Guest Post by Mish Shedlock, blogger at MishTalk:

New mortgage rules are so absurd that only President Biden or other Progressive-minded economic illiterates could possibly have come up with them.

Subsidizing High-Risk Homebuyers

Please note that not only will banks offer Subsidies to High-Risk Homebuyers, it will be at the expense of those with better credit scores.

Fannie Mae and Freddie Mac will enact changes to fees known as loan-level price adjustments (LLPAs) on May 1 that will affect mortgages originating at private banks nationwide, from Wells Fargo to JPMorgan Chase, effectively tweaking interest rates paid by the vast majority of homebuyers.

The result, according to industry pros: pricier monthly mortgage payments for most homebuyers — an ugly surprise for those who worked for years to build their credit, only to face higher costs than they expected as part of a housing affordability push by the US Federal Housing Finance Agency.

“It’s unprecedented,” added David Stevens, who served as Federal Housing Administration commissioner during the Obama administration. “My email is full from mortgage companies and CEOs [telling] me how unbelievably shocked they are by this move.”

Under the new rules, high-credit buyers with scores ranging from 680 to above 780 will see a spike in their mortgage costs – with applicants who place 15% to 20% down payment experiencing the biggest increase in fees.

Under the revised LLPA pricing structure, a home buyer with a 740 FICO credit score and a 15% to 20% down payment will face a 1% surcharge – an increase of 0.750% compared to the old fee of just 0.250%.

When absorbed into a long-term mortgage rate, the increase is the equivalent of slightly less than a quarter percentage point in mortgage rate. On a $400,000 loan with a 6% mortgage rate, that buyer could expect their monthly payment to rise by about $40, according to calculations by Stevens.

Meanwhile, buyers with credit scores of 679 or lower will have their fees slashed, resulting in more favorable mortgage rates. For example, a buyer with a 620 FICO credit score with a down payment of 5% or less gets a 1.75% fee discount – a decrease from the old fee rate of 3.50% for that bracket.

Reverse Pricing

This reverse pricing of mortgage rates is so insane that I am at a loss for additional words.

Median Home Prices Sink 3% in March, the Biggest Yearly Drop Since 2012

On a housing-related note, Median Home Prices Sink 3% in March, the Biggest Yearly Drop Since 2012

Home Prices Are Falling Everywhere, But Not as Fast as They Rose

On April 1, I commented Home Prices Are Falling Everywhere, But Not as Fast as They Rose

Median Price vs Repeat Sales

- Median price is timely but highly inaccurate.

- Measures or repeat sales of the same home as per Case-Shiller methodology are accurate but severely lagging on the way up and down.

See the above articles for discussion.

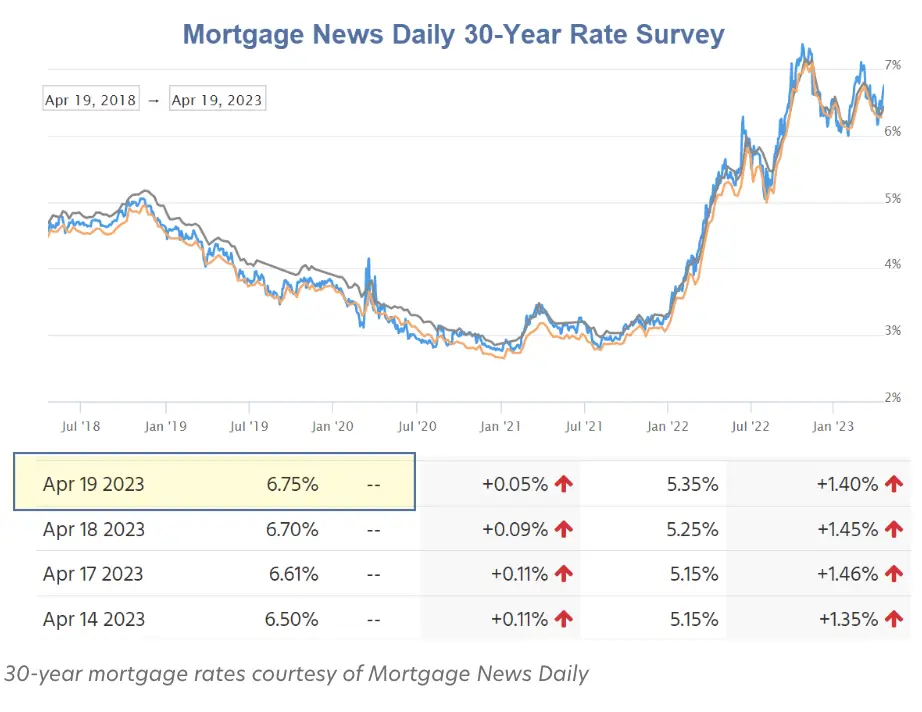

Meanwhile, please note the best rate for those with high credit scores will jump from 6.75 percent to 7.0 percent.