“The boom can last only as long as the credit expansion progresses…”

~ Ludwig von Mises

Written by Bryan Lutz, Editor at Dollarcollapse.com:

A Japanese investor who woke up this morning holding a 30-year government bond owns one of the worst seats in global finance.

The yield on that bond just climbed to 3.94%, which means its price fell.

And the yen that bond pays him back in just touched its weakest level against the dollar since 1986.

He is losing on both ends at once.

So, here is the move: sell the duration.

Get out of long-dated Japanese government paper. Rotate what is left into the one asset Tokyo cannot conjure with a keystroke.

Holding to maturity does not save him. A coupon is only a promise to deliver yen on a schedule, and the yen is melting while he waits.

Now look west.

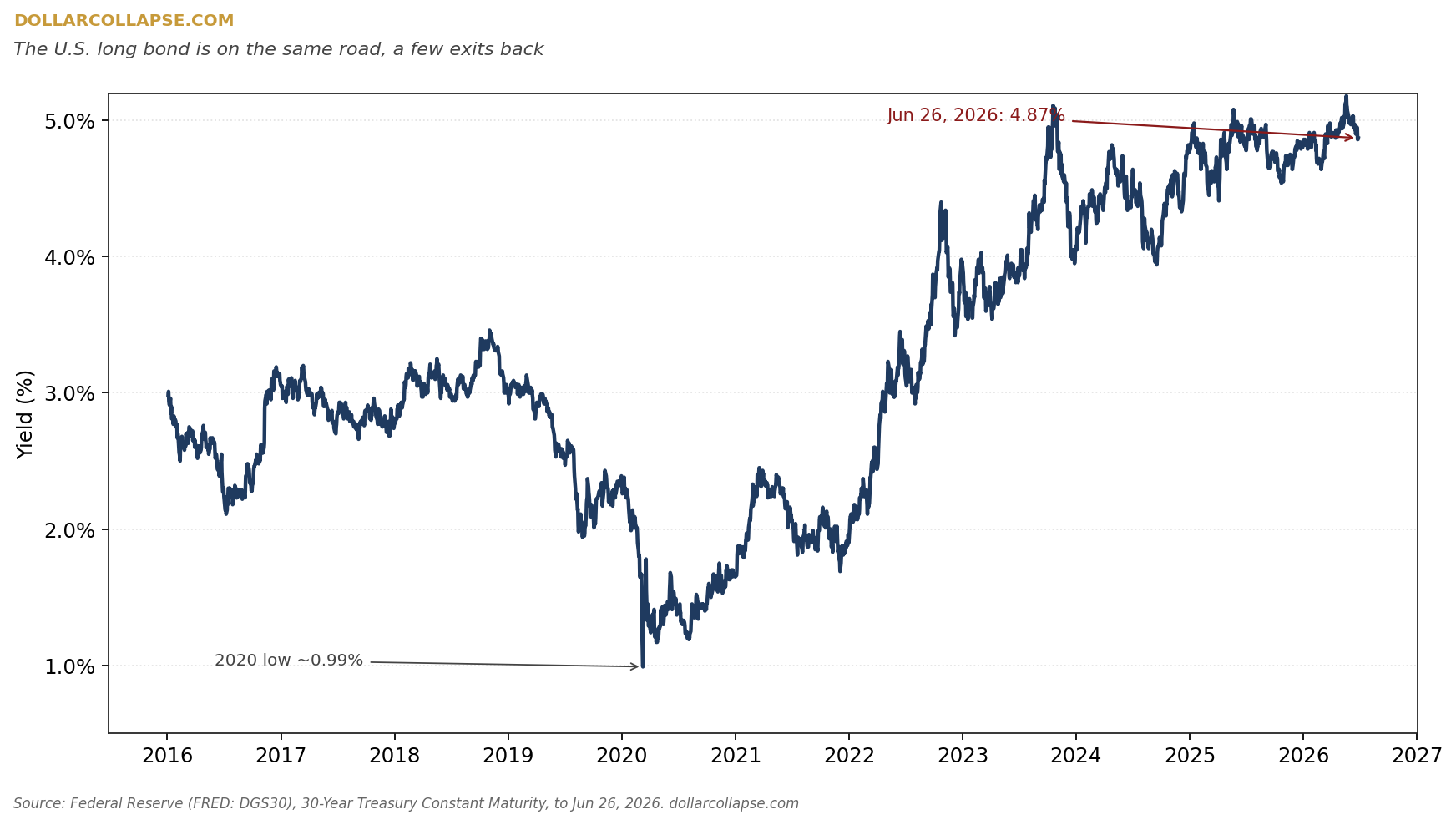

The United States is not standing where Japan stands today. It is standing a few exits back on the same highway, watching the same scenery arrive a little later. $39 trillion in debt. Interest costs north of a trillion dollars a year. A debt-to-GDP ratio above 120% and climbing.

