Since at least the 1980s, US policy has been to convince us to borrow as much as possible on pretty much anything we could think of. This worked brilliantly until 2008, when homeowners, consumers and businesses hit a wall and private sector defaults began to exceed new loans. Another Great Depression was imminent.

But instead of allowing this natural cleansing process to run its course, governments around the world stepped into the breach themselves, borrowing tens of trillions of dollars to replace evaporating private sector debt. The idea, to the extent that there was one, was to buy time for traumatized consumers and businesses to relax a bit and start borrowing again.

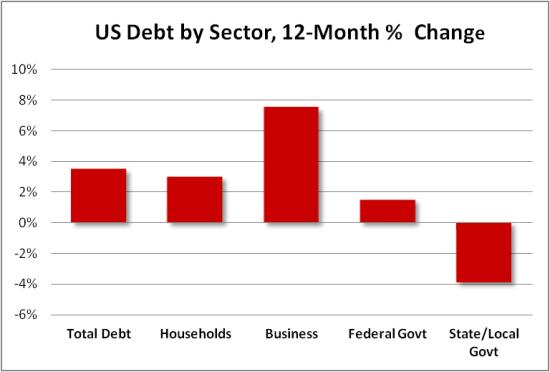

This appears to be happening. The latest Fed Z.1 report shows overall US debt growing again, with the private sector leading the way.

It’s not surprising that near-zero interest rates and trillions of dollars of newly-created currency would get people borrowing again. What is surprising is that anyone thinks this is a good thing. In 2013 total US debt, equity prices, household net worth, large-bank assets and derivatives books, and a long list of other debt-related measures pierced the records they set in 2007. In other words we’ve recreated the conditions that prevailed just before the world nearly fell apart.

Will the result be different this time? It’s hard to see how, especially since developed-world governments now have roughly twice as much debt as they did back then, so their ability to ride to the rescue will be limited.

As this is written the Fed is announcing that it will scale back its debt monetization to only $75 billion a month, or $900 billion a year. Its balance sheet, which just hit $4 trillion, will grow by nearly 25% in 2014, to nearly $5 trillion, which is a measure of how much new currency it is creating and pumping into the banking system.

The next stage of the plan is to get the banks to start lending this money, which would, through the magic of fractional reserves, produce loans in some large multiple of the original amount. So we might be on the verge of trading a nasty-but-comprehensible Kondratieff Winter for something a lot wilder.

8 thoughts on "The Private Sector Is Borrowing Again – And That’s Not Good"

Who cares….. Everyone should borrow as much as possible. The sooner this m*t*er f*c*er burns down, the sooner we can rebuild it and rid ourselves of these politicians and begin anew with some statesmen. So, let us all borrow and party on. The only real solution at this point is for states to begin succeeding and that doesn’t look like it will happen; thus, HELLO CREDIT CARDS!!!!

Redeo ad fontes

Expat

seceding. My apologies, I was typing to fast.

Still typing TOO fast.

I can’t tell from the bar graph how much debt has actually increased, only that business borrowing has increased about 3 times as fast as household borrowing. Both debt levels may still be relatively anemic in absolute terms. Based upon my personal experience I can’t tell. All I know is that the roads are congested with vehicles, restaurants are full, it’s hard to find parking at the malls, both residential and commercial construction is everywhere, and expensive wedding venues are booked for at least a year, to cite a few examples. I don’t mean to sound glib or insensitive, but that’s what I see (at least in Miami). Maybe it’s mostly fueled by debt but it’s been going on for too long for that to seem possible. There are still credit limits. Go figure.

There are two charts at the end of the current issue of “Things that make you go hmm…. that everyone should see in relation to this post.

Taking on household debt could be done for optimistic reasons or because it’s the only way to make ends meet, and it’s hard to tell the difference from aggregate statistics. What if consumer credit increases are coming from cash advances used to pay bills? What if student loans are being taken out by young unemployed folks who view the money as a means of survival more than an investment in their futures? But in the mainstream news it’s always portrayed as bullish: the consumer is back!