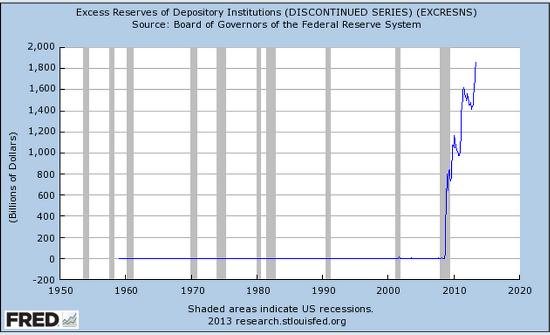

In normal times, today’s combination of record low interest rates and massive infusions of capital into the banking system would ignite the mother of all expansions. That it hasn’t has confused the economists whose textbooks clearly state that it should. And it has convinced the Fed to just keep upping the ante with QE after QE, so that bank excess reserves, which are historically around zero (because lending out as much as possible is how banks make money) have risen to completely unprecedented levels.

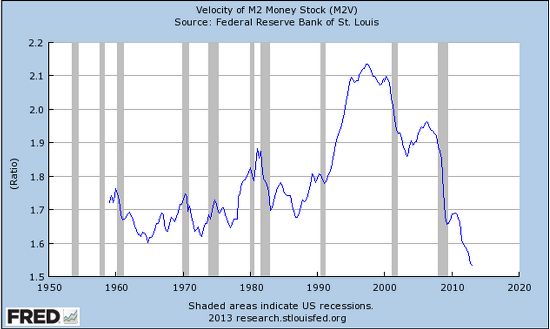

The reason these reserves haven’t found their way into loans and then into consumer spending is that five years ago most banks nearly died and many consumers nearly went broke, and neither group was going to forget the experience soon. So the velocity of money – the rate at which each existing dollar changes hands via loans and spending — sank to historic lows that are a mirror image of money creation and bank reserves.

But that may be about to change. Home prices and stock indexes are soaring, which makes consumers and small businesses both a lot more creditworthy and a lot more interested in leverage. Banks, meanwhile, are finally realizing that they’ve left a ton of money on the table by not writing mortgages and business/personal loans into the strength of these nascent asset bubbles. And the only thing that scares a banker more than future massive defaults is being left behind by a boom in the current quarter. They’re reacting, as they always eventually do, by looking to lend:

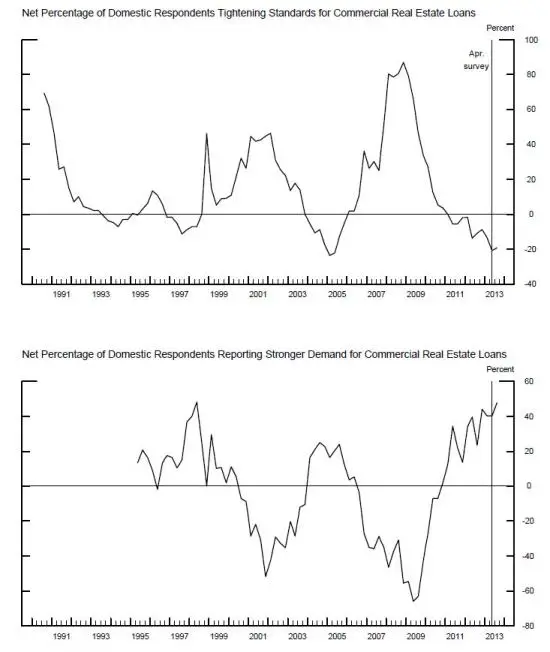

Fed Survey: Banks eased lending standards, “experienced stronger demand in most loan categories”

From the Federal Reserve: The July 2013 Senior Loan Officer Opinion Survey on Bank Lending Practices

