Written by Bryan Lutz, Editor at Dollarcollapse.com:

The Fed spent the past year cutting rates while the bond market spent the past three months raising them.

Let’s break that down:

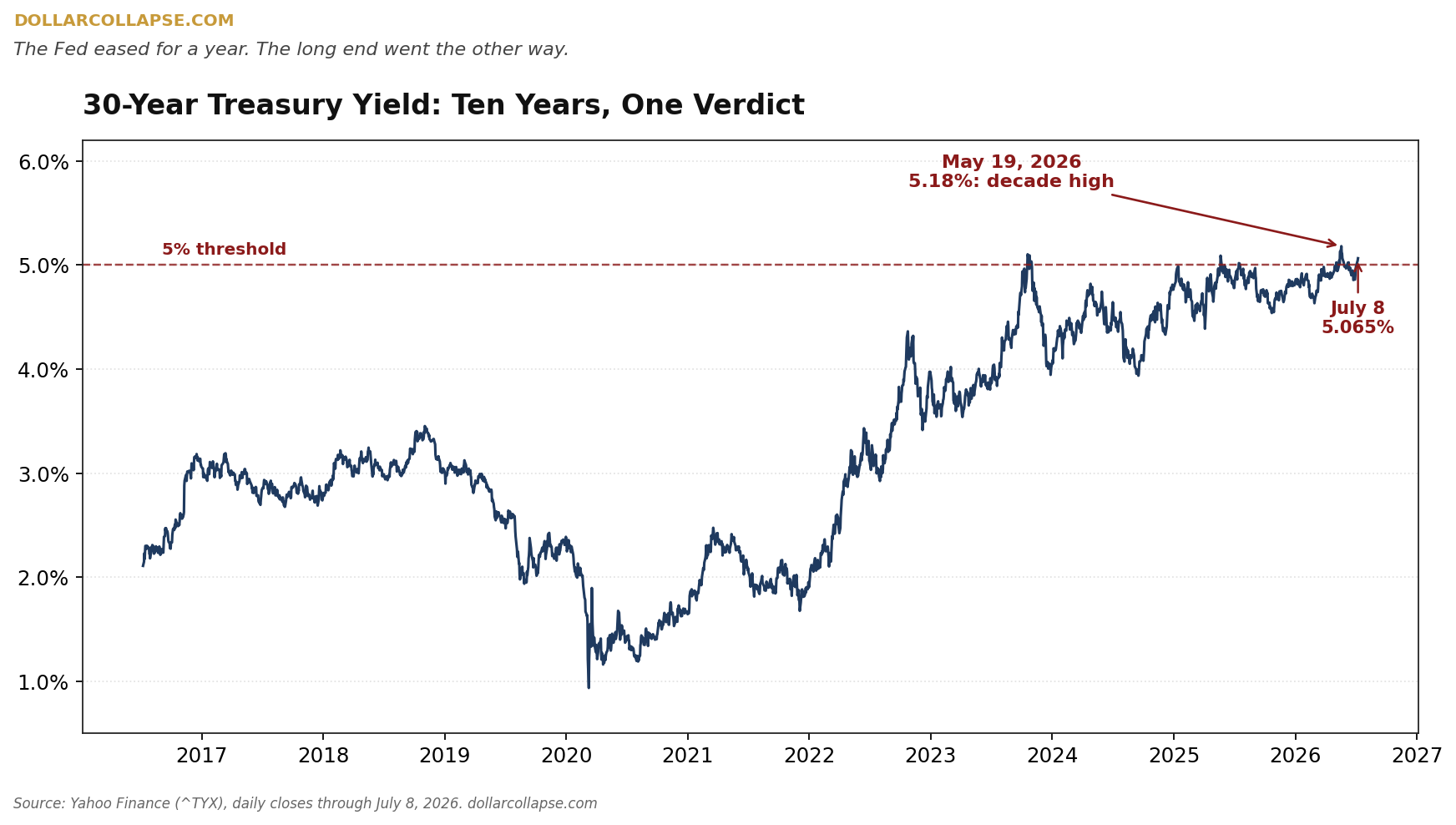

Fed funds sits at 3.63%, a 52-week low. The 30-Year Treasury yield touched 5.2% in May, its highest level in a decade, and closed back above the 5% line this week above 5.065%.

One rate is set by a committee in Washington. The other is set by people with their own money at risk…

Guess which one?

