statement: This is not investment advice. Anyone considering what is said in this email or from the author should consult a licensed financial advisor before taking action or making any purchases.

Written by Bryan Lutz, Editor at dollarcollapse.com:

I hope you’re having a restful Sunday.

Here’s what we do.

Every Sunday I share a few thoughts with you, and other subscribers at Dollar Collapse.

Sometimes we’ll talk about economics, sometimes recent events, and other times, life.

Here are three thoughts for this morning:

1. Fund Managers are the most all-in(risk on) in the markets than they have been in the past twenty years. Here’s the contrarian play.

This is another sign of the top.

A 10% reading has historically been the kind of complacent, fully-invested extreme that shows up near tops, not bottoms.

Just before the Great Financial Crisis in 2008, Bank of America’s Private Wealth allocators were sitting around 11% cash as a percentage of portfolios. They were all in, in the equity markets.

Then after the crash, fear crept in, reality slapped them in the face, and fund managers became conservative, looking for a bottom.

Fund Managers are now sitting on the lowest cash allocation in history 🚨 pic.twitter.com/fYLQ6Ev2Vu

— Barchart (@Barchart) July 7, 2026

The contrarian play here is… drumroll…

To hold a good amount of cash.. dry powder. 🙂

2. The more I look at water stocks, the more interested I get.

Last Sunday, I highlighted a blue chip, water-related stock that had recently made a $4.5 Billion cash acquisition to service data centers.

That company was Ecolab (ECL). That got me curious…

What are other water-related companies that may also be great long-term holds?

