Most readers would know, and quite correctly, that a combination of QEs and Rate hikes does not make economic sense.

But by the same rationale, the fiat currency system we have in place in 1971 doesn’t make economic sense; or, for that matter, the Central Banking system that the Federal Reserve surreptitiously implemented after 1913 doesn’t make much sense either. So, let’s ignore – makes sense, doesn’t make sense – argument for now, and look into why the above combination is what is the most likely way forward for the US Fed.

For the uninitiated, QE (Quantitative Easing, a process that expands the Fed’s balance sheet through purchases of Treasuries or other financial assets, such as mortgage-backed securities) greatly expands the money supply and is indicative of an ultra-loose monetary policy.

Rate hikes, on the other hand, indicate a tighter monetary policy, at least in theory, as they ought to lead to a contraction of the money supply by increasing the cost of borrowing. Other things remaining the same, of course. Left unsaid more often than not is that this “higher-interest-rate-is-a-tighter-monetary-policy” does not depend on nominal interest rates but on the real interest rate, i.e., the interest rate after accounting for price inflation. Therefore, if price inflation is high or rising, interest rates must be sufficiently high to provide a positive yield and dampen borrowing.

The QE Necessity

This is as straightforward as it can get. Without any recessions and at a time when Federal Revenues are growing at a healthy 5% (of course, the bulk of the growth stems from monetary inflation, with M2 expanding at a similar pace), the increase in US National debt over FY2025-26 is on track to reach $2.4 trillion. Who is going to fund this quantum of annual debts? Certainly not the Chinese or the Japanese, given their own debt troubles.

A good portion can come from the US public/companies, as well as foreign central banks, but not at current yields on the 10- and 30-year Treasuries. The current real rates (after adjusting for even the government’s lowball estimates of price inflation at 4%) are actually negative. This has to increase substantially to attract private demand for the quantum of treasuries that need to be sold.

To complicate matters, over the course of FY 2026-27, about $8.25 trillion of maturing Federal debt must be refinanced. Excluding the nearly $3 trillion (out of this $8.25) held by the US Fed, more than $5 trillion of treasuries needs a new buyer or, at the very least, a higher interest rate to convince existing holders to roll over.

If that is the problem, it necessarily means that QE is a big part of the solution as well. Now, Warsh can choose to call this “Not QE” if he wants, but the end result is the same: the Federal Reserve’s purchases of securities aimed at economic stability.

Notwithstanding the above, the biggest driver of QEs going forward will be the bursting of US asset bubbles. The US economy is swarming with asset bubbles, with many well past the stage of bursting in a normal scenario. Private credit, housing bubble 2.0, and the AI bubble are among the more prominent and obvious ones. The less well-understood ones would be the Bond bubble and the Dollar bubble. H2 of 2026 could well see the lined-up dominoes start to fall one after another.

What would this do to the debt? My guess is we will easily see the US National Debt cross $50 trillion by Sep 2028. It is impossible to forecast the terminology Warsh would use, but the only conceivable route to fund the bulk of the increase would be QE.

Massive QEs are just around the corner.

The Rate Hikes Necessity

The 2008 GFC (Global Financial Crisis) saw a combination of QE and ZIRP (Zero Interest Rate Policy) as policy responses by the US Fed.

The 2026/27 GCC (Global Currency Crisis) will, however, see QE and rate hikes (not the Volcker-type hikes, just marginal ones) in response.

From 1981 onwards, the US Government and the Fed have used monetary inflation as a solution to all its problems – the 1987 stock market crash, the 1991 Gulf crisis, the 2000 dot com bubble burst, the 2008 GFC, and the 2019 Covid crisis. The solution was always a massive increase in the National debt and the debt-to-GDP ratio, oddly accompanied by falling 30-year Treasury rates. But this was only because price inflation, as measured by the much-flawed “Personal Consumption Expenditures” price index, has been largely benign over the decades.

Today, the situation is very different. As explained in the previous article, Kevin Warsh – Walking into an Inflationary Tsunami, the pipeline for much higher inflation in the months ahead is very strong. Both in terms of structural factors and the near-term cyclical factors.

