Written by Bryan Lutz, Editor at Dollarcollapse.com:

Japan got there first.

Decades of deficits…

Near-zero rates….

And a central bank that bought so much of its own government’s debt that it wound up owning roughly half the market.

But, for our purposes, Tokyo shows where the rest of the developed world goes next…

For years the story was that Japan had broken the rules and gotten away with it. Mountains of debt, no inflation, no crisis. It has been every Keynesian economist’s dream – the free “printing press” lunch they swore existed.

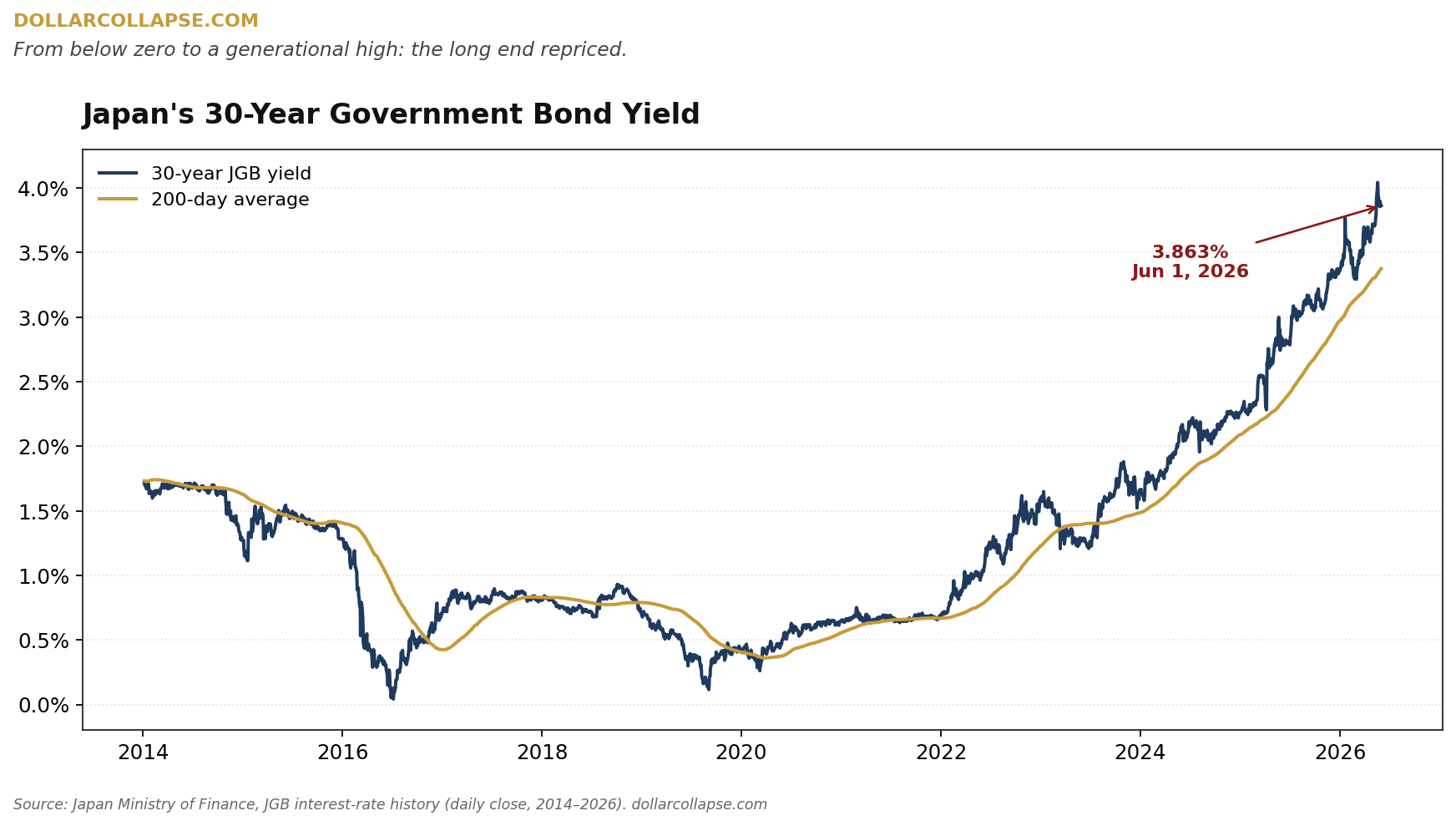

That story is over. The overall trend for Japan’s government bond yield is… Up.

