Written by Bryan Lutz, Editor at Dollarcollapse.com:

For seventy years, the rule was simple.

Central banks bought gold. They didn’t buy silver…

Silver was the metal you mined and shipped. Gold was the metal you stored and counted.

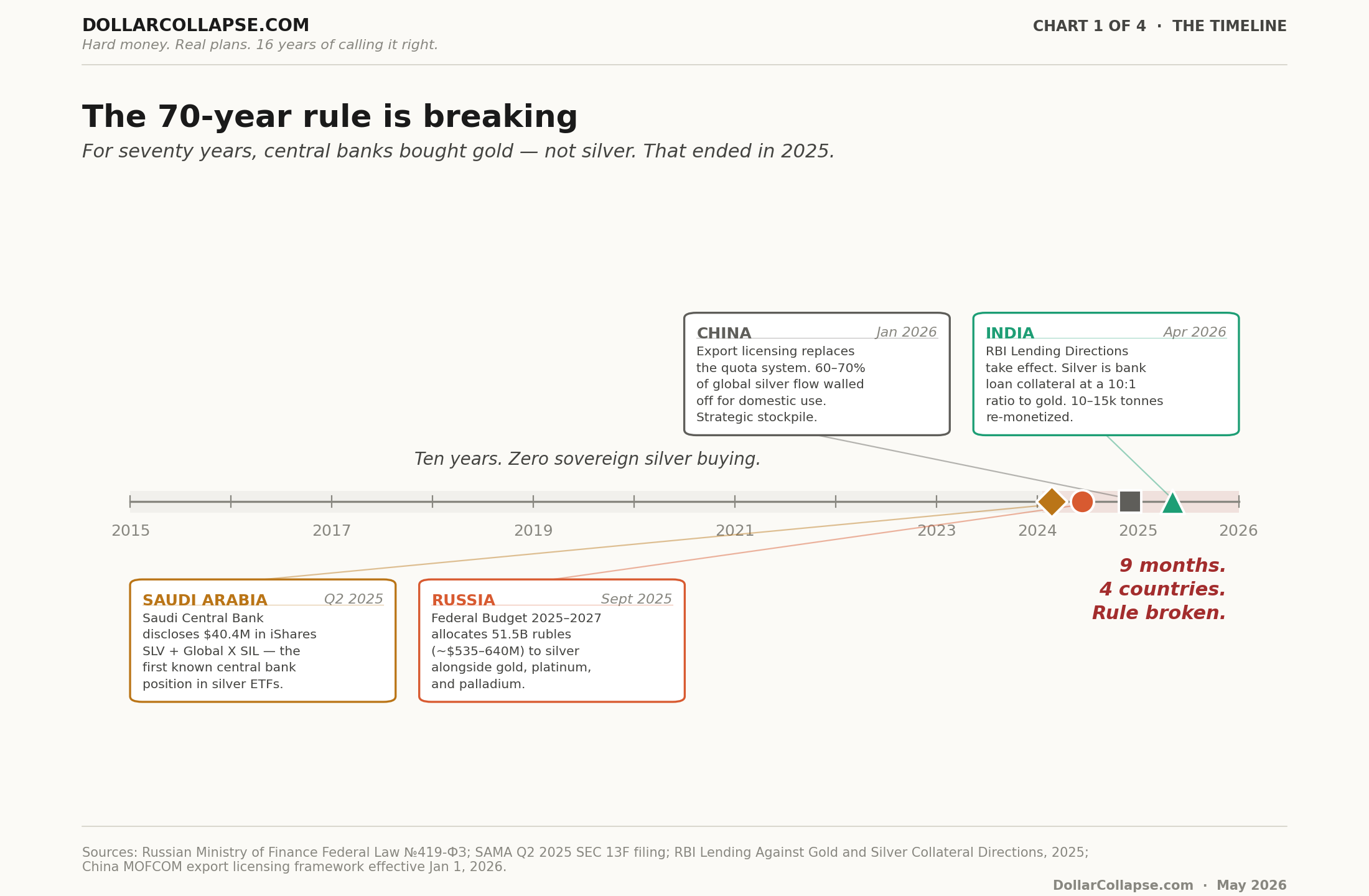

Then in nine months, four sovereign players broke that rule four different ways.