Japan goes first because Japan is further down the road.

That is the whole reason a U.S. Treasury holder should read a Tokyo bond-market story as a memo addressed to him.

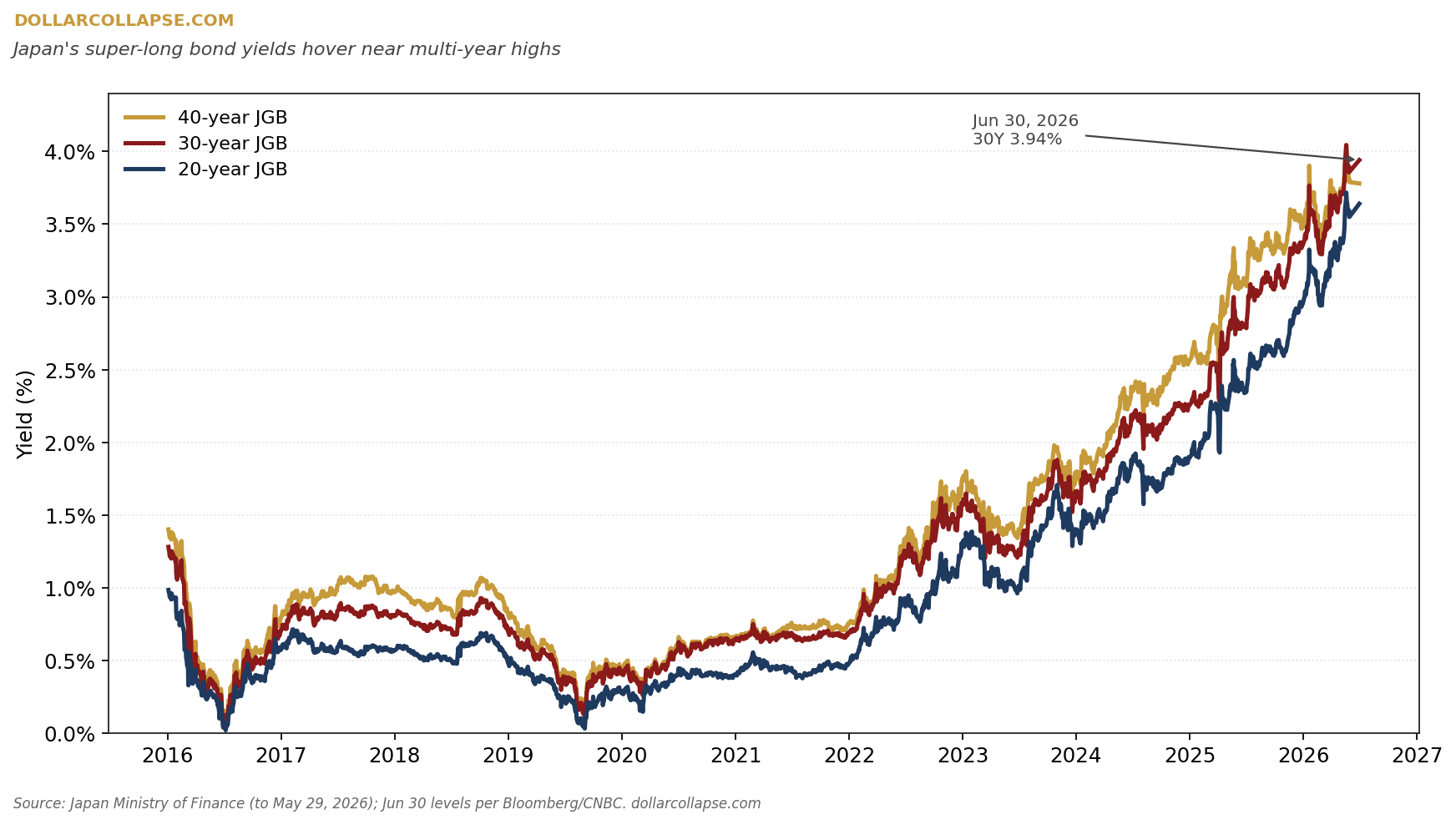

Here is what “safe” government paper has been doing in the country with the developed world’s heaviest debt load:

Each of Japan’s long bond yields have moving up and to the right since 2022, and steeper into 2026.

