Powell’s last meeting. Warsh in the wings. A trap with no exit, dressed up as a personnel decision.

By the Dollarcollapse.com Editorial Team:

Today is almost certainly Jerome Powell’s last FOMC meeting. Kevin Warsh is on a clear path to take the chair in mid-May. We are getting a lot of mixed messages from America’s most influential voices.

Ray Dalio, who runs the largest hedge fund on earth and is nobody’s idea of a goldbug, went on CNBC and told Warsh in plain English that cutting rates would destroy what is left of the Fed’s credibility.

The president, meanwhile, has spent every public appearance for a year demanding cuts.

Federal interest expense is running upwards of $88 billion a month.

Gold is north of $4,500.

And the man being handed the steering wheel has already told the Senate that the Fed has not yet reckoned with the policy errors that produced 25 to 35 percent inflation for every American no matter the income.

This is what a fiat-currency endgame looks like in real time. Not yet bank runs and breadlines. A confirmation hearing…

Here is Dalio in his own words, on Money Movers, on Monday:

“We are certainly in a stagflationary period. Because of the issues that are here, in terms of a more immediate inflation, farther from the target. Certainly, you would not cut interest rates now. You will lose your credibility. The Federal Reserve would lose its credibility, particularly now.”

— Ray Dalio, CNBC, April 27, 2026

Dalio is the founder of Bridgewater, one of America’s most successful hedge funds. He is telling the incoming chair of the Federal Reserve, in front of a national television audience, that the only correct decision is to refuse the President who appointed him. But either way, Warsh is inheriting a crisis.

Warsh’s Choices Don’t Look Good

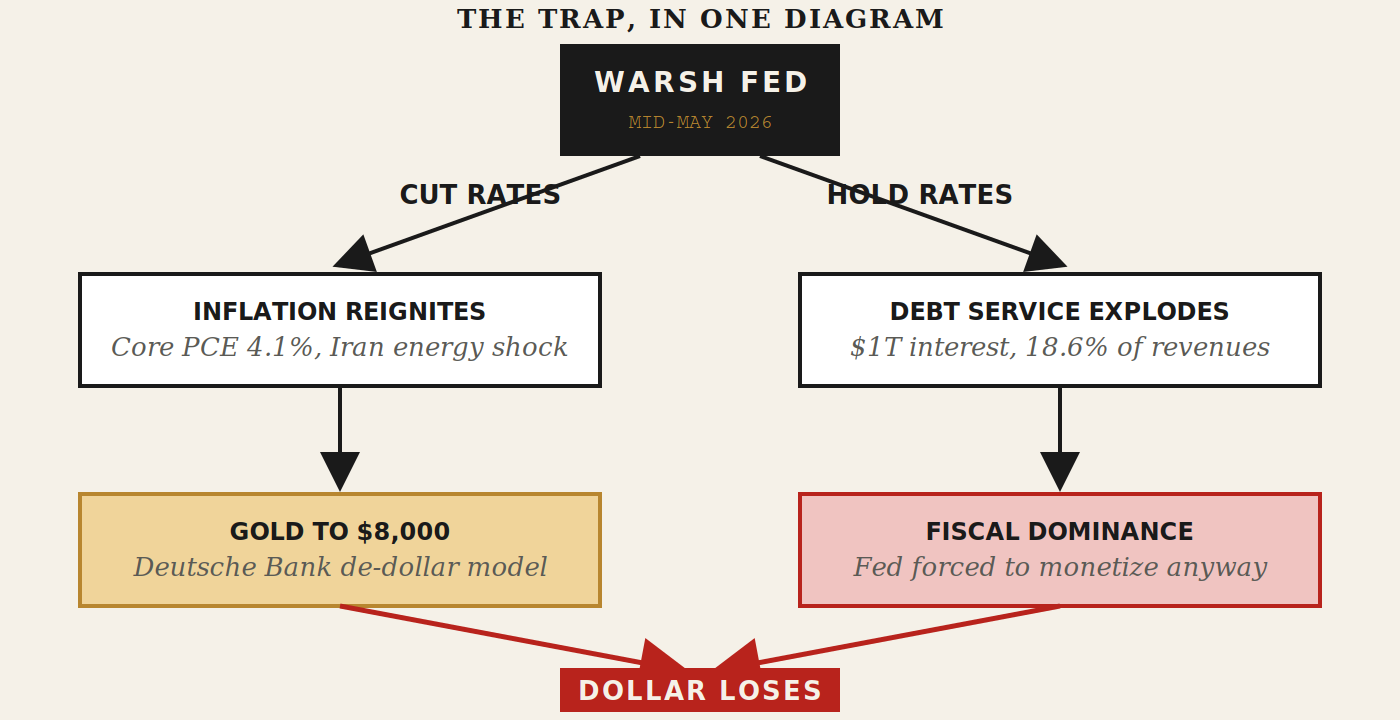

The setup matters because of what it forecloses. Warsh has two doors. Both are trapdoors.

