Guest post from Shanmuganathan N. author of

The US Federal Reserve will most certainly cut the Fed Funds Rate on September 18th, probably by 50bps. The gold prices will also go higher as has been explained by analysts on various business channels. The rationale as stated by “experts” is that the Fed lowering the rates reduces the incentive to hold onto US Dollars and hence makes Gold more attractive. Sounds reasonable.

So are these two events – Fed cutting rates and Gold prices going up – correlated as explained above? Not at all. These analysts couldn’t be more wrong if they tried. Read on.

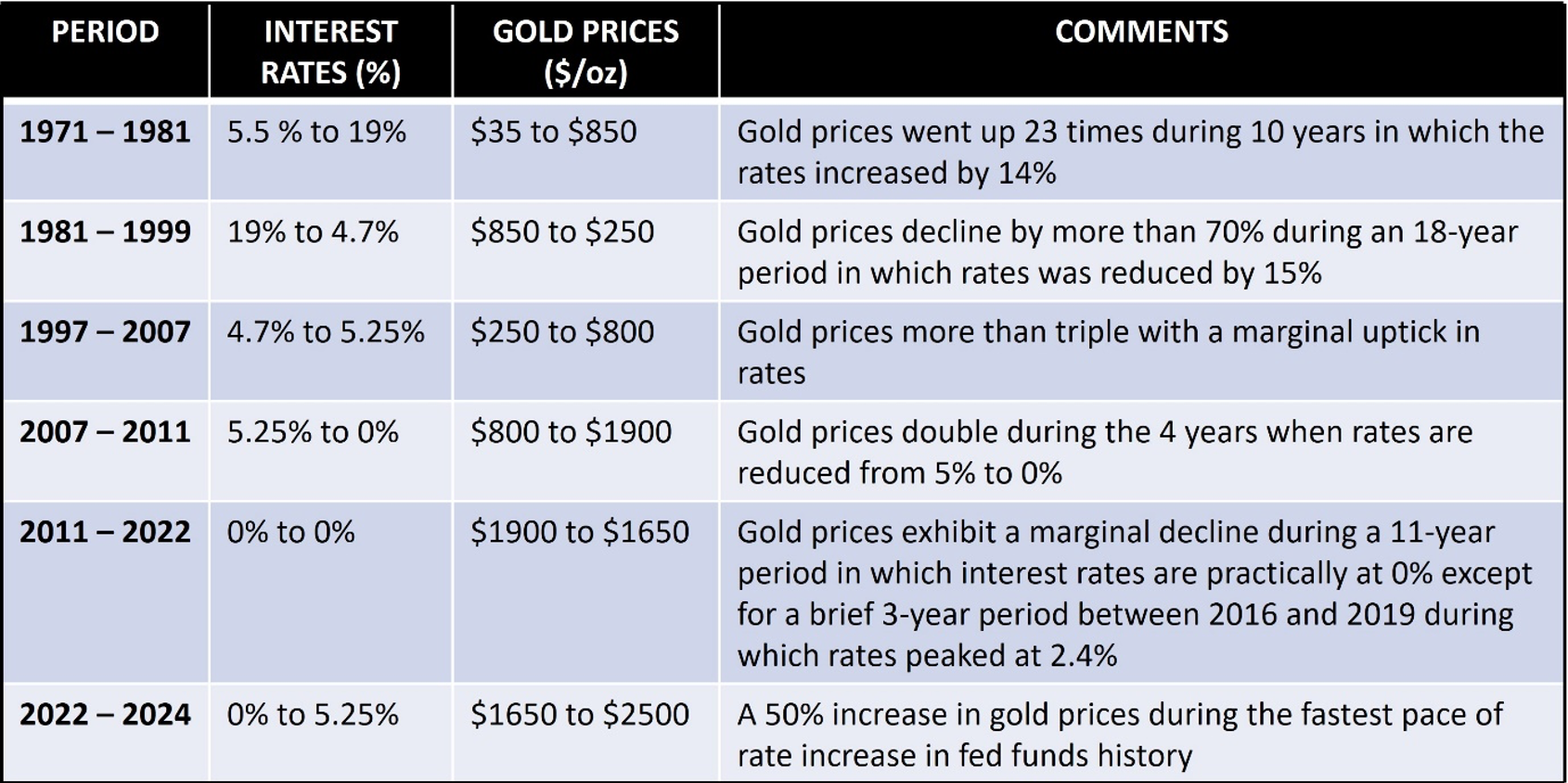

Historical Movements in Interest Rate and Gold Prices

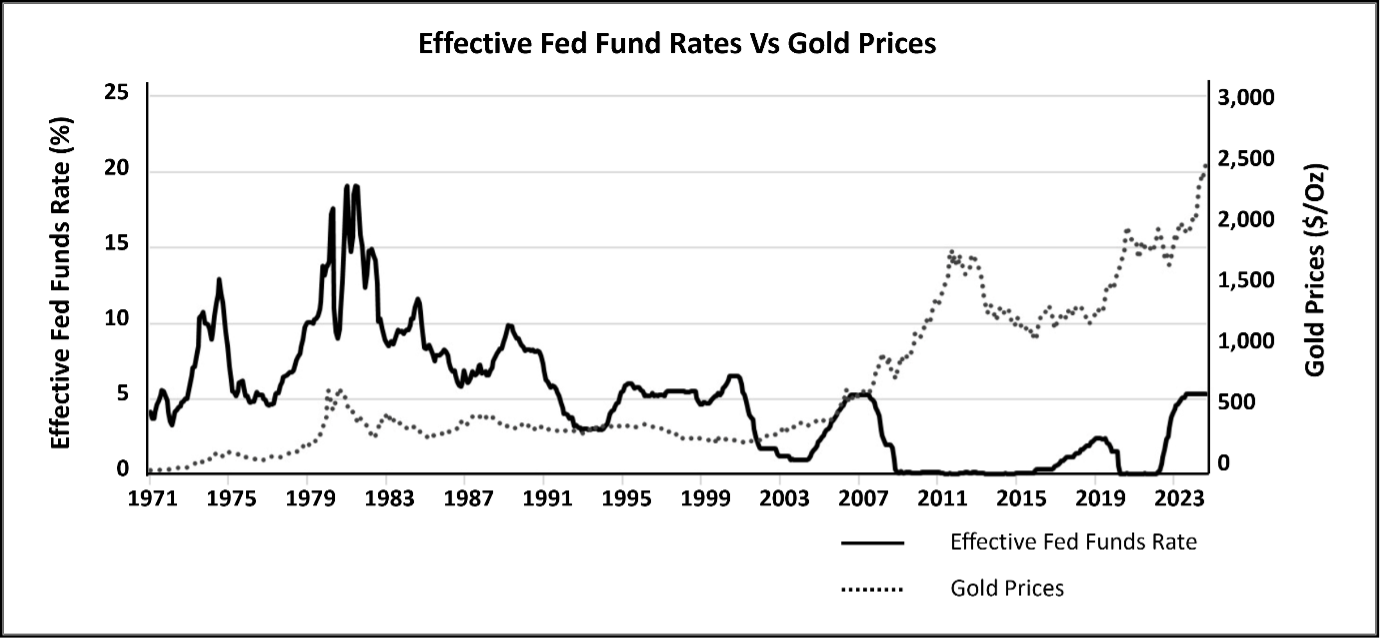

The above table should put to rest the theory stated in the opening paragraph. Excepting for a brief 4-year period between 2007 and 2011, what one can conclude from the above table is that interest rates and gold prices are positively correlated. i.e. an increase in interest rates, causes the gold prices also to increase and a decrease in interest rates causes the gold prices to decline as well. These are very secular trends lasting 10 years or longer as could be inferred from the table. The same is shown in the figure below.

What the media has been conveying through the decades i.e the inverse correlation between the Fed funds rate and gold prices is incorrect. For the last 45 years, there has been a positive correlation except for the 4 years between 2007 and 2011.

What then drives Gold Prices?

That ofcourse is a billion-dollar question. As I have explained in my book RIP U$D: 1971-202X …and the Way Forward, two factors are the primary drivers i.e. The Cantillon Effects and the Real Interest Rates (i.e. price inflation-adjusted interest rates). The nominal interest rates are irrelevant. For example, Paul Volcker had to offer an 8% real yield (the Fed Funds rate was 20 – 22%+ when the price inflation was around 13-14%) during the early 1980’s to stop the upward trajectory of gold prices.

So what is the rate that the Fed has to offer to stop the gold price movement this time around? Even assuming that a 5% real yield will do this time, the Fed funds rate would have to be close to 15%. That is because the US Government is underreporting on the price inflation through a series of changes which started in the mid-1980’s that deliberately understates price inflation.

