As I keep emphasizing, the real money from the AI trade won’t come from picking who emerges as the AI-leader (Meta, Microsoft, Amazon, etc.).

Instead, it’s from investing in the smaller “picks and shovels” plays that the MAG-7/ hyperscalers NEED in order to complete the AI-build out.

Think of it this way… A homebuilder HAS to buy lumber, cement, nails, wires, etc. regardless of whether the home sells or not. The same is true for the current AI buildout: companies like Meta, Microsoft and the like HAVE to invest in certain sectors/ companies in order to build datacenters and other AI infrastructure.

One of the most critical sectors is photonics.

Everyone knows that the AI buildout requires chips/ Graphics Processing Units (GPUs). What many investors don’t understand is that the ability to move data between these chips is just as critical as the chips themselves. And copper wire physically cannot handle this.

Think about what’s happening inside a modern AI data center. You have thousands of GPUs working in parallel, training models that now exceed 100 trillion parameters. Every one of those GPUs needs to communicate with every other one, continuously, in real time.

Copper can’t do it. For one thing, the bandwidth isn’t there. Secondly, the heat is unmanageable. The physics simply don’t work at scale.

Enter photonics.

Photonics use light instead of electrons to carry data. In its simplest form, a photonic system has four parts:

- A laser — converts an electrical signal into a light pulse

- A waveguide — a tiny channel (often etched into silicon) that guides the light, like a fiber optic cable on a chip

- A modulator — encodes data onto the light by switching it on and off billions of times per second

- A detector — converts the light pulses back into electrical signals at the destination

That’s it. Signal in, convert to light, send through waveguide, convert back.

Capital is being deployed rapidly into the sector.

In March 2026, NVIDIA (NVDA) invested $4 billion total in photonics manufacturers — $2 billion into Lumentum and $2 billion into Coherent. Both deals included not just equity stakes but multi-billion dollar purchase commitments for advanced laser components and future capacity access rights. The deals also fund new U.S.-based fabrication facilities.

NVDA isn’t the only one.

Marvell acquired Celestial AI for $3.25 billion, bringing its “Photonic Fabric” technology in-house.

Nokia acquired Infiner for $2.3 billion giving Nokia silicon photonics and indium phosphide capabilities it previously lacked.

GlobalFoundries acquired both AMF and InfiniLink in January 2026. AMF is a premier silicon photonics foundry with a proven 200mm platform. InfiniLink is a startup specializing in advanced optical data connectivity chips.

AMD bought Enosemi for an undisclosed amount. The reason was Enosemi’s optical I/O — giving AMD its own in-house photonics capability to reduce NVIDIA dependency.

And so on.

The point I’m trying to make is that the biggest infrastructure trade of the year likely isn’t chips, but photonics. And the markets know it.

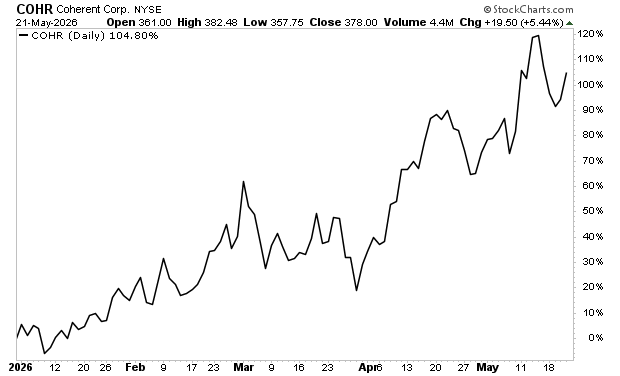

Coherent (COHR) is an American manufacturer of optical and photonic technologies. Its shares are up over 100% this year alone.

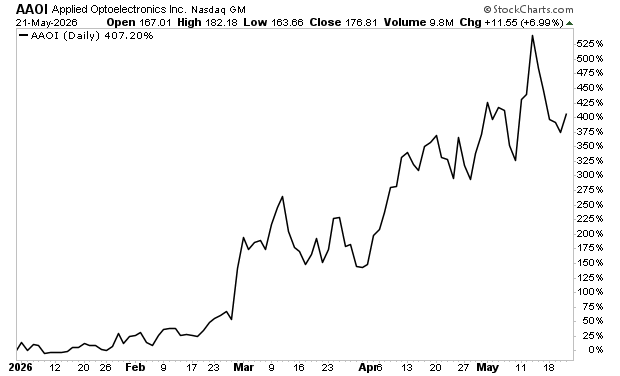

Applied Optoelectronics (AAOI) makes optical transceivers — the modules that convert electrical signals to light and back inside data centers. Its stock is up over 400% year to date.

My point here is that if you are looking to see outsized gains from the continued AI-buildout, you need to look outside of Big Tech to the “picks and shovels” plays: the companies that will profit from the AI even if the technology doesn’t result in a productivity boom.

Photonics is one such area. But there are more. Many more.

Sign up to receive our daily market commetary for more investment insights.

Best Regards

Graham Summers, MBA

Chief Market Strategist

Phoenix Capital Research