Door one: he cuts.

The Iran war is still pushing energy prices. Core PCE is running at a 4.1 percent annualized rate. Inflation is already above target, not below it. A rate cut into that backdrop reignites the price level, breaks the dollar’s reserve narrative further, and hands the gold market the catalyst Deutsche Bank just put a number on. The German bank’s research desk modeled emerging-market central banks pushing their gold allocation to 40 percent of reserves and arrived at $8,000 an ounce, an 80 percent move from here.

Central banks have already added more than 225 million ounces since 2008. The dollar’s share of global reserves has fallen from over 60 percent in the early 2000s to about 40 percent today. The problem for Warsh is that he isn’t coming in on a clean slate. The trajectory was set before Warsh was nominated. A rate cut just compresses the timeline.

Door two: he holds.

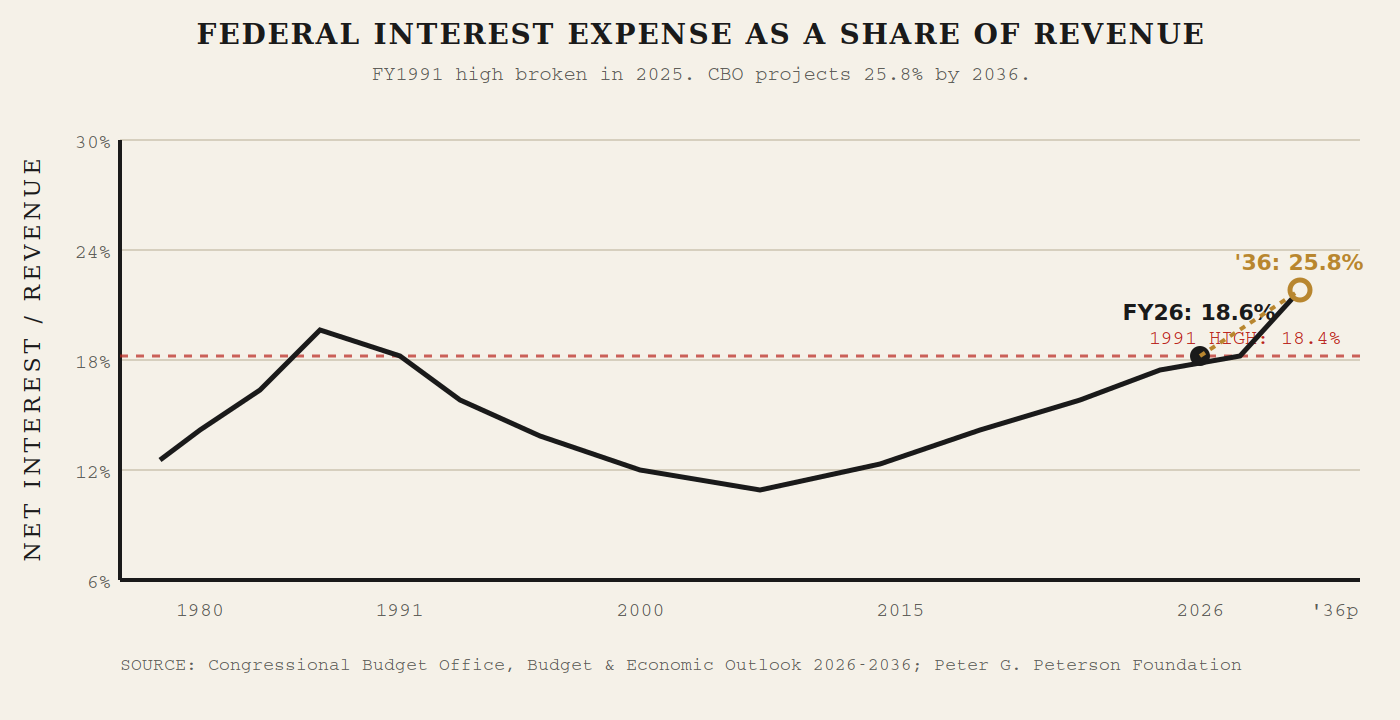

This is the door Dalio is pointing at. It is also the door that puts the fiscal arithmetic on live television. The Treasury paid out $529 billion in interest in the first six months of fiscal 2026 alone. That is roughly $88 billion a month, or $22 billion a week, or about as much as the Department of Defense’s military budget and the Department of Education combined. Net interest will hit $1 trillion this year on CBO numbers. As a share of GDP it is now 3.3 percent, which is the highest reading since 1991. As a share of federal revenues it is 18.6 percent, which is also the highest since 1991. Net interest now eats 44.5 percent of the deficit, which is the same as saying the federal government is now borrowing money primarily to pay the interest on the money it already borrowed. That is the textbook definition of a debt spiral.

The 1991 record (the red line in the chart) is no longer the ceiling.

Holding rates means watching that line go vertical. The Fed cannot hold rates indefinitely against a $39 trillion debt stack growing by $7 billion a day, because the Treasury auction calendar will eventually demand a buyer of last resort. That buyer, as it always is, will be the Fed. Hold the rate, lose the balance sheet. Cut the rate, lose the dollar. The destination is the same. The only that changes is the route.

The historical parallel here is not Volcker, even though everyone wants it to be. Volcker took a job nobody wanted in 1979 with a clear mandate from a president (Carter) and a Congress willing to absorb a brutal recession. He had room to operate. Warsh has none of that. He has a president demanding cuts, a hostile fiscal arithmetic, an inflation rate that has not behaved since 2021, and a predecessor whose press conference today will spend twenty minutes establishing that whatever happens next is not Powell’s fault.

The cleaner parallel is Arthur Burns. Burns took the chair in 1970 under a president (Nixon) who wanted easy money to win re-election, ran the printing presses to oblige, watched inflation tear out of containment, and left the institution so wounded that it took Volcker’s 20 percent funds rate and a double-dip recession to repair it. Warsh is being set up for the Burns role. The only question is whether he plays it.