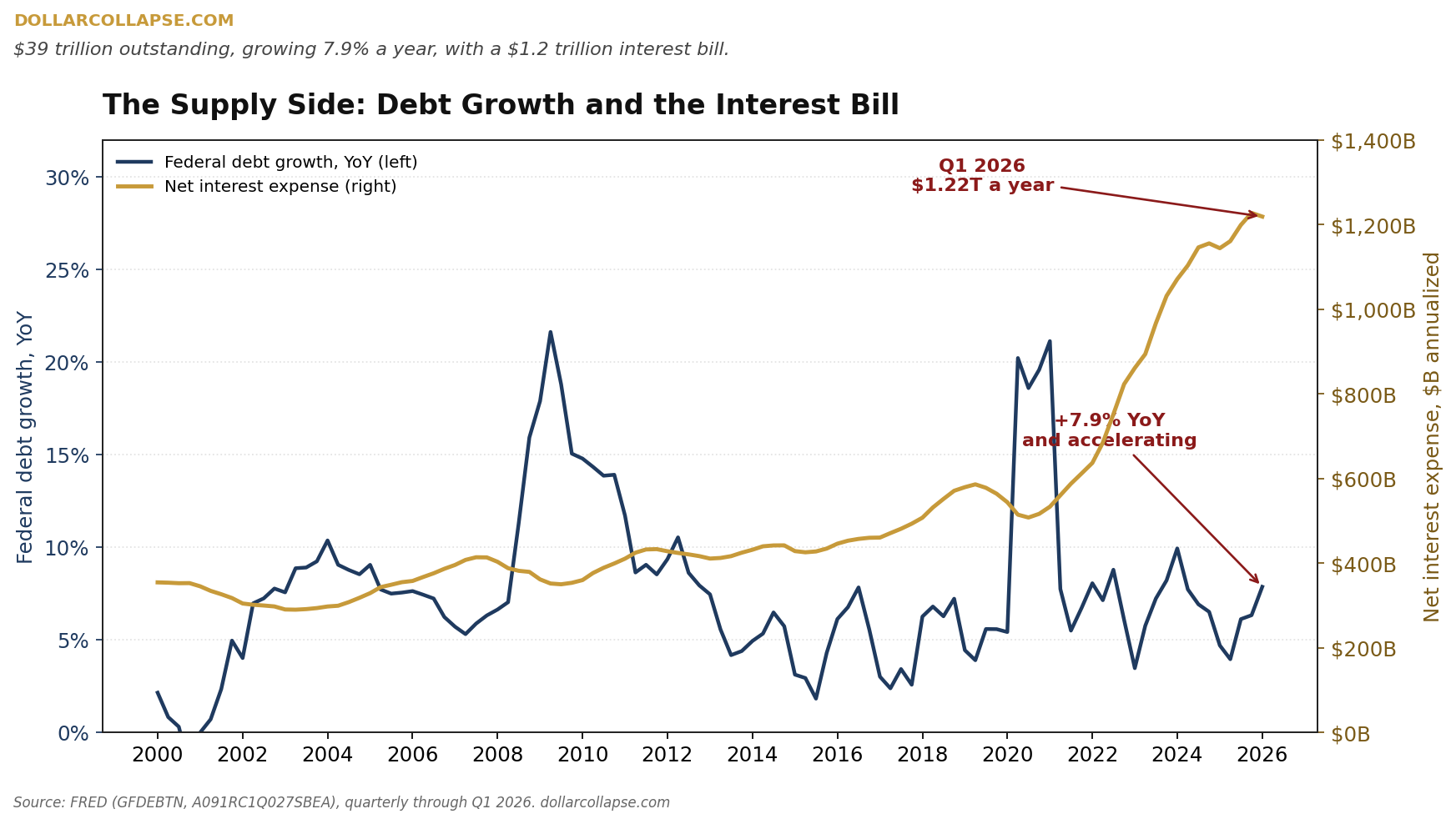

You can find the right answer by how fast the US debt is rising. Federal debt stands at $39.07 trillion and grows 7.9% a year. US debt was growing 6.3% a year, but over the last three months, the growth rate itself has accelerated 24%. And net interest on that debt now costs the Treasury $1.22 trillion a year. Supply is expanding fast, and buyers are setting the price.

That’s the result of the Fed easing for a year.

Here’s the long end’s (US 30Y Treasury yield) response:

A 5.18% close on May 19, the highest in a decade. Back above 5% this week.

The short end tells the same story. The 2-Year yield hit 4.13% this month, a 52-week high, while Fed funds sits at a 52-week low. The spread between them has collapsed 31% in three months, to 0.36. So, the market is ignoring the Fed on both ends of the curve.

At 2:00 PM today the Fed released the minutes of its June 16-17 meeting, the one where it held rates at 3-1/2 to 3-3/4 percent. The committee that cut its way to a 52-week low has stopped cutting. A few members want to go the other way:

FOMC Minutes, June 16-17, 2026:

“A few participants commented that, in light of these developments, there was a case for raising the target range for the federal funds rate, but those participants indicated that they supported maintaining the current target range at this meeting.”

The easing bias is gone too:

“Members also agreed that the statement would not repeat the language that had suggested an easing bias regarding the likely direction of the Committee’s future interest rate decisions.”

Buried deeper is the most honest sentence in the document. The manager of the Fed’s trading desk told the committee that:

“the ownership composition of Treasury securities has shifted somewhat over the past several years from relatively price-insensitive official-sector holders to more price-sensitive private investors, which could have implications for the term premium component of yields.”

Here’s what that means:

$39 trillion in debt, growing 7.9% a year, with a $1.2 trillion interest bill.

The June inflation report arrives July 14. The May number was already 4.27%, the highest in a year, and the Fed’s own minutes admit inflation is “elevated” and still climbing. So, many investors are betting the next move is a rate hike, not a cut.

Watch what happens if the Fed does nothing while inflation runs above 4% and the 30-Year Treasury pays above 5%. That would tell you the Fed has stopped fighting inflation and started protecting the government’s borrowing costs. That’s what you call fiscal dominance.

One important asset has figured this out early. Gold pays no interest and answers to no government. Yet, it’s up 22% over the past year even after a 14% drop this spring.

Keep it in perspective. This is one more data point, not a tipping point. Governments don’t default overnight, and world reserve currencies don’t collapse, they lose value a little at a time.

But something has to measure the plumbline…

This month, the judge is the 30-Year Treasury Yield.