Tomorrow’s 2:00 PM statement and 2:30 PM presser will be about the dot plot. The H.4.1 release Thursday at 4:30 PM ET is where the policy actually lives.

By the DollarCollapse Editorial Team

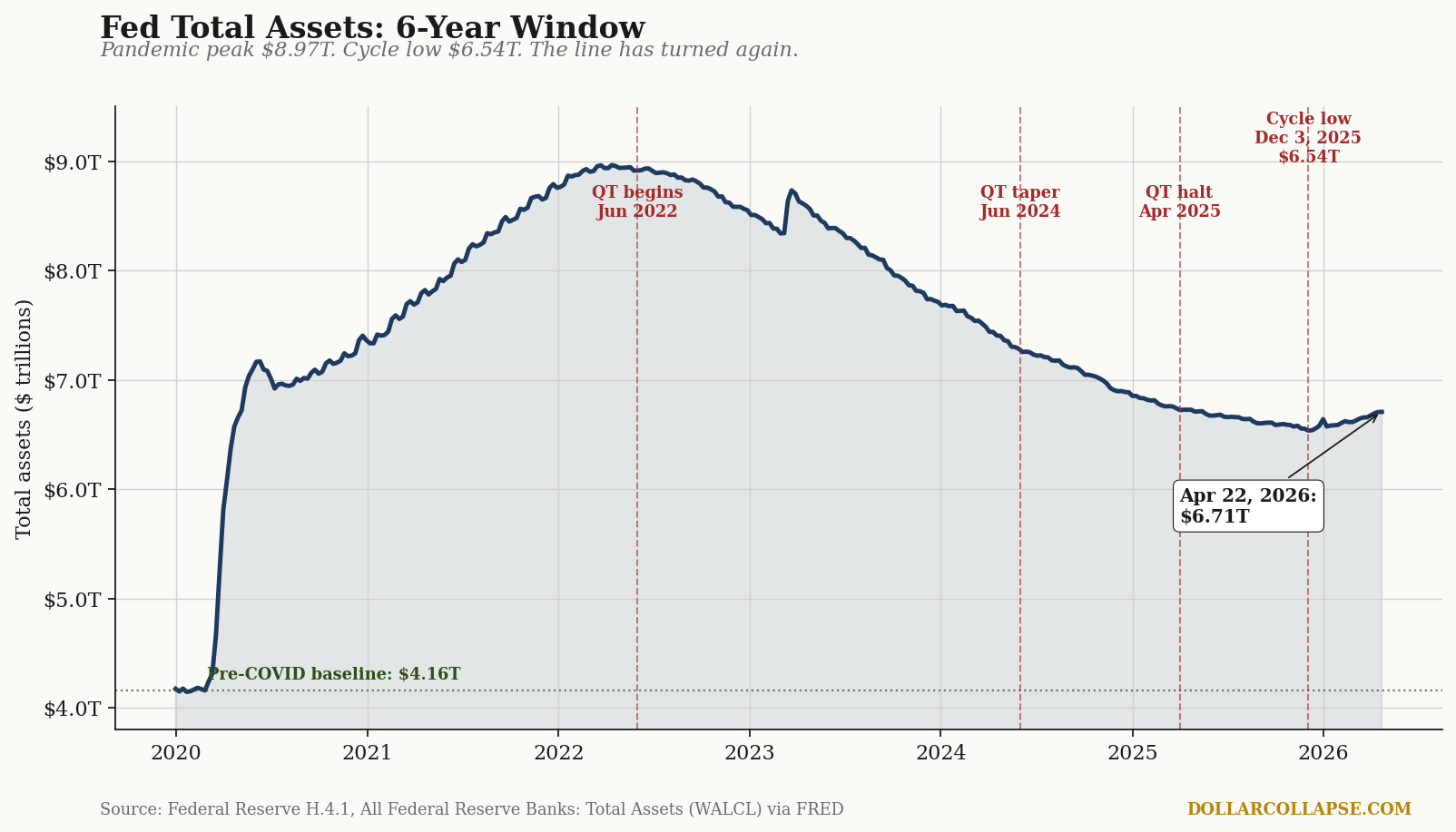

The April 28-29 FOMC meeting begins this afternoon. Markets are positioned for a 25 basis point cut tomorrow, and the rate decision will dominate the headlines through Wednesday evening. The headlines will miss the policy. The Federal Reserve’s balance sheet (WALCL on FRED) bottomed at $6.536 trillion on December 3, 2025, and has since climbed to $6.707 trillion as of the H.4.1 release dated April 22. That is a $172 billion increase over twenty weeks, in the middle of what the Fed described as a halt to quantitative tightening, with no announcement, no press conference, and no rate-policy framing. The next H.4.1 lands Thursday at 4:30 PM ET. The story is in that release, not the one tomorrow.

The 6-year tape. WALCL spiked from $4.16 trillion in February 2020 to $8.97 trillion at the April 2022 pandemic peak, an increase of $4.81 trillion in 26 months and the most aggressive monetary expansion in Federal Reserve history. The QT process announced in May 2022 ran the balance sheet down by approximately $2.43 trillion over thirty-three months, capped by the QT taper of June 2024 and the effective halt announced March 2025. The dotted green line at $4.16 trillion shows the pre-COVID baseline. The current $6.71 trillion reading is $2.55 trillion above that baseline, or 61% larger than the Fed’s pre-pandemic balance sheet, six years and three QT cycles after the initial expansion. The line has now turned upward again. Most coverage of tomorrow’s meeting will not mention this chart.