The July 2013 Senior Loan Officer Opinion Survey on Bank Lending Practices addressed changes in the standards and terms on, and demand for, bank loans to businesses and households over the past three months. The survey also contained special questions about changes in banks’ lending standards on, and demand for, the three main types of commercial real estate (CRE) loans over the past year, and on the current levels of banks’ lending standards for many types of business and household loansrelative to longer-term norms. In the July survey, domestic banks, on balance, reported having eased their lending standards and having experienced stronger demand in most loan categories over the past three months. This summary is based on the responses from 73 domestic banks and 22 U.S. branches and agencies of foreign banks. Regarding loans to businesses, the July survey generally indicated that banks eased their lending policies for commercial and industrial (C&I) and CRE loans and experienced stronger demand for such loans over the past three months … The survey results also indicated that banks eased standards and terms on, and saw increases in demand for, some categories of lending to households. Modest net fractions of respondents reported having eased standards on prime residential or nontraditional mortgage loans, and a large net fraction indicated that they had seen increased demand for prime mortgage loans. A moderate net fraction of respondents reported that they had eased standards on auto loans over the past three months, and small net fractions indicated that they had eased standards on credit card loans and other consumer loans. Demand for all three types of consumer loans asked about in the survey had reportedly strengthened, on balance, over the second quarter.

What does this mean? Just that human nature is unchanging. We relive our most recent intense experience until a new intense experience pulls us in. That’s where booms and busts come from, and that’s why they’re getting bigger. Each bust is more severe and takes longer to get over, which forces panicked governments to try even harder via deficits, money creation and interest rate manipulation, to make us forget.

Eventually the boom/bust amplitude will become overwhelming. An asset bubble will broaden into an Austrian crack-up boom. Or a bust will be so deep and pervasive that it becomes a decade-long Kondratieff winter.

There’s no guarantee that this incipient pick-up in lending will turbocharge the current asset bubble. It could be a false alarm, to be followed by another downturn (there are plenty of data points suggesting that this is the case). But if so, the world’s governments and central banks will just up the ante again. Because fiat currency is essentially play-money, the numbers can be as large as the owners of the printing press care to make them.

So while the fiat currency bubble is clearly entering a new chapter, it’s not yet clear what the chapter is.

13 thoughts on "Are Banks Finally Ready To Start Lending?"

All that is missing from the inflation-to-be scenario is a higher velocity of money. That being the proverbial floodgate that releases the flood of dollars into the system. The catalyst will be the wealth effect of consumers, businesses, and banks satisfied in the belief that the “recession” is over and its time to party again.

Yes, but can (and, therefore, will) that happen “again”? The boom-bust cycles can’t go on forever, or can they, or is this time still not the last? There is a reason that no fiat currency (i.e., objectively baseless money yet decreed by law) hasn’t lasted more than about 90 years (we’re at 100 years and counting, probably because the US dollar is/has-been the reserve currency – a unique situation.)

Yes, of course they are. It’s how they manufacture debt money and make a profit. They’ve been able to to do this for the last five years (Indeed, I re-mortgaged last year). But they haven’t. Why? Among many reasons, one would suspect it’s because they’ve been making reasonable medium term profits gambling, via algorithmic robots, on the ‘pumped’ stock market. Easy, low risk, & offset. Bank reports certainly suggest they’re doing OK (Albeit well massaged accounting). Aren’t they wholly, and hungrily, tied to central bank policy? If Bernanke carries out his threat to ‘Taper’ then maybe the market will go through a brief, horrific crash, and a couple of majors may even go pop. Then it’ll be game on. Again. Exactly what SHOULD have happened back in 2008. Investment arms, segregated from retail operations, will probably take a hit. But they’ll amalgamate again in the future.

The game changer, for me, this time around, will be the rest of the world and how willing they will be to deal in US Dollars. Will Russia continue to sell it’s energy in US Dollars? Will the Saudis? Will China want to dump some more of it’s ‘Worth a lot less’ dollars/Bonds in exchange for real stuff? It’s difficult to foresee an imminent line of foreign sovereign wealth/pension funds lining up to purchase US dollar denominated debt at the moment (Government or private repackaged mortgage backed shit). Especially considering the way it’s custodian has been acting of late. Saying all that, humans are strange creatures…