Well, this could be one…

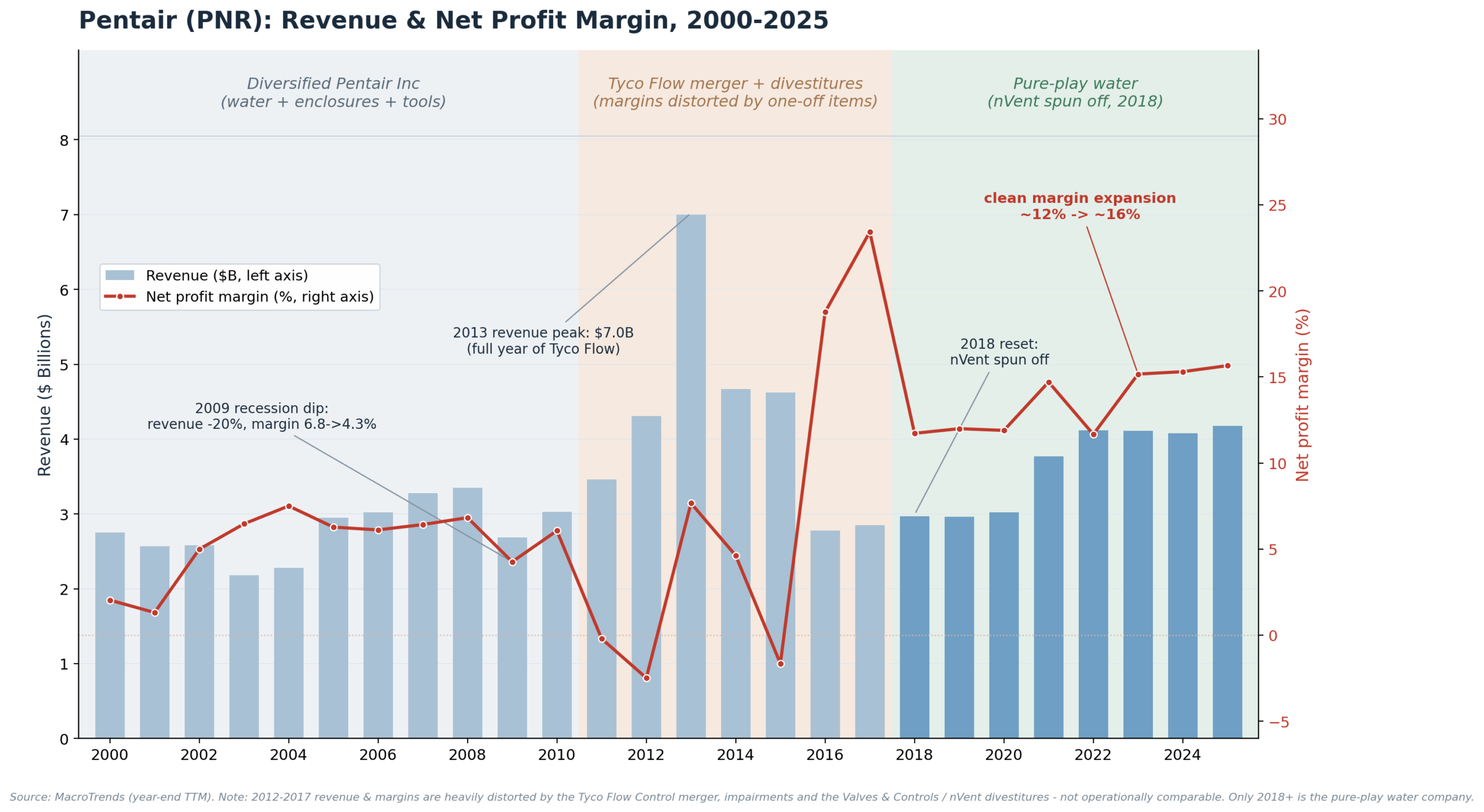

It’s called Pentair (PNR). Recently, its been moved into the spotlight because everyone wants in on the AI / data center play.

The thing is, this one has very little exposure to data centers.

Pentair just took a dive.

The stock’s trading well below its 200-day, down near $76 from triple digits…

The reason? Cyclical fear.