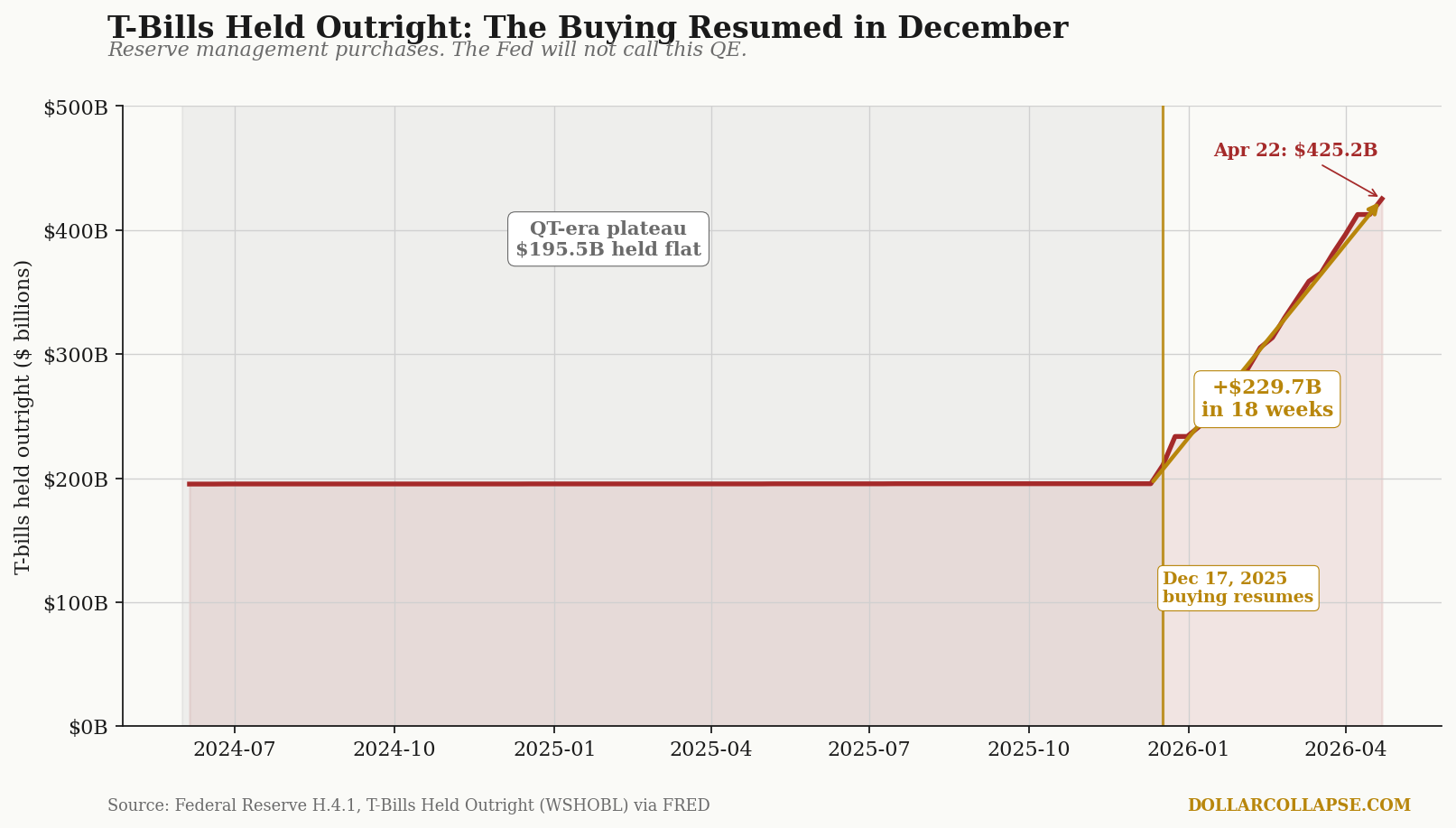

The composition of that turn is the giveaway. The Fed reports its Treasury holdings on the H.4.1 broken into bills (short-dated, under one year) and notes and bonds (longer-dated). T-bill holdings (WSHOBL on FRED) are the cleanest read on what the Fed is actively buying, because T-bills mature quickly, and a flat or rising T-bill line means the Fed is replacing what matures plus more.

This is the chart that does not appear in the FOMC statement. From late July 2025 through early December, T-bill holdings sat exactly at $195.5 billion for nineteen consecutive H.4.1 releases. That is the QT-era runoff plateau. On December 17, 2025, T-bill holdings began rising. By the April 22 release, they had reached $425.2 billion. That is a $229.7 billion increase in T-bill holdings over eighteen weeks, which is more than the entire $172 billion increase in WALCL over the same window. The implication is straightforward: the Fed is buying T-bills faster than the rest of the balance sheet is running off. The framing the Fed has used to describe these purchases is “reserve management.” The structural function is the absorption of Treasury issuance using freshly created reserves. There is a technical distinction between this operation and the formal QE programs of 2008 to 2014 and 2020 to 2022, and it is real, but it is also small. Increasing the Fed’s holdings of US Treasury securities by buying them with reserves it created is what QE has always meant. The label is the only thing that has changed.