Shadow Government Statistics measures “Price Inflation” using the same metrics that the US Government used during that 1970’s and that reflects a double-digit price inflation in the US today and possibly even worse than what was experienced during the 1970’s as shown. So, we need substantially higher interest rates, i.e. atleast 15%, compared to what is prevailing today to prevent raising gold prices.

That ofcourse is an impossibility. Even at a net rate of slightly higher than 3%, the US Federal Government finances are on the verge of bankruptcy due to the interest outgo on the National Debt. At a 15% rate on the National Debt, 100% of the Federal revenues would have to go towards servicing the interest alone. That is even assuming that the Federal Revenues do not collapse due to the higher interest rates and the National Debt does not go up substantially higher.

The Fed is thus in a desperate situation to save the Federal Government from becoming an explicit defaulter. They also need to be seen to save the collapsing job market. So a series of rate cuts are a given at this juncture. The casualty of this monetary policy is going to be the US Dollar and that is going to reflect in substantially higher gold prices. The tailwinds of monetary inflation of the last 2 decades are so strong that gold prices will go up even if the Fed hikes rates. We have seen that for the last 2 years where the Fed hiked the rates to 5% and gold prices went up 50%.

So the media is right about rate cuts ahead and the ensuing higher gold prices. But for entirely the wrong reasons.

What Lies Ahead?

Looking a few years ahead, we are going to have substantially higher gold prices i.e. atleast a 10-fold move from the current price of $2500/oz. This is going to be accompanied by much higher interest rates though these rates are going to lag the price inflation numbers. Additionally, this number of $24,000/oz as I have explained in the book is the floor and not the ceiling to gold prices. Fiscally and monetarily speaking, there is no reason why the bull market ahead in Gold prices should not rival what happened during the 1970’s.

About the Author

Shanmuganathan. N is an Economist and author of the book “RIP USD:1971-202X …and the Way Forward”. He can be contacted at sh**@***********al.com