Here’s the 30-year Japanese government bond yield going back to 2014:

The number on the right is 3.863%, the close on June 1. Head back six years, in June 2020 it was barely above zero. Two yers

Now, this week the same market threw a head-fake.

Reuters, reporting Tuesday:

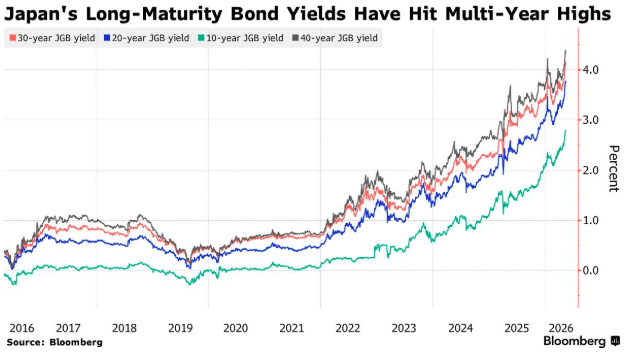

Japan’s 10-year yield dropped 11 basis points to 2.57%, its lowest since May 13, after a strong auction pulled buyers into the new debt.

Bloomberg flagged demand at the June sale as firmer than its trailing 12-month average.

So the bears took a day off…

But step back from the candle, zoom out, and look at the chart again…

From a Dow Theory perspective, the trend shows the Japan’s government bond yields are going parabolic.

Here’s what Dow Theory says…

A market moves in two ways at once:

- The primary tide

- The secondary wave, and the daily ripple.

The primary tide is the one that matters. A trend holds until price carves a lower high and a lower low and confirms the reversal. Until that happens, one good auction is just a ripple.

Look at the 30-year again. Higher highs. Higher lows. Price rides above its 200-day average the entire climb.

By Dow’s own test, the primary trend in Japanese long yields points up, and a single strong 10-year auction doesn’t change it.

The tide is still coming in.

Here’s why it keeps coming in, and why a few good auctions can’t turn it around.

Japan owes more than anyone in the developed world. The IMF puts its gross debt north of 230% of GDP. And servicing that load gets expensive in a hurry.

CNBC reported that debt-service costs in the fiscal 2026 budget jumped 10.8% to 31.3 trillion yen, with the government’s own math assuming a 3% interest rate, the highest assumption in 29 years.

For example, this spring, after she ruled out extra spending, the prime minister reversed course and called for a 3 trillion yen ($19 billion) supplementary budget for household costs.

Here’s the trap.

Higher yields raise the interest bill. The bigger bill widens the deficit. The wider deficit demands more bonds. And more bonds, as the Bank of Japan steps back from the market, mean higher yields…

Last summer the Ministry of Finance hit that wall head-on. It had to redraw its issuance plans because the market wouldn’t swallow 20-, 30-, and 40-year paper at the price the government wanted to pay, so it shoved the borrowing into short-term bills instead, which is really a borrower hiding from its lender.

Now pull the lens back.