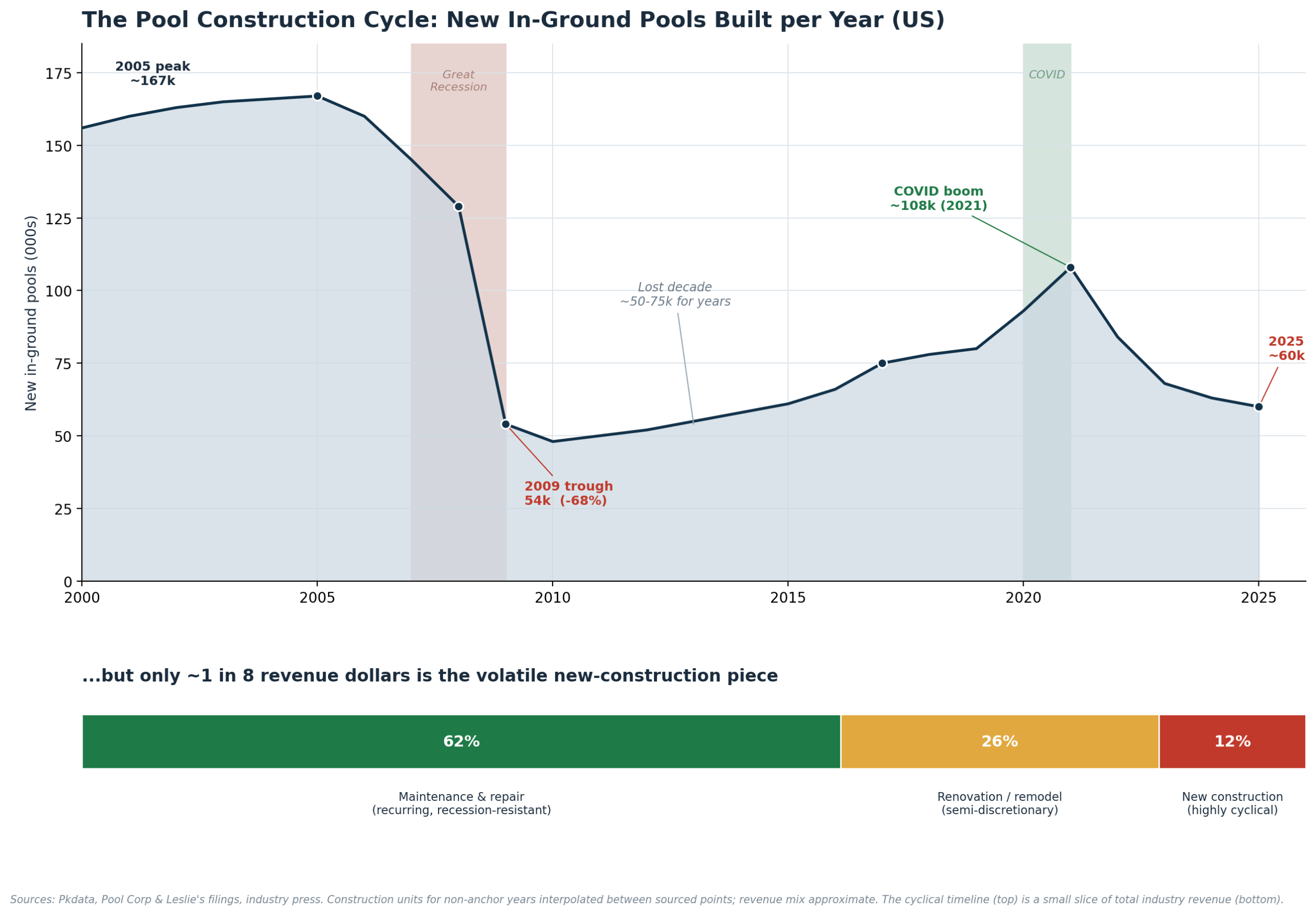

Wall Street sees a soft housing market and assumes the pools stop getting built.

But pool is barely a third of Pentair’s revenue, and most of that is parts and maintenance, not new construction.

New builds cratered after 2008, and again after the COVID boom… yet the aftermarket kept right on humming.

You see, there are roughly 14 million pools in America.

And once one’s in the ground, you maintain it, because letting the mold and algae win costs a lot more than a new filter. Residential pools might go DIY, but only for about a year or so. That’s what happened after 2008.

Now, Pentair(PNR) is a company that dumped industrial electricity after 2008, went all-in on water, and expanded its margins the whole way. Today the company’s growth is focused on M&A, raising prices, expanding margins, and maintaining a 49 year record of dividend payouts.

Here’s a quick run down:

Price: $76.19, giving the company a market capitalization of $12.31B, with a P/E multiple of 18.30. It’s near the bottom of its 52-week range of $69.93 to $113.95, which is down about 27.5% over the past year, which is the cyclical-fear sell off.

Dividends: $0.27 per share quarterly ($1.08 annualized), a yield of roughly 1.36–1.4%. The headline: this is its 50th straight year of dividend growth. That milestone will make Pentair a Dividend King, which is a step up from Aristocrat. It’s very conservatively funded: a ~25% earnings payout ratio and ~23% cash payout ratio. Right now, its dividend pays out higher than the S&P.

Free cash flow: Roughly $746M in FY2025 (up ~8% year over year), on operating cash flow near $815M. Management targets converting close to 100% of net income to free cash flow.

Return on assets: approximately 9–10% (net income ~$654M against ~$6.9B total assets). For context, the return picture is stronger on equity — ROE runs about 17.6% — with gross margin near 41.9% and net margin around 15.6%.

So the market drained Pentair on a false assumption, and fear that doesn’t hold water.