And here is where the Fed-as-political-instrument story stops being a slogan and starts being a confirmation hearing transcript. At his Senate Banking testimony last week, Warsh said what most us at Dollarcollapse have been saying for the last several years:

After Covid, when prices went up to the tune of 25-to-35% for virtually all deciles of the American people, that’s an indication that the Fed missed its mark. We are still dealing with the legacy of the policy errors in 2021 and 2022.

— Kevin Warsh, Senate Banking Committee, April 2026

That is the right diagnosis. It is also a remarkable thing for the incoming chair of the institution that made the policy error to say in a confirmation hearing. The man being handed the wheel is openly campaigning on the idea that the wheel is broken. He has also proposed swapping out core PCE for a trimmed-mean inflation gauge that would make the headline number appear roughly 70 basis points closer to the 2 percent target without changing a single price in the real economy. It’s just another new ruler for an old measurement, designed to produce the cuts the president wants while preserving plausible deniability about what the Fed is actually doing.

Which brings us back to the trap. A trimmed-mean PCE that suddenly reads 70 basis points lower does not change the price of eggs, the price of beef (which the news flow today reminds us is not coming down), the price of gasoline (highest level since the Iran war started), or the cost of refinancing the debt. It just changes what the Fed says about those prices. And the bond market, which is not stupid, has already priced the gap.

Bloomberg’s own headline this morning is that “America’s Bond Market Privilege Is Disappearing as U.S. Debt Soars.” In the article, former Fed economist quoted in the same piece, Harvard’s Wenxin Du, put it about as plainly as anyone in the establishment is willing to:

“They’re just not your fly-to-safety assets because people don’t necessarily fly to them over crisis.” — Wenxin Du, Harvard, former Fed economist (Bloomberg, April 29, 2026)

So here is the convergent map.

Warsh cuts: gold runs, dollar share of reserves drops further, Deutsche Bank’s $8,000 number stops looking aggressive and starts looking late.

Warsh holds: the interest line goes vertical, the Treasury runs out of buyers at the long end, the Fed is forced into yield curve control or outright monetization, and gold runs anyway.

Warsh redefines inflation with a trimmed-mean trick: the bond market discounts the new measure on day one, real yields stay elevated, and gold runs because the institution just confirmed its own credibility crisis.

Same destination…

Powell knows this. That is why he is leaving with a smile and a wave. His parting gift to the Fed?

Plausible deniability. Whatever happens next, it happens to Warsh.

Buy the metal. The succession will sort itself out.