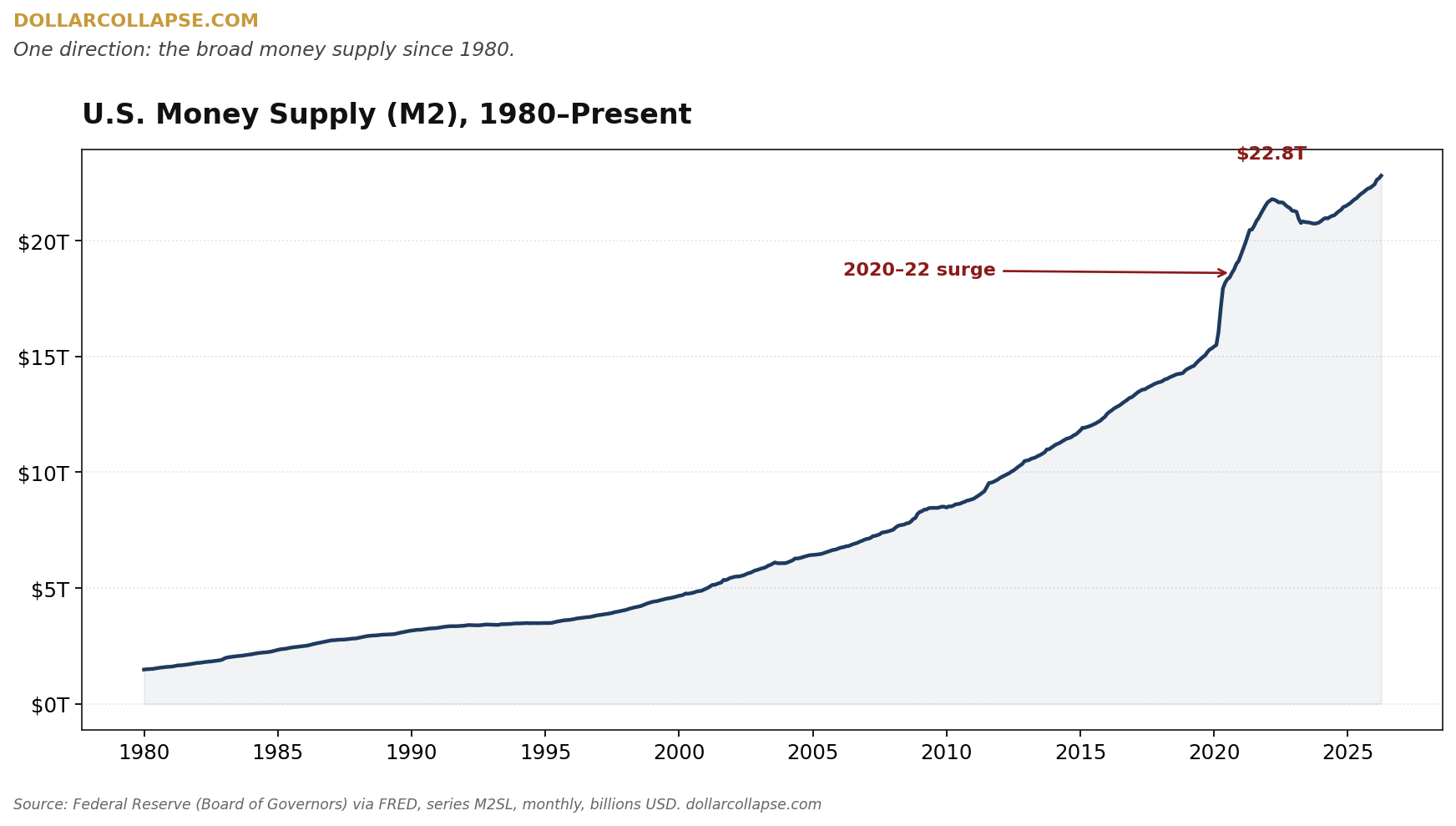

Here’s US M2, the broad money supply, since 1980:

The 2020 spike has never come down.

The dollar is the world’s reserve currency, so this line sets the pace for everyone else. When the country that prints the reserve currency runs its presses, every other country faces the same choice: match the pace, or watch its own currency climb against the dollar.

A rising currency sounds like a prize, but for an export economy(like Japan) carrying the heaviest debt on earth it’s a punishment:

A brief discount on imports, then crushed exporters, falling prices, and a heavier real debt load for years. Tokyo has spent a decade making sure that doesn’t happen.

So as the dollar supply grows, the yen supply will grow to meet it.

Nations, Japan and others have been devaluing their currency against the USD on purpose. Each one races to cheapen its money faster than the next, because the cheaper currency exports more and inflates away more of its debt. And because the USD’s M2 Supply keeps expanding the track only runs downhill.

Japan’s been in the currency fight for years, with the weakest major currency and the biggest debt to inflate away. Its rising yield just shows where the front line sits now. The more the bond market demands, the more the Bank of Japan has to print to hold the line, and the more it prints, the lower the yen goes.

So watch Tokyo. It reached this point a decade ahead of everyone else, and it runs the play the rest of us get next:

A government that can’t fund itself at market rates, a central bank that prints the difference, and a currency that pays the bill.

A strong auction here and there buys time. It doesn’t buy an exit. The debt is too big, and the arithmetic too plain.

Welcome to the Land of the Rising Yield. Watch it rise.