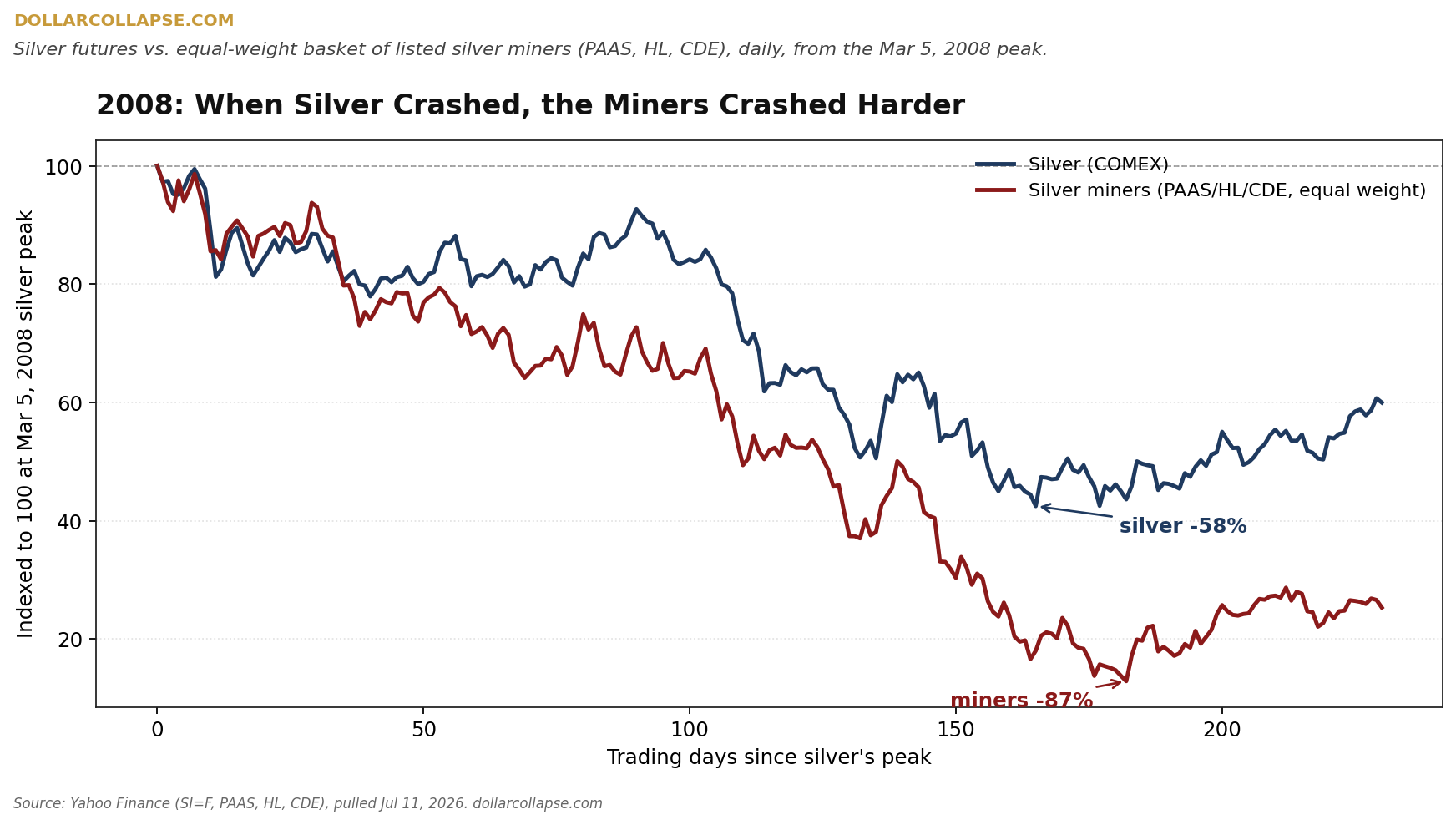

3. Silver is down 48% from its January top. In 2008, the miners crashed harder than the metal. This time they refuse. That should tell you something…

In 2008, silver fell 58%.

The miners fell 87%.

Equity investors led the panic, and a metal bottom took months to form.