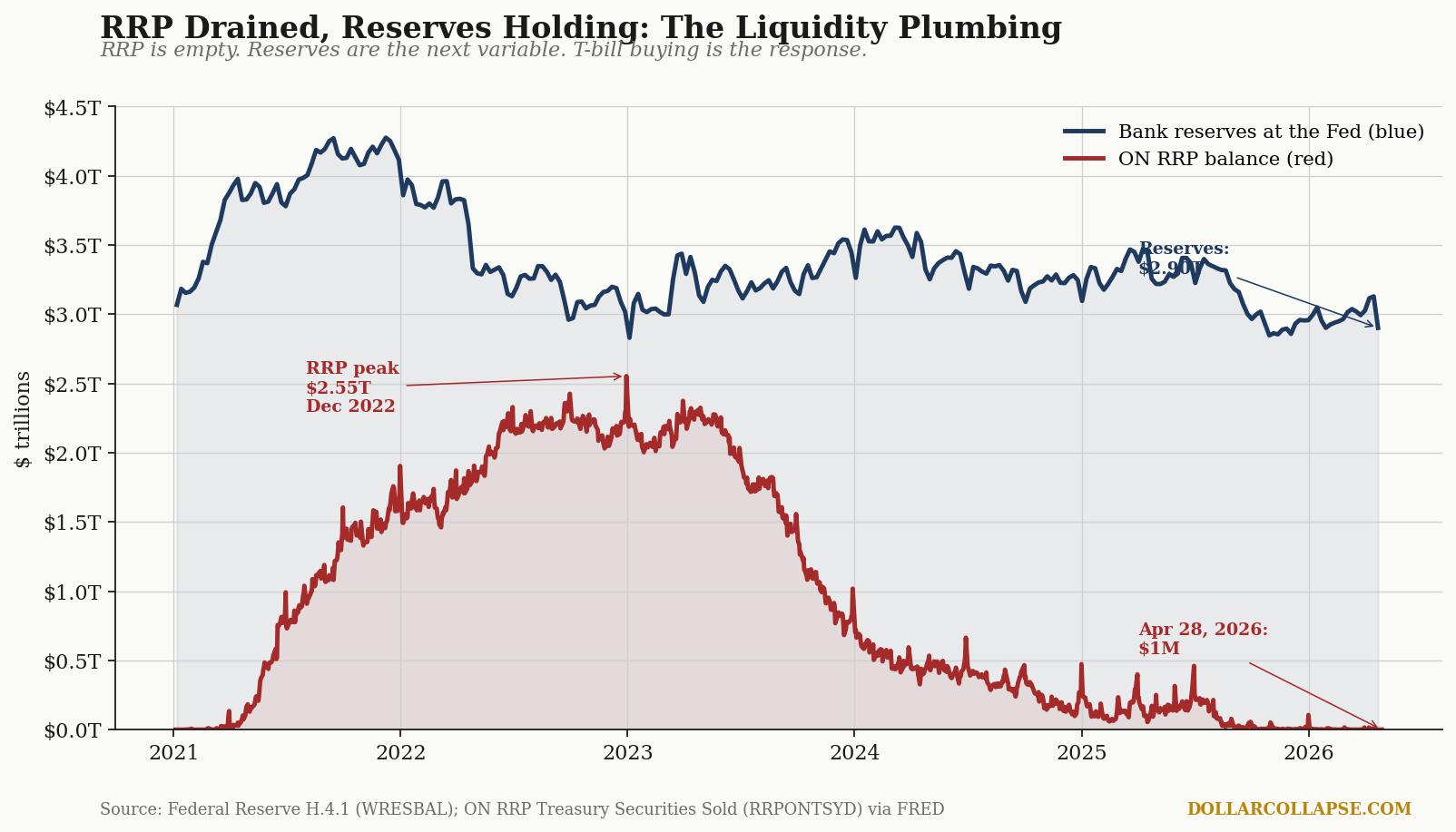

The other half of the same story: the RRP is empty. From its December 2022 peak of $2.55 trillion, the Federal Reserve’s overnight reverse repo facility (RRPONTSYD on FRED) has drained to $643 million as of the April 28 reading. That is a 99.97% drawdown. Over the same period, bank reserves at the Fed (WRESBAL) drifted lower from a 2021 peak of $4.28 trillion to the current $2.90 trillion.

The plumbing matters because of what it triggers. The RRP was the buffer the Fed used to absorb excess money market liquidity during QT. With the RRP drained, the next variable to absorb Treasury issuance is bank reserves. The Fed has historically defined “ample reserves” as somewhere in the $2.7 to $3.0 trillion range. Reserves are now at the lower end of that band. If reserves continue to drift, the Fed faces a 2019-style repo market dislocation, which is what the September 2019 emergency T-bill purchases were designed to prevent and what they are designed to prevent now. The official framing then was “not QE.” The official framing now is “reserve management.” The instrument is the same: Treasury bills, purchased at scale, with newly created bank reserves.

This is the structural mechanism that makes the rate decision tomorrow second-order. A 25 basis point cut is monetary easing of one type. A $230 billion Fed bid for short-dated Treasury paper, sustained over eighteen weeks, is monetary easing of a different type. The first is conversation. The second is the policy.

The political constraint matters. The federal government rolled approximately $9 trillion in maturing debt in fiscal 2025 and will roll a similar amount in fiscal 2026. Treasury issuance at the front end of the curve has expanded to accommodate the rollover, and someone has to hold that paper at yields the Treasury can afford to pay. With the RRP drained, the marginal buyer is either the banking system or the Federal Reserve. The Fed has answered that question for the eighteen most recent weeks of H.4.1 releases by stepping in.

The rate cut tomorrow, if it comes, is the conversation. The balance sheet is the policy. We will be charting the H.4.1 on Thursday at 4:30 PM ET.