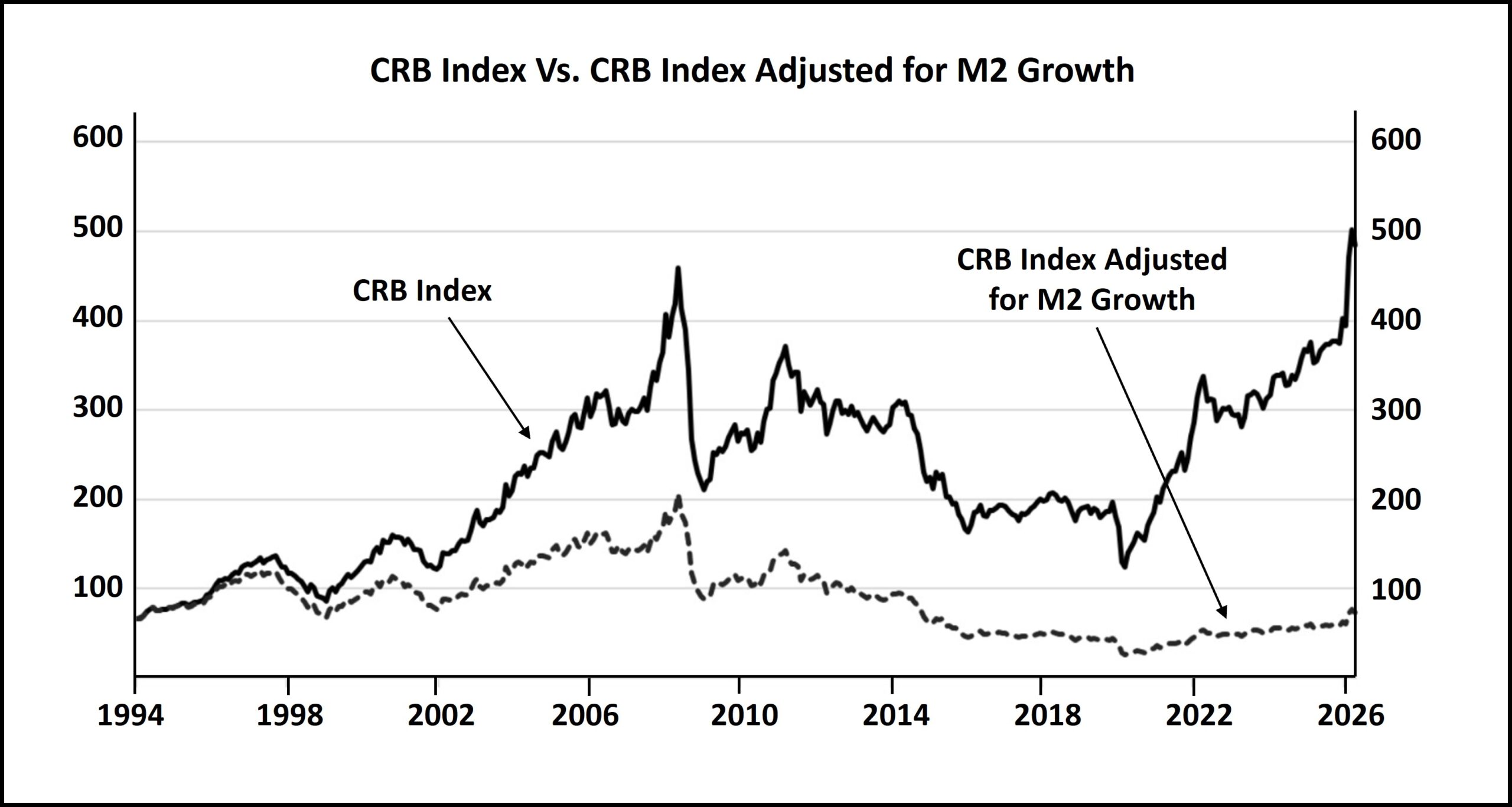

While the current CRB nominal index, as well as prices of individual commodities such as gold and copper, are at/near all-time highs, when adjusted for the monetary inflation (growth in M2) over the decades, the CRB index is just 1/3rd of the 2008 peak. The bottom of the current cycle happened in 2020, and we probably have a decade of rising commodity prices ahead. If anything, we are closer to the bottom rather than the top of commodity prices in the current cycle.

This implies that the one problem that cannot be solved by Monetary Inflation is Price Inflation. When prices are rising and the currency is rapidly losing value, the only response from an interest-rate perspective would be to raise them meaningfully. And that is what Warsh would be forced to do, despite the recessionary environment in which he would be operating. The last time the US faced this stagflationary (recession + high price inflation) situation was in the late 1970s, and Volcker raised interest rates to 20%+ to counter it.

The inflation rate at that point was about 13%, and Volcker had to offer a real interest rate of 8% to quell the forces driving price inflation. Today, given the massive debt, even a nominal 8% interest rate is out of the question. Looking ahead, on a $50 trillion national debt, an 8% interest rate would be $4 trillion, and that could well be close to 100% of the federal revenues in a recessionary environment (the federal revenues collapsed 20% after the 2008 GFC, and it took 4 years for the revenues to recover).

Therefore, interest rates are set to go higher for the foreseeable future. Just to make it abundantly clear, Warsh would certainly know that these marginal hikes would do little to counter the raging price-inflationary forces. But at the very least, he has to be twiddling his thumbs instead of doing nothing. These hikes would just be a show-and-tell to convince markets that the Fed is still working to contain price inflation. Consequently, it is quite possible that we get a 5-handle on the fed funds rate over the next 2 years. And this brings us to the next question.

