Written by Bryan Lutz, Editor at Dollarcollapse.com:

Here are two facts that seem to contradict each other:

Fact one:

According to the IMF’s latest data, the US dollar’s share of global foreign exchange reserves just dropped to 56.8%, a 31-year low. Central banks around the world have been quietly, methodically buying other currencies and gold, letting the dollar’s relative weight shrink year after year.

Fact two:

Since the US and Israel launched a war against Iran in late February, the Dollar Index has been rising. The dollar has been one of the best-performing assets of the past several weeks. ‘King Dollar’ is back, according to at least half the financial headlines.

So which is it? Is the dollar dying or dominant?

Both. And that’s the point.

The war-driven dollar bounce is real, temporary, and ultimately irrelevant to the long-term story. It’s a blip on a multi-decade downtrend…The monetary equivalent of a dead-cat bounce. Meanwhile, the structural forces undermining the dollar’s reserve status have not paused for the war. If anything, the war is accelerating them.

Three charts prove it. Let’s walk through them.

1. The 31-Year Low

Wolf Richter at Wolf Street has been tracking this quarterly for years, and the trend line is relentless. In 2001, the dollar accounted for 71% of all global foreign exchange reserves. Today it’s 56.8%, the lowest reading since 1994. And the mechanism behind the decline is more interesting than the headline number.

Central banks haven’t been dumping US dollar assets. As of Q4 2025, foreign central banks still held $7.46 trillion in US securities, which has been roughly flat with 2014. The dollar’s share is falling not because anyone is selling, but because everyone is buying everything else faster. The total pool of global foreign exchange reserves has surged, and the incremental buying has gone disproportionately to euros, yen, pounds, Canadian and Australian dollars, Chinese renminbi… and increasingly to what the IMF calls the ‘non-traditional reserve currencies.’ That category (dozens of smaller currencies combined) has more than doubled its share since 2021, now standing at 6.1%.

Translation: the world’s central banks are building the exits while the building is still standing. They’re quietly moving their valuables to safer storage. Nobody wants to trigger a dollar collapse. But nobody wants to be caught holding too many dollars when it happens, either.

“This path is obviously not permanently sustainable. And the ‘twin deficits’ need to be brought down substantially before something goes off the rails, such as a surge of inflation and much higher bond yields.”

— Wolf Richter

Why are they doing this? Because the maths are obvious. The US runs a structural trade deficit and a structural federal budget deficit simultaneously. Both are funded, in part, by foreign central banks willing to accumulate dollar-denominated assets. As those central banks diversify, the US loses its most captive buyer for its debt. Eventually, the result is higher yields and a weaker dollar, which is coming sooner than later.

The US national debt crossed $39 trillion just two weeks into the Iran war. At this level, interest payments are becoming the single fastest-growing line item in the federal budget. This doesn’t look like it will change.

The dollar’s long decline from 71% to 56.8% happened across bull markets, bear markets, Democratic administrations, Republican administrations, and every Fed regime from Greenspan to today. This is a structural problem. In 1971, the dollar’s gold anchor was cut, and that set the trajectory for where we are today.

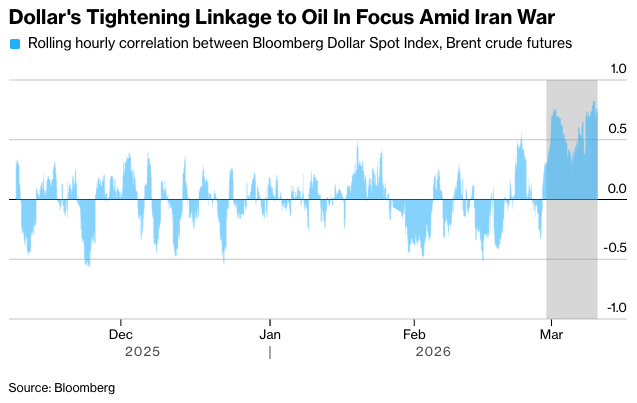

2. The War Bounce: Dollar Rises With Oil

Since the US-Israeli attack on Iran began, oil surged from the low $60s to over $100 a barrel. At one point oil touched $120 a barrell before pulling back. And the dollar has risen right alongside it. This seems counterintuitive. War, debt, inflation risk shouldn’t that be dollar-negative? So why is the dollar going up?