And almost nobody is connecting the dots.

So let’s connect them.

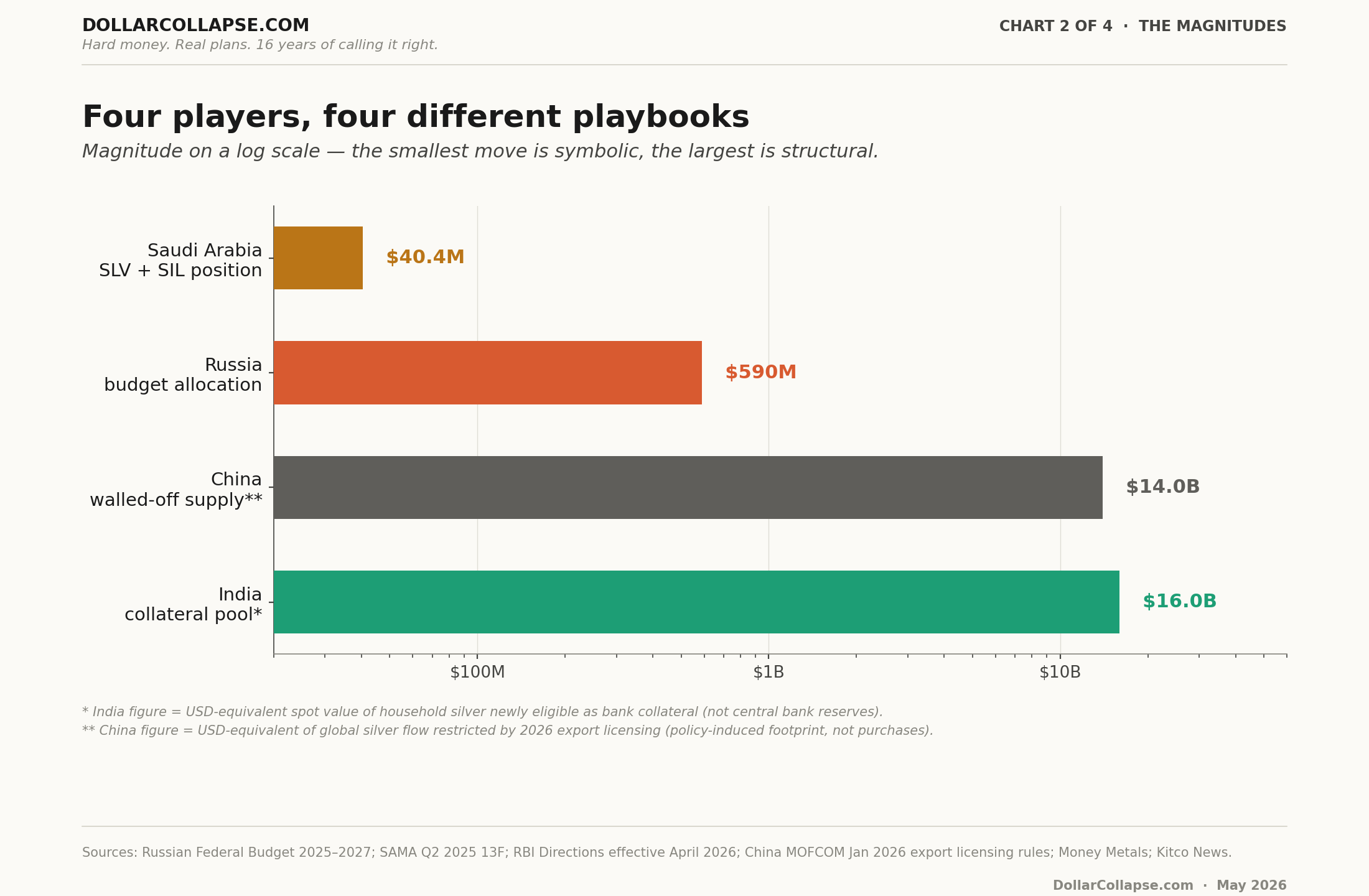

Saudi Arabia, Q2 2025

The Saudi Central Bank (SAMA) filed a 13F with the SEC disclosing 932,000 shares of iShares Silver Trust (SLV) and 203,700 shares of Global X Silver Miners (SIL) totalling $40.4 million.