Why the long end is breaking

Start with the trigger that lit the fuse this week.

The yen blew through 162 to the dollar, a level last seen four decades ago.

A weak currency imports inflation, because everything Japan buys from abroad costs more in yen. And inflation is the long bond’s natural predator.

A strategist at Natixis put the problem in one sentence:

“There is no anchor for long-term inflation expectations right now.”

When investors stop trusting the central bank to hold the line on inflation, they demand more yield to hold long-dated debt. That is what 3.94% on the 30-year is telling you. There is a lack of trust…

Then there is Japan’s spending problem.

Prime Minister Sanae Takaichi has unveiled a plan to mobilize more than ¥370 trillion, roughly $2.3 trillion, into AI, semiconductors and other favored sectors through 2040.

She also prefers easy money, and she has leaned on the Bank of Japan to keep it that way.

So, the bond market is staring at a government that wants to spend trillions it does not have, and a central bank that markets no longer trust to push back.

Governments always choose to spend. Then the bond market hands it the bill. That sequence is not unique to Japan. It is not new, either. It is the oldest story in fiat money, running in the country that has run the experiment longest.

The Bank of Japan is not asleep. It raised its benchmark rate to 1% this month, the highest in three decades. But that doesn’t matter.

Tokyo even spent the reserves to defend the currency. Between April and May it deployed ¥11.7 trillion, about $72.8 billion, to prop up the yen.

The yen kept falling anyway.

That is the trap in one image: a central bank that cannot hike fast enough to defend its currency without blowing up the cost of servicing the biggest debt pile in the developed world, and cannot sit still without watching that currency bleed out.

Hike, and the debt service cost explodes. Hold, and the yen dies. There is no third door marked “no consequences.”

Here is the yen itself, forty years of it on one screen:

The line spent a decade getting stronger into 2011. It has spent every year since giving that strength back, and then some.

Why “get out” is the right call, not the panicked one

Walk the bondholder’s actual profit and loss, because the math makes the case better than any adjective.

Rising yields cut the market value of his bond today. If he sells, he sells at a loss.

If he holds to maturity instead, he collects coupons and principal in yen that buys less with each passing month. A bond sold for forty years as the definition of safe now loses on the price… AND on the unit of account at the same time.

That is what you call a slow confiscation with a payment schedule.

For decades, betting against this bond was the trade that ruined people. Traders called shorting JGBs “the widowmaker,” because the Bank of Japan controlled the curve and crushed anyone who fought it.

The thing that made it a widowmaker was central-bank control of the long end.

But that control is the exact thing breaking now.

When the anchor lifts, the bet that used to kill you becomes the bet that pays you.

So, the resolution is the one Dollar Collapse has argued for fifteen years. Move out of long-duration government promises. Move into the assets a government cannot print: gold first, because gold carries no counterparty, no maturity date, and no central bank behind it.

That is move one in any honest playbook written for the end of a fiat cycle. Japan is the country forced to read it out loud.

Does the American long-bond holder act now?

Yes. Not in a panic, and not all at once. But yes.

The United States sits earlier in this story than Japan, and it is the same story: a fiscal trap, a central bank under political pressure, and a long end waiting for the market to reprice risk it has been ignoring.

The American holding 20- and 30-year Treasuries owns the same structure that is failing in Tokyo, with a few years of runway Japan no longer has.

So, the move is not to wait for Washington’s bond market to start screaming before believing Tokyo’s.

Shorten the duration. Treat the words “risk-free” as a claim to be checked, not a fact. Begin the move into gold and hard assets while it is still a choice and not a stampede.

Japan goes first.

Take the free lesson the Japanese one is teaching right now.