Because the US is now the world’s largest oil producer, and oil is still priced in dollars. When oil spikes, every oil-importing nation in the world suddenly needs more dollars to pay for it. Japan needs more dollars. Germany needs more dollars. India, South Korea, Brazil… They all need more dollars. That surge in dollar demand (call it the petrodollar mechanism) is what is temporarily propping up the currency right now. As of right now, the dollar is trading like a petrocurrency, not a reserve currency. It’s rising because oil is rising, not because the world has suddenly rediscovered faith in US fiscal management.

“It may not be obvious or intuitive why the dollar would strengthen following a U.S. attack on Iran… the dollar has benefited from the surge in crude oil prices… both WTI and Brent surged from the $60s to as high as $120.”

— Jesse Colombo, The Bubble Bubble

Here is the trap:

This war-driven dollar rally is not only temporary, it is sowing the seeds of the next phase of dollar decline. Deutsche Bank has warned that the Iran war could accelerate the emergence of a ‘petroyuan,’ as nations locked out of the Hormuz Strait or alienated by US policy look for oil-pricing alternatives to the dollar. Iran itself has been demanding oil payments in yuan. The Middle East Monitor notes that the Strait of Hormuz through which roughly 20% of globally traded oil passes daily is now contested in a way it hasn’t been since the 1980s tanker wars. Any sustained disruption will shatter the petrodollar arrangement’s most basic premise: that US security guarantees make the dollar-for-oil deal reliable.

Meanwhile, the war is running up the US national debt at a ferocious pace. Wars are inflationary. Inflationary debt spirals are dollar-negative. The war has created a short-term dollar bounce by spiking oil demand for dollars, but it has simultaneously worsened every long-term structural factor that is killing the dollar.

Both things are true. The bounce is real. The trend is also real. The bounce is measured in weeks. The trend is measured in decades. Act accordingly.

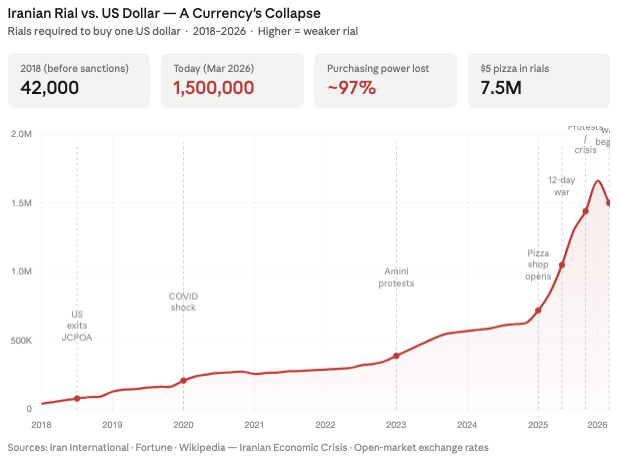

The Canary in the Coal Mine: The Iranian Rial

In April 2025, a pizza shop opened in Tehran’s upscale Niavaran neighborhood with a simple gimmick:

It priced its pies in dollars. Five dollars. At the time, this seemed like a marketing stunt, a kind of quirky hedge against inflation. Clever, even.

One year later, it looks like prophecy.

Iran is undergoing a textbook currency collapse in real time. The rial, once trading at around 42,000 to the dollar in 2018, had already fallen to 1 million rials per dollar by early 2025. By January 2026, it hit 1.66 million. As of this writing, it hovers around 1.5 million. That is a loss of roughly 97% of its value against the dollar in eight years. The Iranian government has responded by issuing ever-larger-denomination bills…

First the 5 million rial note, then the 10 million rial note ($7 at current rates).