This was the first publicly disclosed central bank position in silver-linked ETFs. A Gulf central bank parked reserves in a Wall Street silver fund alongside its energy ETF holdings, and a sentence that would have been unthinkable five years ago became a footnote in a quarterly filing.

Russia, September 2025

Russia’s Federal Budget for 2025 to 2027 allocated roughly 51.5 billion rubles, somewhere between $535 million and $640 million depending on FX, for precious metals purchases by Gokhran, the State Fund of Precious Metals.

It’s the first budget cycle in modern Russian history that names silver explicitly. Right alongside gold, platinum, and palladium.

Kitco News reports:

Russia’s central bank may be boosting silver prices through undeclared purchases

“Hints of a major new buyer, Russia’s central bank, starting to influence the silver price, which has risen to a 14-year high. Silver outperformed gold immediately after the budget allocation was announced at the end of September, and ETF inflows in the first half of 2025 alone eclipsed all of 2024.”

China, January 2026

China didn’t announce a silver reserve. China replaced its export quota system with a licensing framework.

To export silver from China starting in January 2026, you need to produce 80 tonnes annually and secure $30 million in credit lines. The numbers are designed to disqualify almost everyone.

Net effect: 60 to 70 percent of global silver flow now stays inside Chinese borders.

This is the rare-earths playbook applied to silver. Beijing doesn’t need to hold the metal in a vault if it controls the gate.

Alasdair Macleod has tracked this from a different angle, arguing the West has been net-importing Chinese silver for years and that the pipe just got shut off. On his read, the supply deficit is now in its eighth consecutive year, not the Silver Institute’s official five.

Either way, it’s a stockpile.

India, April 2026

The Reserve Bank of India’s Lending Against Gold and Silver Collateral Directions, 2025 took effect in April. Silver ornaments and coins are now formal bank loan collateral at every commercial bank and NBFC in the country.

The cap: 10 kilograms of silver per borrower. Versus 1 kilogram of gold. The 10-to-1 ratio is now built into Indian banking law.

It’s the implicit monetary parity of silver to gold, written into the lending framework of the world’s largest silver-importing nation.

The rule pulls an estimated 10,000 to 15,000 tonnes of household silver, the kind sitting in temple vaults and family safes across India, into the formal banking system as money-good collateral. No central bank silver purchase in modern history has touched that magnitude.

Essentially, India is telling its banks silver is gold’s monetary cousin…

The timeline

Here’s the timeline. Ten years of nothing, then four sovereign moves in nine months.

There was a flat decade, then a step-change. The rule broke.

Four playbooks, not one

The newswire treats these as a list of similar headlines, but they aren’t.

Saudi’s $40 million is a symbolic signal.

Russia’s $590 million budget allocation is open and named in policy.

China’s 60 to 70 percent supply control is operational, not a reserve.

And India’s 10,000 to 15,000 tonne household pool is structural. It’s the largest by an order of magnitude, and it’s the one nobody’s talking about.

You can see in the chart below what changes when you put the four moves on the same scale.

Why now

Three forces broke the rule simultaneously.

Gold got too expensive per unit. With gold near $5,000 an ounce, a single one-ounce coin is friction-heavy as a settlement instrument. Silver around $80 is closer to a working monetary unit.

Industrial demand turned silver structural. The Silver Institute has logged five consecutive years of supply deficit through 2024, with industrial demand at a record 680.5 million ounces. Solar, EVs, and AI compute have given silver the demand profile of a strategic metal, not a precious one.

And sanctions logic. Russia, in the State’s own framing, described silver as an asset that could withstand financial coercion. The same logic is available to anyone planning for future U.S. sanctions exposure…

Which is, increasingly, everyone.

Here’s the same data, stacked.

The pattern is set

The four moves were not coordinated. Each sovereign reached the same conclusion on its own clock, for its own reasons.

The gold-and-only-gold rule held for seventy years because it didn’t need to break. Now the gold math is forcing it.

The next sovereign silver move won’t be telegraphed. It’ll show up in a 13F filing, a budget annex, or a footnote in a central bank press release. The kind of thing that takes a week for the wire to notice and a month for the analysts to admit they missed.

The pattern is set. The question is which one. And what month.

Watch the filings.

The rule won’t announce its next break.