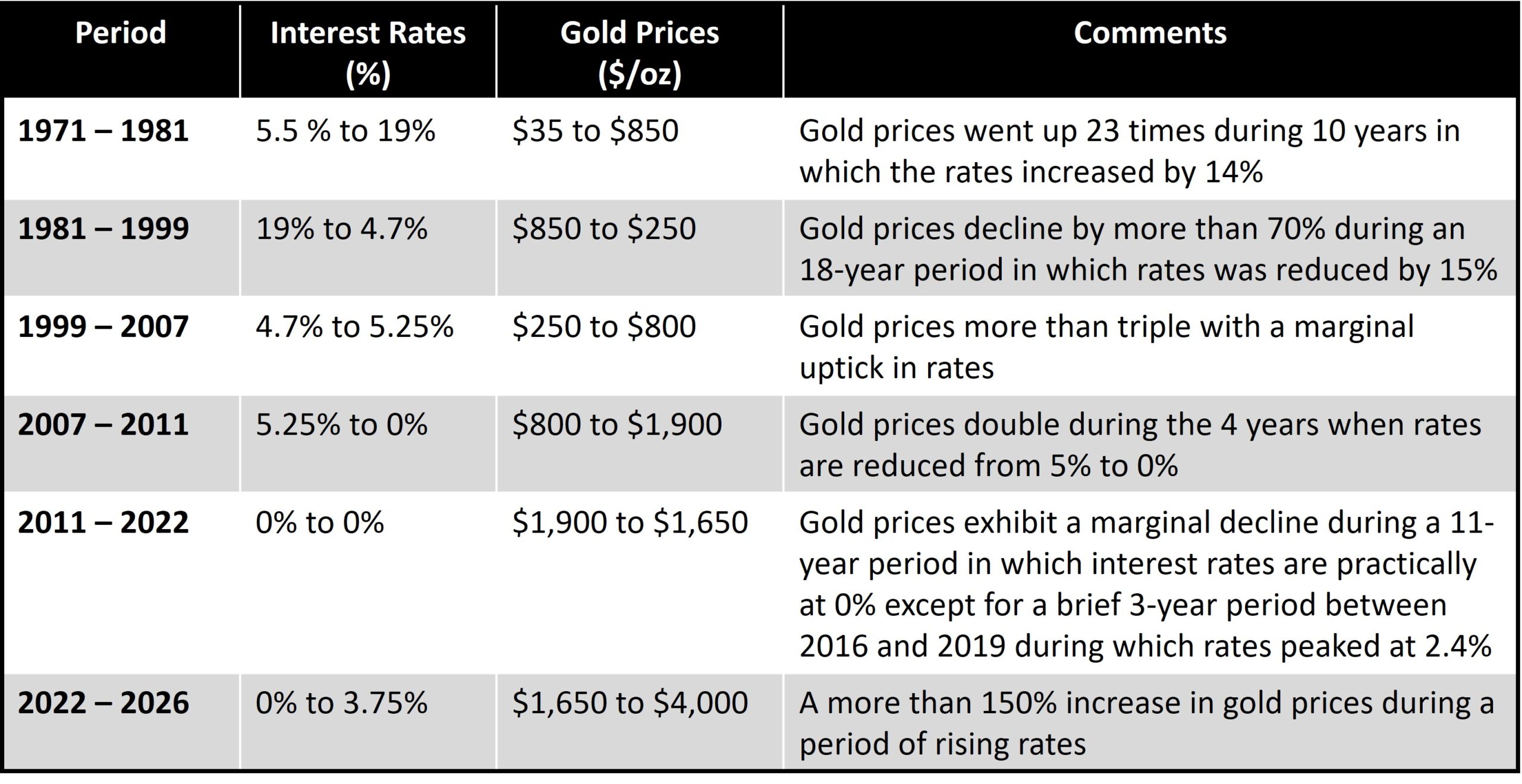

How can gold prices go higher when interest rates are rising?

The evidence that interest rates and gold prices are positively correlated (i.e., they move in the same direction) is overwhelming. When interest rates rise, gold prices also rise, and vice versa. The table below shows the relationship over the last 55+ years; except for the 4 years between 2007 and 2011, gold price movements and interest rate changes have moved in the same direction.

The reasons have been elaborated in my previous publications, but the short answer is that real interest rates affect gold price changes, not nominal interest rate changes.

The Warsh Trek – To Boldly (and Imprudently) Go Where No Fed Chair Has Gone Before

The US PCE Index has been above 2.5% for 12 months in a row, and this is well above the Fed’s target of 2%. Worse, the trajectory has been upward, and the recent May reading came in at 4.1%. If Warsh could have meaningfully raised rates, he would have done so in his very first meeting.

Warsh well understands that his quiver on the “interest rate front” is limited and must be used only when unavoidable, while pretending to be fully armed to tackle the forces of price inflation. Amidst all this, the QE expansion will occur, which will put an even greater pressure on price inflation.

As written earlier, Warsh can at best twiddle his thumbs.

About the Author

Shanmuganathan N (aka Shan) is an Economist based in India and can be contacted at sh**@***********al.com