If there is one job that no Austrian Economist will take up at this juncture, it would be that of the Federal Reserve Chair. The road ahead seems to be set in stone, and in a society that has been sold the idea that “printing currency units is a panacea to all problems” for nearly 45 years, doing the opposite is an invitation to get lynched. It is near certain that Kevin Warsh would go down in history as the Fed Chair who presided over the demise of the dollar. Perhaps as infamous as Gideon Gono, who presided over the Zimbabwean dollar’s hyperinflation.

Can anything be done at this point to prevent the imminent demise of the dollar? Of course, yes, and the advice would be no different from what the then Treasury Secretary Andrew Mellon suggested to Herbert Hoover in 1929: “Liquidate labor, liquidate stocks, liquidate the farmers, liquidate real estate. It will purge the rottenness out of the system”.

Of course, Hoover ignored Mellon’s sensible advice and turned what ought to have been a short, severe recession into the prolonged Great Depression of 1929 to 1946. Hoover pursued the most interventionist policies after the 1929 stock market crash, though by the standards set by subsequent U.S. presidents, Hoover might appear like a Laissez-faire Economist. Forget the Federal Reserve or the US Treasury, we don’t have an Andrew Mellon anywhere in the US administration today. The one Republican in the House of Representatives who understands these issues is Thomas Massie, and Trump is desperately trying to get him defeated in the primary. Not that one person can make a difference in the grand scheme of things. But this suggests that Trump is likely to adopt a policy framework equivalent to “Hoover on steroids”. Given the problems and the likely solution that would be pursued, the end result cannot be anything other than a high-inflationary economic depression.

The Inflationary Spike Ahead

Make no mistake – the price inflationary spike that lies ahead is a structural phenomenon that has been in the works for a few decades. Perhaps even from 1971 onwards. Attributing this to the Iran War or even Biden / Trump 1.0, notwithstanding the culpability, would be a genuine understatement of the problem.