That is the universal sign of a government that has lost control of its own money supply. The former head of the Tehran Stock Exchange warned publicly that Iran was entering ‘the stage of dollarization.’ Dollar-pegged property sales expanded from luxury apartments to mid-range homes. Street merchants began pricing goods against the open-market dollar rate. Tehran had, effectively, adopted the dollar as its real currency, while publicly denouncing it.

“What initially appeared symbolic began to look practical… informal dollar transactions, once largely limited to luxury goods, steadily expanded… dollar-pegged property sales and rentals increased noticeably.”

— Iran International, March 25, 2026

Here is the lesson that every dollar-denominated investor needs to absorb: Iran’s rial collapsed because the government could not stop spending more than it collected, could not stop printing to fill the gap, and could not maintain credibility with its own citizens. Sound familiar?

The mechanism is identical everywhere it has ever happened.

Argentina.

Venezuela.

Zimbabwe.

Weimar Germany.

The details change. The process does not.

Now consider the exquisite irony: Iranians are desperately seeking dollars as a store of value.

At the moment global central banks are quietly reducing their dollar holdings. The dollar is simultaneously the currency everyone in Tehran wants to hoard, and the currency every central bank in Beijing, Moscow, and Riyadh is slowly divesting. Both groups are rational. Iranians are comparing the dollar to the rial, a no-contest. Central banks are comparing the dollar to gold and a basket of alternatives. They’re choosing diversification.

The Tehran story is not an argument that the dollar is fine. It is an argument that all fiat currencies are on the same spectrum, with the rial at one end and the dollar further along than most Americans realize. Iran got there faster because its government was more reckless, more isolated, and more corrupt. The US government is reckless, increasingly isolated, and demonstrably corrupt… They’re just moveing at a slower pace, with the luxury of reserve currency status buying extra time.

The dollar is not the rial. But the rial was not always the rial, either.

The Destination Is Fixed

Let’s map the scenarios:

Scenario A: The Iran war ends quickly. Oil falls back below $80. The petrodollar bounce reverses. The Dollar Index resumes its prior trend lower. The reserve currency share continues its slow slide toward 50%. Gold resumes its bull market.

Scenario B: The Iran war drags on. Oil stays above $100. The petrodollar temporarily props up the dollar. But the war adds trillions to the national debt, spikes inflation, and accelerates the global search for dollar alternatives including Deutsche Bank’s ‘petroyuan’ scenario. The dollar eventually falls harder from a higher level.

Scenario C: Escalation. Hormuz gets disrupted. Oil goes to $150 or $200. The global economy convulses. Emergency dollar demand spikes. The Fed responds with money printing. The dollar initially surges, then craters as the inflation hits.

Notice anything? In Scenario A, the dollar declines. In Scenario B, the dollar declines after a bounce. In Scenario C, the dollar surges and then collapses. In every scenario, real assets outperform paper ones over the relevant time horizon. In every scenario, the direction of the dollar’s long-term reserve currency share is the same.

The 31-year low in reserve currency status isn’t a crisis yet. It’s a direction. A direction that has been consistent across every administration, every Fed chairman, every market cycle for the past 25 years. The Iran war hasn’t changed the direction. It’s just created noise around the signal.

The Iranian pizza shop priced in dollars is a preview of what will happen to all fiat currencies sooner than later. They will trend toward their intrinsic value over time. The dollar is declining in reserve status while the rial is collapsing outright. These are not different phenomena. They are the same phenomenon at different speeds.

Stack gold and silver accordingly. The second half of this decade is going to be very interesting.