Here’s what that crash looked like:

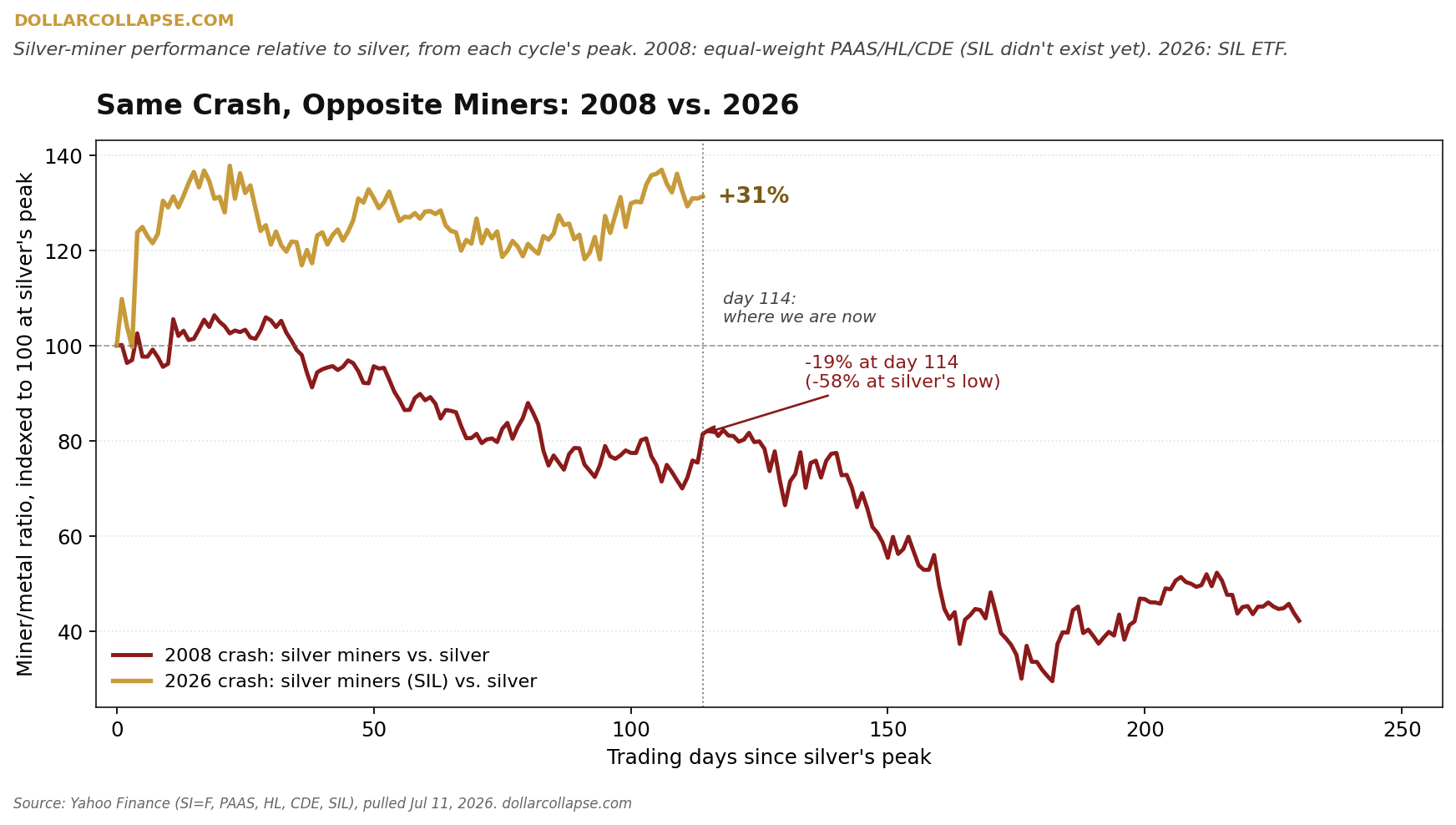

Now look at today.

Silver is down 48% from January’s $115 top. The miners? Down 32%, and GAINING 31% against the metal:

Same crash in the metals, opposite the miners.

In 2008, the paper panic spread to the producers. Paper hands got shaken out at the producer level.

This time, the miners are holding up. Those who placed allocation into the miners last year know their worth, and they aren’t selling. This time really is different.

***This is not investment advice. Anyone considering what is said in this email or from the author should consult a licensed financial advisor before taking action or making any purchases.