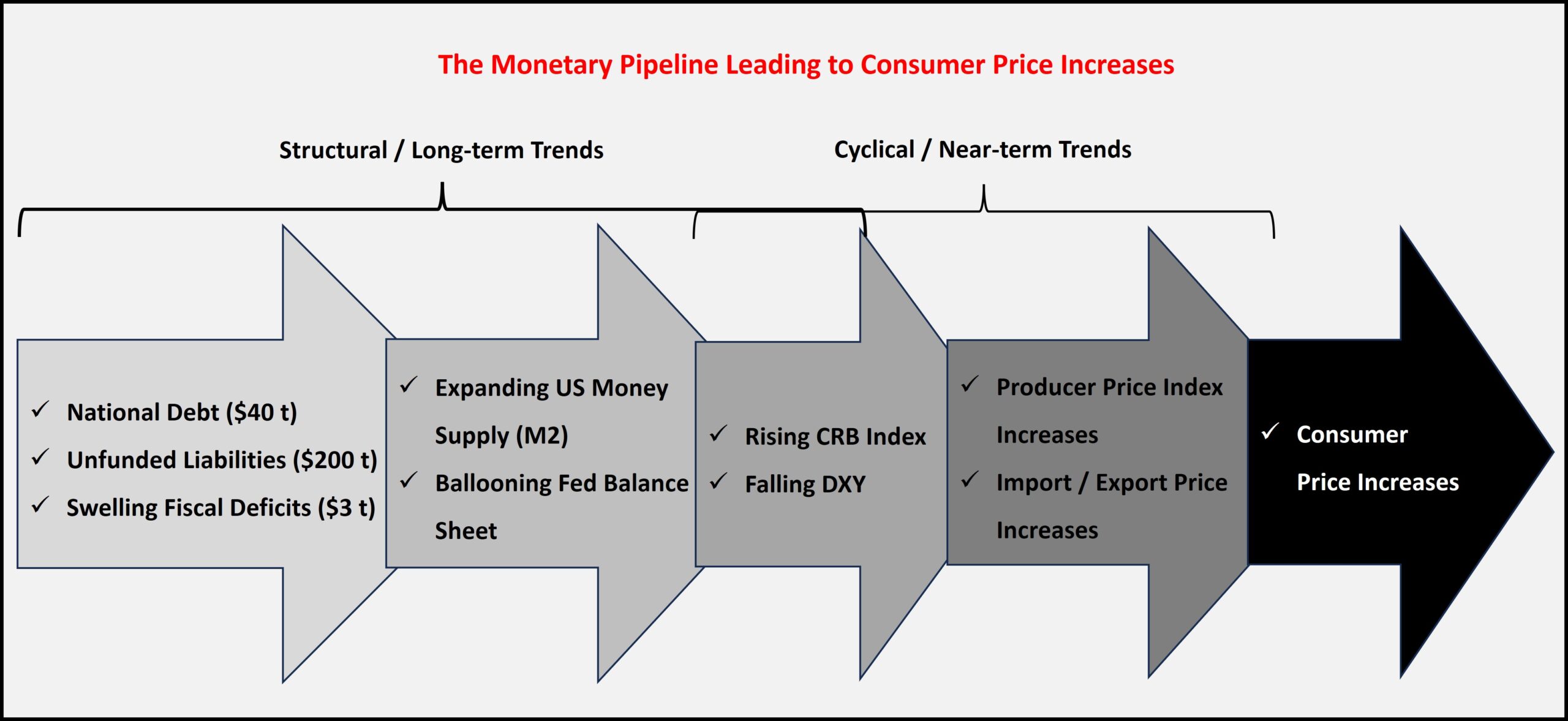

The monetary pipeline, as outlined above, ultimately leads to galloping price inflation and a loss of confidence in the currency. While with most currencies the translation of a weak fiscal policy into higher consumer prices occurs within a few years, in the case of the US, by virtue of its status as the world’s reserve currency, the translation has indeed taken a while. The US was able to export its monetary inflation, thereby giving its citizens a much higher standard of living than what their production ought to have enabled. This also necessarily meant that the standards of living of the non-US residents were suppressed by an artificially strong US dollar. That this narrative is nearing its end must be obvious to most.

The structural issues, i.e., the National debt, the trend of increasing fiscal deficits, and the money supply, have been extensively described in the media, and so I am not going to expand on them here. That said, a line on the recent increases in M2 might be worth recording. By March 2026, the US Money Supply M2 had recorded 25 straight monthly increases, which cannot bode well for the future purchasing power of the US Dollar.

What is of greater interest are the near-term factors that are aligning with the structural tailwinds of a loose fiscal and monetary system.

- The DXY, which was near 110 when Trump took office in Jan 2025 (and close to the high of the current decade of 112 set in Jan 2022), is now below 100. A 10% decline in the DXY within a year, especially for a President who campaigned on a strong dollar/reigning in price inflation, is a clear signal that Trump is doing the exact opposite of what he promised in the electoral campaign.

- The CRB index that was 350 in Jan 2025 had steadily increased to 410+ by Feb 2026. Since the start of the Iran war in Mar 2026, the index has jumped to 500+, indicating a near 45% under Trump 2.0 so far. Clearly, another nail in the coffin of stable consumer prices.

Even these two factors – DXY and the CRB Index – while more often than not translate into higher consumer prices, could still take 6 to 12 months to take effect. Better leading indicators are increases in the producer price index and import/export prices. These are also not subject to the usual CPI tweaks (hedonic adjustments, substitutions, etc.). And this is where the evidence is most damaging on what lies immediately ahead.

These numbers are monthly changes and clearly point towards substantially higher consumer prices in the next few months. We should not be surprised by double-digit, or at least high single-digit, consumer price increases by Q3 2026, even with all the juggling in the CPI calculations.

What Will Warsh Do?

What can he do? Can he hike interest rates by several hundred basis points to combat the surging price inflation? What will that do to the multi-asset hyper bubbles in housing, bonds, and AI stocks? I don’t think there’s any chance of doing anything close to what is necessary. And even a couple of hundred basis point hikes may not be sufficient at this juncture. Remember, Volcker had to offer a real interest rate of 8% to combat the price inflation of the 1970s. Even a nominal 8% yield on the Fed funds rate is not even under theoretical consideration for the US today.

Kevin Warsh is walking into an Inflationary Tsunami armed with nothing more than an Umbrella.

The Gold Redemption

The treasury market had it correct. The 30-year treasury rate crossed 5% for the first time in nearly 20 years. Although the rates are much too low for what lies ahead, Treasury rates are at least moving in the right direction. Albeit much too slowly, as bond investors will soon realize.

Gold is, however, moving in the wrong direction as compared to what the fundamentals ought to dictate. Both the structural and near-term factors point towards substantially higher gold prices. What Kool-Aid the gold traders have drunk, we will never know. But the current low prices are temporary, and the redemption is just months away. If not weeks.

We will witness much higher than $6000/oz later this year and multiples thereof in the years ahead.

About the Author

Shanmuganathan N (aka Shan) is an Economist and can be contacted at sh**@***********al.com