References

[1] Wolf Street / Wolf Richter — “Status of US Dollar as Global Reserve Currency: USD Share Drops to 31-Year Low” (March 28, 2026) https://wolfstreet.com/2026/03/28/status-of-us-dollar-as-global-reserve-currency-usd-share-drops-to-31-year-low-as-central-banks-diversify-into-other-currencies-gold/

[2] IMF — Currency Composition of Official Foreign Exchange Reserves (COFER), Q4 2025 https://data.imf.org/?sk=E6A5F467-C14B-4AA8-9F6D-5A09EC4E62A4

[3] The Bubble Bubble (Substack) — “The Dollar Is Trading Like a Petrocurrency” (March 29, 2026) https://thebubblebubble.substack.com/p/the-dollar-is-trading-like-a-petrocurrency

[4] Bloomberg — “Dollar Enjoys Petrocurrency Status as Oil Drives Markets” (March 10, 2026) https://www.bloomberg.com/news/articles/2026-03-10/dollar-oil-link-is-all-that-matters-right-now-in-currency-market

[5] Bloomberg — “Iran War Could Be Making of the Petroyuan, Deutsche Bank Says” (March 25, 2026) https://www.bloomberg.com/news/articles/2026-03-25/iran-war-could-be-making-of-the-petroyuan-deutsche-bank-says

[6] Asia Times — “Iran War Restores King Dollar’s Crown — For Now” (March 29, 2026) https://asiatimes.com

[7] Fortune — “Dollar Dominance Is Reinforced by the Global Oil Trade, but the Iran War Could Give Rise to the ‘Petroyuan'” (March 28, 2026) https://fortune.com/2026/03/28/dollar-dominance-dedollarization-global-oil-trade-iran-war-petroyuan-us-security-shield/

[8] Fortune — “Iran, the $39 Trillion National Debt and De-Dollarization: How Trump Exposed America’s Achilles Heel in Hormuz” (March 24, 2026) https://fortune.com/2026/03/24/iran-hormuz-petrodollar-national-debt-trump/

[9] Iran International — “Dollar-Pegged Pizza in Tehran Points to a Different Kind of Regime Change” (March 25, 2026) https://www.iranintl.com/en/202603242827

[10] Fortune — “Iran Issues Its Largest-Ever Currency Denomination as Inflation Ravages the Economy” (March 23, 2026) https://fortune.com/2026/03/23/iran-rial-largest-ever-currency-denomination-inflation-financial-sector-ponzi-scheme/

[11] Wikipedia — Iranian Economic Crisis (updated March 2026) https://en.wikipedia.org/wiki/Iranian_economic_crisis

[12] Middle East Monitor — “War, Oil and Power: Could the Iran Conflict Shake the Petrodollar Order?” (March 14, 2026) https://www.middleeastmonitor.com/20260314-war-oil-and-power-could-the-iran-conflict-shake-the-petrodollar-order/

[13] Bloomberg — “Treasuries Sink as Oil Jump Stokes Inflation Fears” (March 1, 2026) https://www.bloomberg.com/news/articles/2026-03-01/dollar-surges-as-traders-brace-for-war-impact-markets-wrap

[14] MarketPulse / OANDA — “The War-Petrodollar Trade Extends — Oil Jumps, Dollar to 2026 Highs” (March 3, 2026) https://www.marketpulse.com/markets/petrodollar-trade-extends-dxy-outlook/

[15] J.P. Morgan — “De-Dollarization: The End of Dollar Dominance?” https://www.jpmorgan.com/insights/global-research/currencies/de-dollarization

[16] StoneX Group — “Reserve Currency Status Slows the Dollar’s Long Decline” (February 9, 2026) https://www.stonex.com/en/market-intelligence/reserve-currency-status-slows-the-dollar-s-long-decline-2026-02-09/

[17] Geopolitical Economy Report — “Iran Challenges US Dollar, Demanding Oil Be Sold in Chinese Yuan” (March 17, 2026) https://geopoliticaleconomy.com/2026/03/17/economic-war-iran-petrodollar-oil-yuan/