I think that one of the reasons it has been so hard to predict financial and economic events since 2008 is because the fiscal and monetary interventions worldwide have been so inherently contradictory. The effort to increase bank lending is a good case in point. The monetary policy efforts to lower long term interest rates, increase bank lending, and to create inflation are incompatible. Banks lend according to the steepness of the “yield curve” and the demand of credit-worthy borrowers, not because of reserves. Since ’08 the yield curve has been “flat” (which means that long term interest rates have been relatively low compared to short-term rates, so “borrowing short” and lending long” is another version of reward-free risk for banks) and there has been relatively little borrowing demand from credit-worthy borrowers. Two things are beginning to change: Long term interest rates are rising while short-term rates are being held down AND banks are beginning to loosen their lending standards to service less credit-worthy borrowers. (The financial arm of General Motors, in particular, has been lending to sub-prime borrowers since late 2009, which helps explain why GM has “recovered”.) But there is a another way to parse this change, which is to say that inflation expectations are rising too. It’s one thing for a borrower to go laughing all the way to the bank (pun intended) about getting a 30 year mortgage at 3%, but what of the bank on the other side of that deal. (Answer: Fannie Mae and the willingness of the Fed to buy all the mortgage backed securities from the banks.) Normally no entity in its right mind would lend for such a time span at those rates, but now that inflation expectations are rising so are interest rates, and as long as their risks of lending to less credit-worthy borrowers can be off-loaded to US taxpayers then banks are now more willing to lend.

I suspect this will prove to be a short-term trap, that the same results will follow the same reflationary efforts, that all the stimulations are finally creating a final blow-off euphoria (though incredibly subdued compared to the costs involved) and a much needed bear market and deflationary adjustment period is still inevitable and maybe even imminent.

If not – if the economy is poised to scale new heights – I’ll eat my proverbial hat. I just can’t see how all the fraud and corruption, political hypocrisy and evasion, irresponsible spending and debt, destruction and waste from war, overall cultural depravity, and massive abuse of the monetary system can possibly escape their repercussions, regardless of the alleged new energy and manufacturing “boon” in the US.

By the way, as an aside, it’s common to read that all of the Fed’s purchases simply increase the bank’s reserves. That’s not necessarily true, it depends upon what the Fed buys and from whom. Currently, most of the MBS (mortgage backed securities) the Fed is buying as part of its QE program is bought from the primary dealer banks, who own them and probably even securitized them themselves, and those proceeds generally are saved as reserves or used for financial speculation in something less toxic than MBS. However, the $45 B per month of Treasury bond purchases by the Fed goes to the US Treasury to cover its deficit spending. That money goes out to the “real” economy, not into bank reserves, and is arguably price inflationary.

Another reason bank reserves are not, or at least have not been, lent out is because they are a balancing asset against ever increasing liabilities. Remember, the backdrop to the whole global macro economic situation is deflationary. Deflation is the big bad bugaboo for the existing monetary system. All of the stimulations and QEs and OMTs and “Abenomics” is about offsetting the elimination of debt (the death of fiat money) either through voluntary repayments (instead of increased consumption spending and debt) or defaults (e.g., foreclosures, bankruptcies, write-offs, etc.) Because of the suspension of normal accounting rules since 2008 those liabilities can remain “off the books” and not “marked to market”. Nevertheless, for those who know, those liabilities are real but as long as the bank has “reserves” then the game of inflationary attrition can go on. So those bank reserves are not as available for lending as they might seem.

Hey John Rubino: Banks don’t loan money. Bankers lend credit that they create out of thin air when the duped debt-slave signs the loan documents. All so-called “money” in our system is debt. The banking system in the Western world is simply a legalized counterfeiting, debt-enslavement scam. If you want to help your fellow men escape this futile treadmill of needless labor and suffering, please start using realistic descriptions of Banking in your articles.

Lets just skip this chapter and go to 0; we are going there anyway. Break these over blown rent seeking pirates up and get rid of free trade that has lowered the standard of living, which created the debt to buy the houses in the first place.

The empire is broke and they are selling our assets to the lowest bidders who have our money that they made from the free trade deals we made.